CGST Commissionerate Mumbai South Arrests Co-conspirator in a Fake Input Tax Credit Claim of Rs. 11.07 Cr; Proprietor arrested earlier

CGST Mumbai South Commissionerate has detected tax evasion of Rs. 876 Crores, recovered Rs. 14.4 Crores so far

Anti-Evasion Unit of Mumbai South CGST Commissionerate has arrested the co-conspirator in a case of M/s New Laxmilal & Co. (GSTIN 27ACAPS6257K1ZS) involving fake ITC of Rs. 11.07 Cr on the strength of bogus invoices of Rs 62.90 Cr, without actual movement of goods. This case is a part of Anti-Evasion drive launched by CGST, Mumbai Zone against the tax evaders.

The accused has accepted that he supplied bogus invoices to M/s New Laxmilal & Co. involving network of seven non-existent entities. Based on material evidence and his confessional statement, the accused was arrested under Section 69 of the CGST Act, 2017 for committing offences under Section 132(1) (b) & (c) read with Section 132(5) of CGST Act, 2017. He was produced before Additional CMM court, Mumbai today, 26th April 2022 and was remanded to judicial custody of 14 days. The proprietor of M/s New Laxmilal & Co. had already been arrested in Dec 2021 for availing and utilizing fake ITC on the strength of bogus invoices of Rs 62.90 Cr.

As a part of this drive, CGST Mumbai South Commissionerate has detected tax evasion of Rs 876 Crores approx., recovered Rs. 14.4 Crores approx. and arrested eight persons during the last seven months.

The CGST department is using state of the art and sophisticated data analytics and network analysis tools using Artificial Intelligence, to identify potential and chronic tax offenders. Department is also coordinating with other tax and law enforcing authorities for nabbing tax evaders.

The International Financial Services Centres Authority (IFSCA), in furtherance of its mandate to develop and regulate financial products, financial services and financial institutions in the International Financial Services Centres (IFSC) and to encourage promotion of financial technologies (‘FinTech’) across the spectrum of banking, insurance, securities, and fund management in IFSC has issued a detailed “Framework for FinTech Entity in the IFSCs”.

The “Framework for FinTech Entity in the IFSCs” is aimed at givingboost to the establishment of a world class FinTech Hub at GIFT IFSC comparable with other International Financial Centers (IFCs). The framework proposes to cover (i) financial technology (FinTech) solutions resulting in new business models, applications, process or productsin areas/activities linked to financial services regulated by IFSCA and (ii) advanced/innovative technological solutions which aid and assist activities in relation to financial products, financial services and financial institutions (TechFin).

The framework provides for a dedicated Regulatory Sandbox for FinTech products or solutions namely IFSCA FinTech Regulatory Sandbox and empowers IFSCA to grant Limited Use Authorization within FinTech Regulatory Sandbox to the eligible financial technology entities in IFSC. This would enable them to apply and avail Grants under the IFSCA FinTech Incentive Scheme 2022.

Further, it also enables some class/categories of technology companies having (i) a deployable advanced/innovative technology solution which aids and assists activities in relation to financial products, financial services, financial institutions and, (ii) credible track record including financial performance, to obtain Direct Entry (Authorization by IFSCA) by IFSCAwithout entering into the Regulatory Sandbox.

The framework also incorporates the Inter Operable Regulatory Sandbox (IoRS) mechanism. IoRS is a proposed mechanism to facilitate testing of innovative hybrid financial products / services falling within the regulatory ambit of more than one financial sector regulators. IFSCA will facilitate Indian FinTech’s seeking access to foreign markets and foreign FinTech’s seeking entry into India.

The framework proposes a Regulatory Referral mechanism which shall be governed as per the provisions of the Memorandum of Understanding (MoU) or collaboration or special arrangement between IFSCA and corresponding overseas Regulator(s)

IFSCA endeavors to support FinTech firms for proof of concept (PoC), minimum viable product (MVP), prototype development, product trials, commercialization, and global market access etc.

The GIFT-IFSC offers the unique advantage of being a separate financial jurisdiction within India which is treated like an offshore jurisdiction from FEMA angle with no restriction on currency convertibility. The framework issued by IFSCA, a unified regulator for Banking, Capital Markets, Insurance and Funds Management in IFSC, would enable FinTech firms having innovative ideas or solutions across the banking, capital or insurance sector to have seamless interaction with a single regulator.

