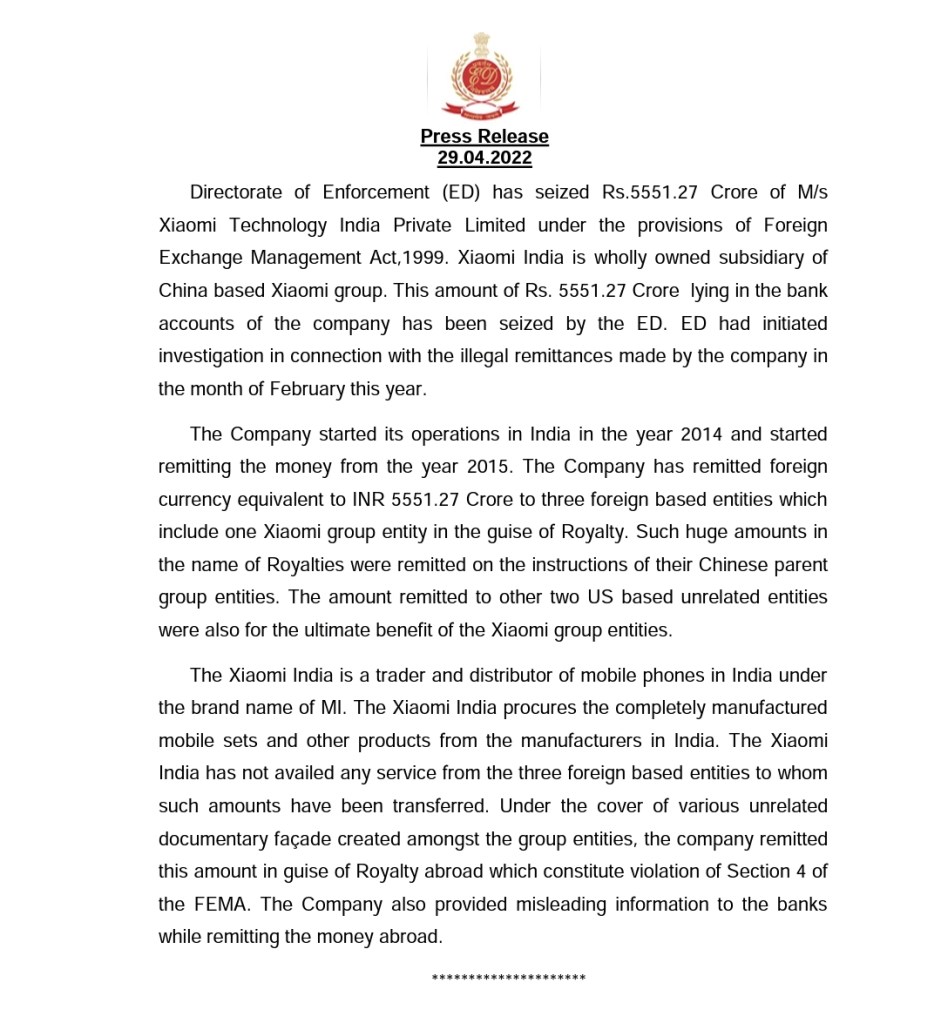

ED has seized Rs.5551.27 Cr. from M/s Xiaomi Technology India Private Limited for illegal remittances in violation of Section 4 of FEMA (Press release dated 29th April 2022)

Simplifying your business ideas, structures, functionalities, relations & operations

ED has seized Rs.5551.27 Cr. from M/s Xiaomi Technology India Private Limited for illegal remittances in violation of Section 4 of FEMA (Press release dated 29th April 2022)

New Rule 12 AC inserted

“12AC. Updated return of income.- (1) The return of income to be furnished by any person, eligible to file such return under the sub-section (8A) of section 139, relating to the assessment year commencing on the 1 st day of April, 2020 and subsequent assessment years, shall be in the Form ITR-U and be verified in the manner indicated therein.

The return of income shall be furnished by a person by following specified manner :

1.Individual, or Hindu undivided family or a firm or limited liability partnership or an association of persons or a body of individuals, whether incorporated or not, or a local authority or an artificial juridical person in whose case accounts are required to be audited under section 44AB of the Act or a Company or a political party required to furnish a return in Form ITR-7.