It has been noted that a section of the media has reported that feedback has been sought from States regarding a suggestion for raising Good & Services Tax (GST) rates on 143 items.

Some reports have even carried the number and description of items. It is clarified that no feedback from States has been sought on the GST rates for any specific items or specific proposals to restructure the rates and the reports regarding the same are purely speculative without any basis in fact.

The GST Council, in its 45th Meeting had formed a Group of Ministers (GoM) to look into the rationalization of rates. The deliberations of the Group are ongoing. The views of the States were sought generally on the Terms of References (ToRs) of the GoM soon after it was set up in September, 2021. A report of the Group is yet to be submitted to the Council for consideration.

Digital Identity plays an important role in development of society, both socially and financially. Ministries/Departments should utilize ‘Aadhaar’ as a foundation to achieve the goal of “saturation” i.e. to reach 100% beneficiaries. Aadhaar has proved to be one of the biggest innovations of the country. Quite interestingly, Aadhaar has given identity to a large number of people who did not have any identity whatsoever earlier. It has bridged the digital divide, enabled e-KYC services, provided banking at the doorstep and at mobiles and facilitated cash transfer directly into the bank accounts of the needy and deserving recipients of various welfare schemes of the Government. The scale and facilities extended by Aadhaar are unheard of in entire world. Benefits of Aadhaar can be classified not only in monetary savings directly to the state but also the indirect benefits accrued in terms of modifying and stimulating responsible behaviour and digital experience of Aadhaar based identity in different sectors and states.

Various schemes like One Nation One Card are actively utilizing Aadhaar for digital authentication. Some encouraging examples like increased customer satisfaction at Fair price shops in Karnataka came to fore during the workshop. It was also deliberated during the discussions that security and privacy of resident data holds utmost importance and UIDAI should always endeavour to continue necessary measures to preserve the confidentiality, integrity & availability of same. A digital identity eco-system must support resident-centricity and allow consent-based framework for growth, scalability and ease of access to residents.

Multiple opportunities enabled by use of Aadhaar as a foundational identity in different sectors like Food Security, DBT, Scholarships, Fintech, Lending, Healthcare etc. various untapped sectors and gaps which can reap the potential of Digital Identity to reach the last mile of users and achieve universal inclusion, both social as well as financial with the cooperation of various Ministries/Departments of Government of India in order to fulfill the vision of ‘Ease of living’ for the residents.

Functioning of Aadhaar Ecosystem and good practices followed by central government ministries utilizing Aadhaar Platform, for instance, Faceless Transport Services (eTransport MMP), PDS, DBT Schemes, eSHRAM portal etc.

(Source: Ministry of Electronics & IT Press Release dated 22 April 2022)

India Post over the recent days has been observing various URLs/Websites getting circulated in social media such as WhatsApp, Telegram, Instagram and through emails / SMS containing tiny URLs/ Short URLs, claiming to be providing Government Subsidies through certain surveys, quizzes.

We wish to inform the citizens of the Country that India Post is not involved in any such activities like announcing Subsidies, Bonus or Prizes based on Surveys etc. Public receiving such notifications/messages /emails are requested not to believe or respond to such fake and spurious messages or share any personal details. It is also requested not share any personally identifiable information such as date of birth, Account numbers, mobile numbers, place of Birth & OTP etc.

India Post though is taking necessary action to prevent these URLs / links / Websites to be taken down through various prevention mechanisms. Public at large is once again requested not to believe or respond to any fake / spurious messages / communications / links.

India Post and Fact Check Unit of Press Information Bureau (PIB) have declared these URLs/Websites as fake through social media.

नकली वेबसाइट ‘https://t.co/enD9FVZYad जैसे कई वेबसाइट भारतीय डाक पर लकी ड्रा करने का दावा कर रही है। भारतीय डाक/डाक विभाग का ऐसी गतिविधि से कोई लेना-देना नहीं है। ऐसी धोखाधड़ी गतिविधियों से सावधान रहें। pic.twitter.com/0UcHXQiIFH— India Post (@IndiaPostOffice) April 21, 2022

Multiple fake websites like ‘https://t.co/enD9FVZYad‘ claims to be running @indiapost_dop 170th anniversary lucky draw. India Post/Department of Posts has nothing to do with such scamming activity. Beware of such fraudulent activities.— India Post (@IndiaPostOffice) April 21, 2022

▶️ Neither the website nor the organisation is associated with the India Post.

▶️ Beware of such fake organisations and webpages.— India Post (@IndiaPostOffice) April 21, 2022

A #FAKE lucky draw in the name of @IndiaPostOffice is viral on social media and is offering a chance to win ₹6,000 after seeking one’s personal details#PIBFactCheck

Gujarat ROC Penalty order for violation of Section 137 read with Section 134 of CA 2013 in the matter of M/S. SVH FABRICS PRIVATE LIMITED

Facts: Company has failed to attach complete Director’s Report (only first page enclosed) in AOC-4, which is a violation attracted penal provisions of Section 137(1) of the CA, 2013 and the company and every officers in default have violated the aforesaid provisions ofthe Companies Act, 2013.

Penalty imposed on Company & all Directors & instructions for fresh filing of Form AOC 4 with additional fees

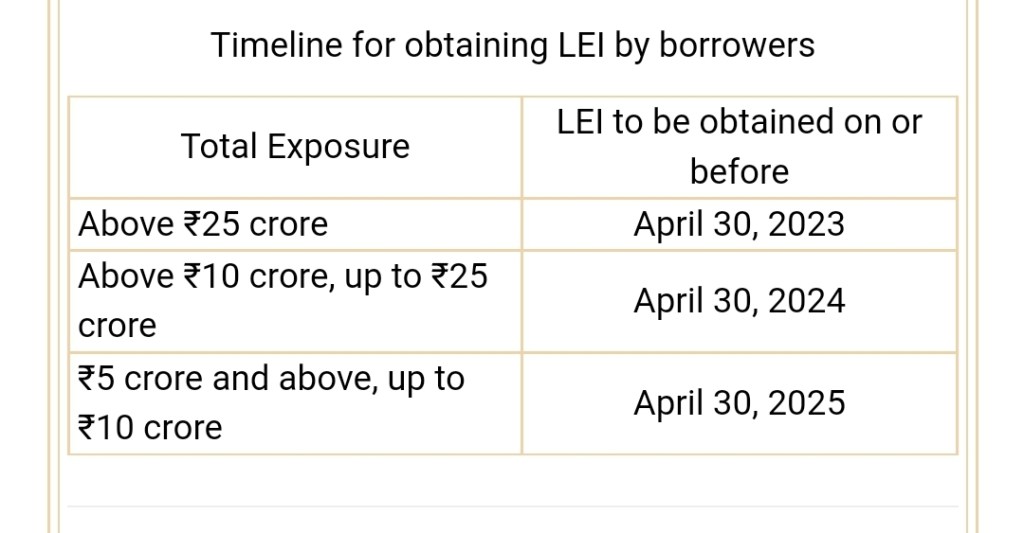

It has been decided that the guidelines on LEI stand extended to Primary (Urban) Co-operative Banks (UCBs) and Non-Banking Financial Companies (NBFCs).

It is further advised that non-individual borrowers enjoying aggregate exposure of ₹5 crore and above from banks and financial institutions (FIs) shall be required to obtain LEI codes as per the timeline given below:

“Exposure” for this purpose shall include all fund based and non-fund based (credit as well as investment) exposure of banks/FIs to the borrower. Aggregate sanctioned limit or or outstanding balance, whichever is higher, shall be reckoned for the purpose. Lenders may ascertain the position of aggregate exposure based on information available either with them, or CRILC database or declaration obtained from the borrower.

Borrowers who fail to obtain LEI codes from an authorized Local Operating Unit (LOU) shall not be sanctioned any new exposure nor shall they be granted renewal/enhancement of any existing exposure. However, Departments/Agencies of Central and State Governments (not Public Sector Undertakings registered under Companies Act or established as Corporation under the relevant statute) shall be exempted from this provision.

These directions are issued under sections 21, 35A and 56 of the Banking Regulation Act, 1949, sections 45JA and 45L of the Reserve Bank of India Act, 1934, section 30A of the National Housing Bank Act, 1987 and section 6 of the Factoring Regulation Act, 2011.