Manner of furnishing return of income :- Electronically under digital signature.

2. Individual, or Hindu undivided family, or firm, or limited liability partnership, or an association of persons or a body of individuals, whether incorporated or not, or a local authority or an artificial juridical person, or a person required to file a return under sub-section (4A) or sub-section (4B) or sub-section (4C) or sub-section (4D) of section 139, other than a person mentioned above.

Manner of furnishing return of income :-

(A) Electronically under digital signature; (B) Transmitting the data electronically in the return under electronic verification code.

Form ITR-U INDIAN INCOME TAX UPDATED RETURN

[For persons to update income within twenty-four months from the end of the relevant assessment year]

(Refer instructions for eligibility)

(Please see rule 12AC of the Income-tax Rules, 1962)

The Indian Computer Emergency Response Team (CERT-In) serves as the national agency for performing various functions in the area of cyber security in the country as per provisions of section 70B of the Information Technology Act, 2000. CERT-In continuously analyses cyber threats and handles cyber incidents tracked and reported to it. CERT-In regularly issues advisories to organisations and users to enable them to protect their data/information and ICT infrastructure. In order to coordinate response activities as well as emergency measures with respect to cyber security incidents, CERT-In calls for information from service providers, intermediaries, data centres and body corporate.

During the course of handling cyber incidents and interactions with the constituency, CERT-In has identified certain gaps causing hindrance in incident analysis. To address the identified gaps and issues so as to facilitate incident response measures, CERT-In has issued directions relating to information security practices, procedure, prevention, response and reporting of cyber incidents under the provisions of sub-section (6) of section 70B of the Information Technology Act, 2000. These directions will become effective after 60 days.

The directions cover aspects relating to synchronization of ICT system clocks; mandatory reporting of cyber incidents to CERT-In; maintenance of logs of ICT systems; subscriber/customer registrations details by Data centers, Virtual Private Server (VPS) providers, VPN Service providers, Cloud service providers; KYC norms and practices by virtual asset service providers, virtual asset exchange providers and custodian wallet providers. These directions shall enhance overall cyber security posture and ensure safe & trusted Internet in the country.

The directions issued by CERT-In are available at https://www.cert-in.org.in/Directions70B.jsp

First registration certificate issued for providing services as M2M Service Provider and WLAN/WPAN Connectivity Provider, informs DoT

Registration certificate issued to M/s Cloud7 Technologies Private Limited by AP-LSA Vijayawada

Government of India has identified that M2M/ Internet of Things (IoT) is one of the fastest emerging technologies across the globe, providing enormous beneficial opportunities for society, industry, and consumers. It is being used to create smart infrastructure in various verticals such as Power, Automotive, Safety & Surveillance, Remote Health Management, Agriculture, Smart Homes, Industry 4.0, Smart Cities, etc. using connected devices. Machine to Machine communication is going to play a major role and will contribute significantly towards the government of India initiative of Digital India and Make in India.

In order to strengthen the M2M eco-system and to facilitate wider proliferation and innovation in the sector, DoT has recently issued guidelines for registration of M2M Service Providers and WPAN/WLAN Connectivity Providers and commenced the process of on-boarding the M2M Service Providers through a simple online registration process, at a nominal cost of Rs. 5000, within 15 days timeframe, through the DoT’s existing Saral Sanchar portal, to aid in ease of doing business. It has been envisaged that entities which are offering/providing the M2M services based on SIM/ LAN shall register as M2M Service Provider and entities which use WPANWLAN technologies for providing M2M connectivity, spectrum shall register as WPAN/WLAN Connectivity Providers. This registration shall help in addressing concerns like connectivity with TSPs, KYC, traceability and encryption for the M2M service providers.

In this regard, DoT is delighted to share that the first registration certificate for providing services as M2M Service Provider and WLAN/WPAN Connectivity Provider, has been issued to M/s Cloud7 Technologies Private Limited on 26.04.22 by AP-LSA Vijayawada. The company is engaged in the planning, installation and management of wireless/RF networks in the unlicensed bands in India.