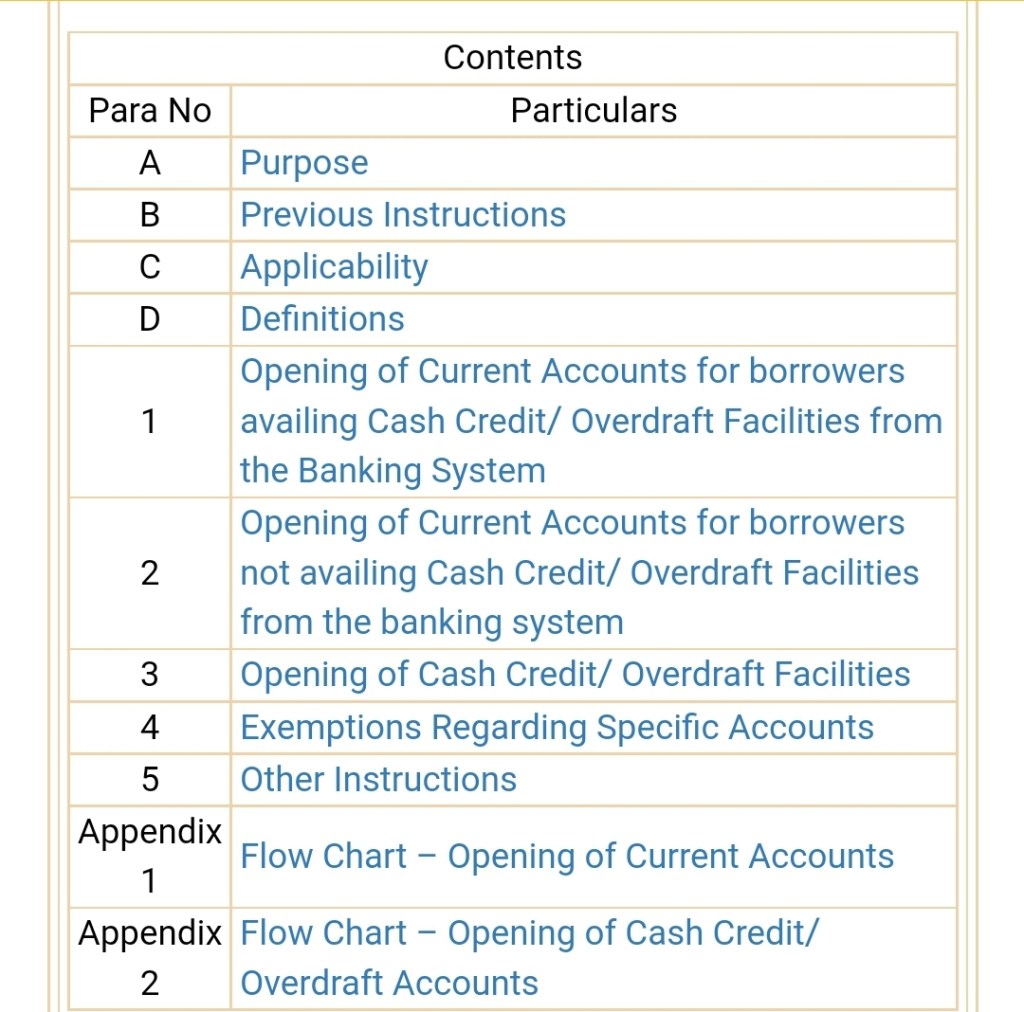

This Circular consolidates earlier instructions issued by the Reserve Bank of India, on opening and operation of current accounts and CC/OD accounts with a view to enforce credit discipline amongst the borrowers as well as to facilitate better monitoring by the lenders.

B. Previous Instructions

This circular consolidates instructions contained in the following circulars issued on the above subject:

The provisions of these instructions shall apply to current accounts and CC/OD accounts opened or maintained with the following Regulated Entities (REs):

All Scheduled Commercial Banks

All Payments Banks

D. Definitions

“Exposure” for the purpose of these instructions shall mean sum of sanctioned fund based and non-fund-based credit facilities availed by the borrower2. All such credit facilities carried in their Indian books shall be included for the purpose of exposure calculation.

“Banking System” for the purpose of these instructions, shall include Scheduled Commercial Banks and Payments Banks only.