With the rapid acceptability of all sectors to digitalize and automate processes, and the advent of new manufacturing techniques and Industry 4.0, DoT expect a quantum jump in the use of IoT and M2M services all across the country, which would generate massive employment opportunities even in the far-flung areas. It would present a host of opportunities to entrepreneurs and startups to participate and develop innovative applications and solutions for the benefit of the citizens. This will lead to a plethora of citizen centric services across different verticals like Power, Automotive, Safety & Surveillance, Remote Health Management, Agriculture, Smart Cities & Homes, Industry 4.0, etc. The resultant explosion in IoT based services would further cultivate the digital ecosystem in the country.

Status Note on GST compensation released to States/UTs

₹ 2.78 lakh crore of compensation released to States for the year 2020-21 itself ; nothing is pending for the year

Centre released ₹ 7.35 lakh crore and compensation of ₹78,704 crore pending only for the year 2021-22

At the time of introduction of GST, the Constitution amendment provided that the Parliament, by law shall provide compensation to States for a period of five years for loss of revenue due to introduction of GST. Accordingly, the GST Compensation to States Act was legislated which provides for release of compensation against 14% year-on-year growth over revenues in 2015-16 from taxes subsumed in GST. This compensation cess is credited to the compensation fund and as per the Act, all compensation is paid out of the fund. Presently, cess is levied on items like pan masala, tobacco, coal and cars.

Compensation of about ₹ 49,000 crore has been released for 2017-18 from the fund, which increased to ₹ 83,000 crore for 2018-19 and further to ₹ 1.65 lakh crore in 2019-20. For these three years, almost ₹ 3 lakh crore compensation was released to States. However, the compensation requirement increased substantially during 2020-21 due to impact of covid on revenues. To ensure that States have adequate and timely resources to combat covid and related issues, Centre borrowed ₹ 1.1 lakh crore in 2020-21 and ₹ 1.59 lakh crore in 2021-22 and passed it on to States on a back-to-back basis. During 2021-22, Centre ensured that release of this amount of ₹ 1.59 lakh crore was front loaded to ensure that States have adequate resources in the earlier part of the year.

Taking into account this loan, ₹ 2.78 lakh crore of compensation has been released to States for the year 2020-21 itself and nothing is pending for the year. Including the assistance released on back-to-back basis, ₹ 7.35 lakh crore has been released to States till now and, currently, only for the year 2021-22, compensation of ₹78,704 crore is pending due to inadequate balance in the fund, which is equivalent to compensation of four months.

Normally, compensation for ten months of April-January of any financial year is released during that year and the compensation of February-March is released only in the next financial year. As explained earlier, compensation of eight out of ten months of 2021-22 has already been released to States. The pending amount will also be released as and when amount from cess accrues in the compensation fund.

Status Note on GST compensation released to States/UTs

₹ 2.78 lakh crore of compensation released to States for the year 2020-21 itself ; nothing is pending for the year

Centre released ₹ 7.35 lakh crore and compensation of ₹78,704 crore pending only for the year 2021-22

At the time of introduction of GST, the Constitution amendment provided that the Parliament, by law shall provide compensation to States for a period of five years for loss of revenue due to introduction of GST. Accordingly, the GST Compensation to States Act was legislated which provides for release of compensation against 14% year-on-year growth over revenues in 2015-16 from taxes subsumed in GST. This compensation cess is credited to the compensation fund and as per the Act, all compensation is paid out of the fund. Presently, cess is levied on items like pan masala, tobacco, coal and cars.

Compensation of about ₹ 49,000 crore has been released for 2017-18 from the fund, which increased to ₹ 83,000 crore for 2018-19 and further to ₹ 1.65 lakh crore in 2019-20. For these three years, almost ₹ 3 lakh crore compensation was released to States. However, the compensation requirement increased substantially during 2020-21 due to impact of covid on revenues. To ensure that States have adequate and timely resources to combat covid and related issues, Centre borrowed ₹ 1.1 lakh crore in 2020-21 and ₹ 1.59 lakh crore in 2021-22 and passed it on to States on a back-to-back basis. During 2021-22, Centre ensured that release of this amount of ₹ 1.59 lakh crore was front loaded to ensure that States have adequate resources in the earlier part of the year.