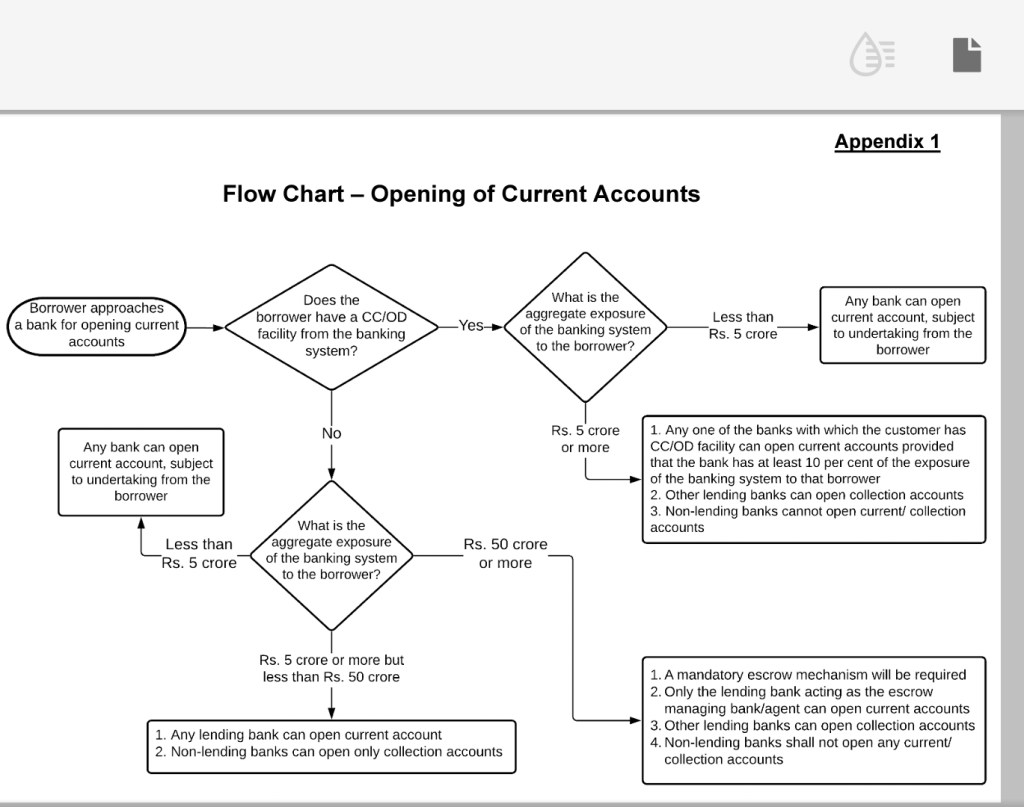

1. Opening of Current Accounts for borrowers availing Cash Credit/ Overdraft Facilities from the Banking System

1.1 For borrowers, where the aggregate exposure3 of the banking system is less than ₹5 crore, banks can open current accounts without any restrictions placed vide this circular subject to obtaining an undertaking from such customers that they (the borrowers) shall inform the bank(s), if and when the credit facilities availed by them from the banking system becomes ₹5 crore or more.

1.2 Where the aggregate exposure of the banking system is ₹5 crore or more:

1.2.1 Borrowers can open current accounts with any one of the banks with which it has CC/OD facility, provided that the bank has at least 10 per cent of the aggregate exposure of the banking system to that borrower. In case none of the lenders has at least 10 per cent of the aggregate exposure, the bank having the highest exposure among CC/OD providing banks may open current accounts.

1.2.2 Other lending banks may open only collection accounts subject to the condition that funds deposited in such collection accounts will be remitted within two working days of receiving such funds, to the CC/OD account maintained with the above-mentioned bank (para 1.2.1) maintaining current accounts for the borrower. The balances in such collection accounts shall not be used for repayment of any credit facilities provided by the bank, or as collateral/ margin for availing any fund or non-fund based credit facilities. However, banks maintaining collection accounts are permitted to debit fees/ charges from such accounts before transferring funds to CC/OD account.