Taking into account this loan, ₹ 2.78 lakh crore of compensation has been released to States for the year 2020-21 itself and nothing is pending for the year. Including the assistance released on back-to-back basis, ₹ 7.35 lakh crore has been released to States till now and, currently, only for the year 2021-22, compensation of ₹78,704 crore is pending due to inadequate balance in the fund, which is equivalent to compensation of four months.

Normally, compensation for ten months of April-January of any financial year is released during that year and the compensation of February-March is released only in the next financial year. As explained earlier, compensation of eight out of ten months of 2021-22 has already been released to States. The pending amount will also be released as and when amount from cess accrues in the compensation fund.

GSTR-1 enhancements & improvements :

The statement of outward supplies in FORM GSTR-1 is to be furnished by all normal taxpayers on a monthly or quarterly basis, as applicable. Quarterly GSTR-1 filers have also been provided with an optional Invoice Furnishing Facility (IFF) for reporting their outward supplies to registered persons (B2B supplies) in the first two months of the quarter. Continuous enhancements & technology improvements in GSTR-1/IFF have been made from time to time to enhance the performance & user-experience of GSTR-1/IFF, which has led to improvements in Summary Generation process, quicker response time, and enhanced user-experience for the taxpayers.

The previous phase of GSTR-1/IFF enhancement was deployed on the GST Portal in November 2021. In that phase, new features like the revamped dashboard, enhanced B2B tables, and information regarding table/tile documents count were provided. In continuation to the same, the next Phase of the GSTR-1/IFF improvements is now available on the Portal.

GSTR-1/IFF can be viewed as usual by navigating in the following manner :

Return Dashboard > Selection of Period > Details of outward supplies of goods or services GSTR-1 > Prepare Online

The following changes are being done in this phase of the GSTR-1/IFF enhancements :

Removal of ‘Submit’ button before filing : The present two-step filing of GSTR-1/IFF involving ‘Submit’ and ‘File’ buttons will be replaced with a simpler single-step filing process . The upcoming ‘File Statement’ button will replace the present two-step filing process and will provide taxpayers with the flexibility to add or modify records till the filing is completed by pressing the ‘File Statement’ button.

Consolidated Summary : Taxpayers will now be shown a table-wise consolidated summary before actual filing of GSTR-1/IFF. This consolidated summary will have a detailed & table-wise summary of the records added by the taxpayers. This will provide a complete overview of the records added in GSTR-1/IFF before actual filing.

Recipient wise summary : The consolidated summary page will also provide recipient-wise summary, containing the total value of the supplies & the total tax involved in such supplies for each recipient. The recipient-wise summary will be made available with respect to the following tables of GSTR-1/IFF, which have counter-party recipients :- Table 4A : B2B supplies- Table 4B : Supplies attracting reverse charge- Table 6B : SEZ supplies- Table 6C : Deemed exports- Table 9B : Credit/Debit notes

It was previously intimated that this enhancement would be made available on the Portal shortly. It is to inform that these changes have now been implemented, and are available on the Portal. For detailed advisory & sample screenshots of the GSTR-1/IFF improvements & enhancements, please click here

https://acrobat.adobe.com/link/review?uri=urn:aaid:scds:US:0efdd15a-eb1f-306e-a2e0-e8bd5e866807

Thanking you,

Team GSTN

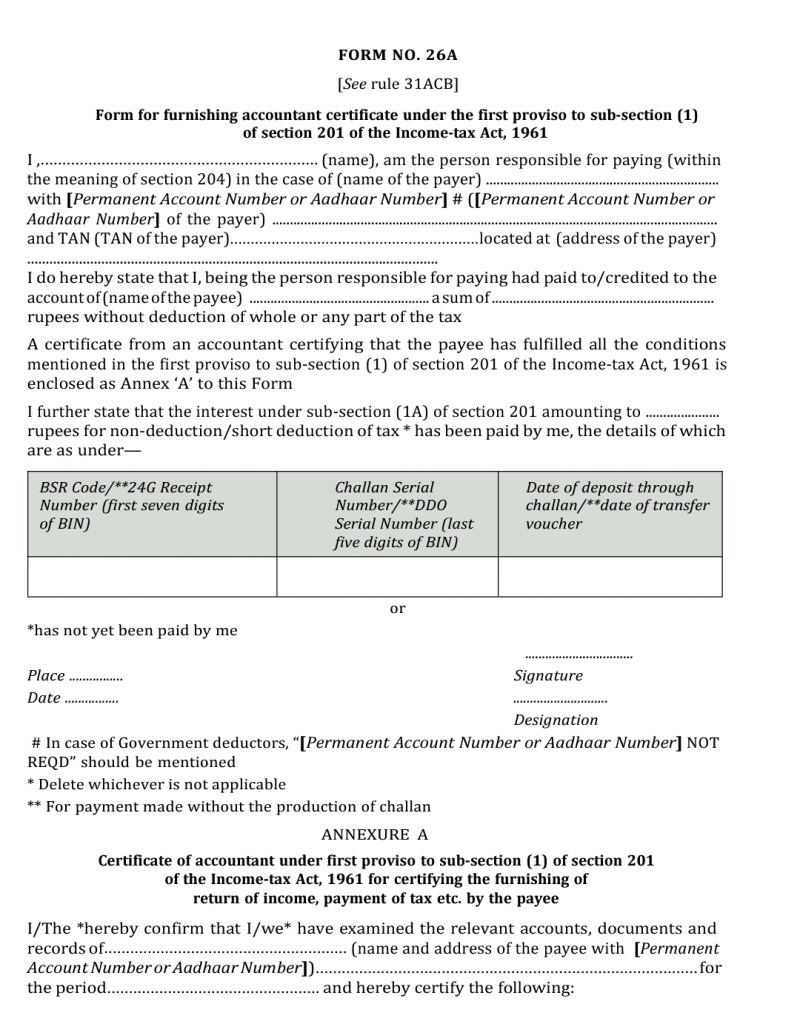

Form 26A : Form for furnishing accountant certificate under the first proviso to sub-section (1) of section 201 of the Income-tax Act, 1961

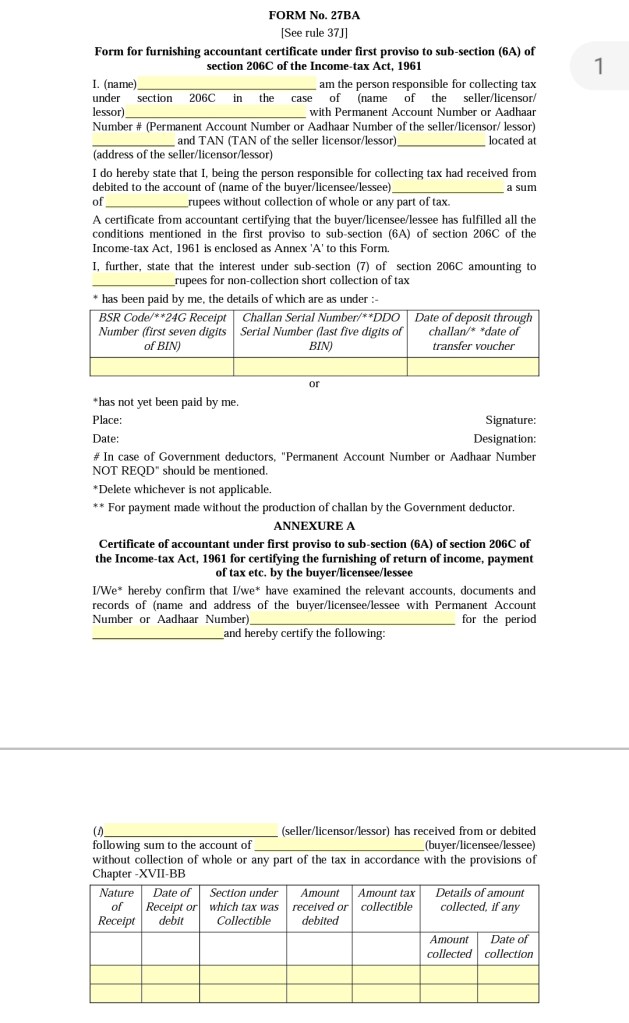

Form 27BA : Form for furnishing accountant certificate under first proviso to sub-section (6A) of section 206C of the Income-tax Act, 1961

Form 10BD : Statement of particulars to be filed by reporting person under clause (viii) of sub-section (5) of section 80G and clause (i) to sub-section (1A) of section 35 of the Income-tax Act, 1961

Form 10BE

Certificate of donation under clause (ix) of sub-section (5) of section 80G and under clause (ii) to sub-section (1A) of section 35 of the Income-tax Act, 1961

are available for filing on the portal.

Income Tax Return

👉 Income Tax Department enables e-filing of ITR-1, ITR-2 and ITR-4 for AY 2022-23;

👉 ITR-1 and ITR-4 can be filed using the online or offline utility

👉 ITR-2 can be filed only using the offline utility;

Taxpayers can download ITR Offline Utility through “Downloads” Menu option, fill and file the ITR through the same.

Documentation requirements in case of transmission of securities.

(1) In case of transmission of securities, where the securities are held in single name with nomination, the following documents shall be submitted:

(a) duly signed transmission request form by the nominee;

(b) original death certificate or copy of death certificate attested by the nominee subject to verification with the original or copy of death certificate duly attested by a notary public or by a Gazetted Officer;

(c) self-attested copy of the Permanent Account Number card of the nominee, issued by the Income Tax Department.

(2) In case of transmission of securities, where the securities are held in single name without nomination, the following documents shall be submitted:

(a) a notarized affidavit from all legal heir(s) made on non-judicial stamp paper of appropriate value, to the effect of identification and claim of legal ownership to the securities:

Provided that in case the legal heir(s)/claimant(s) are named in the Succession Certificate or Probate of Will or Will or Letter of Administration as may be applicable in terms of Indian Succession Act, 1925 (39 of 1925) or Legal Heirship Certificate or its equivalent certificate issued by a competent Government Authority, an affidavit from such legal heir(s)/claimant(s) alone shall be sufficient;

(b) duly signed transmission request form by the legal heir(s)/claimant(s);

(c) original death certificate or copy of death certificate attested by the legal heir(s)/claimant(s) subject to verification with the original or copy of death certificate duly attested by a notary public or by a Gazetted Officer;

(d) self-attested copy of the Permanent Account Number card of the legal heir(s)/claimant(s), issued by the Income Tax Department;

(e) a copy of Succession Certificate or Probate of Will or Will or Letter of Administration or Court Decree as may be applicable in terms of Indian Succession Act, 1925 (39 of 1925) or Legal Heirship Certificate or its equivalent certificate issued by a competent Government Authority, attested by the legal heir(s)/claimant(s) subject to verification with the original or duly attested by a notary public or by a Gazetted Officer:

Provided that in a case where a copy of Will or a Legal Heirship Certificate or its equivalent certificate issued by a competent Government Authority is submitted, the same shall be accompanied with a notarized indemnity bond from the legal heir(s) /claimant(s) to whom the securities are transmitted, in the format specified by the Board:

Provided further that in a case where a copy of Legal Heirship Certificate or its equivalent certificate issued by a competent Government Authority is submitted, the same shall also be accompanied with a No Objection from all non-claimants, stating that they have relinquished their rights to the claim for transmission of securities;

(f) for cases where value of securities is up to rupees five lakhs per listed entity in case of securities held in physical mode, and up to rupees fifteen lakhs per beneficial owner in case of securities held in dematerialized mode, as on date of application, and where the documents mentioned in para (e) are not available, the legal heir(s) /claimant(s) may submit the following documents:

(i) no objection certificate from all legal heir(s) stating that they do not object to such transmission or copy of family settlement deed executed by all the legal heirs duly attested by a notary public or by a Gazetted Officer; and

(ii) a notarized indemnity bond made on non-judicial stamp paper of appropriate value, indemnifying the Share Transfer Agent/ listed entity, in the format specified by the Board:

Provided that the listed entity may, at its discretion, enhance the value of securities from the threshold limit of rupees five lakhs, in case of securities held in physical mode.”

(SEBI NOTIFICATION DATED 25 April 2022)