1.2.3 Non-lending banks are not permitted to open current/ collection accounts.

2. Opening of Current Accounts for borrowers not availing Cash Credit/ Overdraft Facilities from the banking system

2.1 In case of borrowers where aggregate exposure of the banking system is ₹50 crore or more:

2.1.1 Banks shall be required to put in place an escrow mechanism. Borrowers shall be free to choose any lending bank as their escrow managing bank. All lending banks should be part of the escrow agreement. The terms and conditions of the agreement may be decided mutually by lending banks and the borrower.

2.1.2 Current accounts of such borrowers can only be opened/ maintained by the escrow managing bank.

2.1.3 Other lending banks can open ‘collection accounts’ subject to the condition that funds will be remitted from these accounts to the said escrow account at the frequency agreed between the bank and the borrower. Further, balances in such collection accounts shall not be used for repayment of any credit facilities provided by the bank, or as collateral/ margin for availing any fund or non-fund based credit facilities. While there is no prohibition on amount or number of credits in ‘collection accounts’, debits in these accounts shall be limited to the purpose of remitting the proceeds to the said escrow account. However, banks maintaining collection accounts are permitted to debit fees/ charges from such accounts before transferring funds to the escrow account.

2.1.4 Non-lending banks shall not open any current account for such borrowers.

2.2 In case of borrowers where aggregate exposure of the banking system is ₹5 crore or more but less than ₹50 crore, there is no restriction on opening of current accounts by the lending banks. However, non-lending banks may open only collection accounts as detailed at para 2.1.3 above.

2.3 In case of borrowers where aggregate exposure of the banking system is less than ₹5 crore, banks may open current accounts subject to obtaining an undertaking from them that they (the customers) shall inform the bank(s), if and when the credit facilities availed by them from the banking system becomes ₹5 crore or more. The current account of such customers, as and when the aggregate exposure of the banking system becomes ₹5 crore or more, and ₹50 crore or more, will be governed by the provisions of para 2.2 and para 2.1 respectively.

2.4 Banks are free to open current accounts of prospective customers who have not availed any credit facilities from the banking system, subject to necessary due diligence as per their Board approved policies.

2.5 Banks are free to open current accounts, without

any of the restrictions placed in this Circular, for borrowers having credit facilities only from NBFCs/ FIs/ co-operative banks/ non-bank institutions, etc. However, if such borrowers avail aggregate credit facilities of ₹5 crore or above from the banks covered under these guidelines, the provisions of the Circular shall be applicable.

3. Opening of Cash Credit/ Overdraft Facilities

3.1 When a borrower approaches a bank for availing CC/OD facility, the bank can provide such facilities without any restrictions placed vide this circular if the aggregate exposure of the banking system to that borrower is less than ₹5 crore. However, the bank must obtain an undertaking from such borrowers that they (the borrowers) shall inform the bank(s), if and when the credit facilities availed by them from the banking system becomes ₹5 crore or more.

3.2 For borrowers, where the aggregate exposure of the banking system is ₹5 crore or more:

3.2.1 Banks having a share of 10 per cent or more in the aggregate exposure of the banking system to such borrower can provide CC/OD facility without any restrictions placed vide this circular.

3.2.2 In case none of the banks has at least 10 per cent exposure, bank having the highest exposure among CC/OD providing banks can provide such facility without any restrictions.

3.2.3 Where a bank’s exposure to a borrower is less than 10 per cent of the aggregate exposure of the banking system to that borrower, while credits are freely permitted, debits to the CC/OD account can only be for credit to the CC/OD account of that borrower with a bank that has 10 per cent or more of aggregate exposure of the banking system to that borrower. Funds will be remitted from these accounts to the said transferee CC/OD account at the frequency agreed between the bank and the borrower. Further, the credit balances in such collection accounts shall not be used for repayment of any credit facilities provided by the bank, or as collateral/ margin for availing any fund or non-fund based credit facilities. However, banks are permitted to debit interest/ charges pertaining to the said CC/OD account and other fees/ charges before transferring the funds to the CC/OD account of the borrower with bank(s) having 10 per cent or more of the aggregate exposure. It may be noted that banks with exposure to the borrower of less than 10 per cent of the aggregate exposure of the banking system can offer working capital demand loan (WCDL)/ working capital term loan (WCTL) facility to the borrower.

3.2.4 In case there is more than one bank having 10 per cent or more of the aggregate exposure, the bank to which the funds are to be remitted may be decided mutually between the borrower and the banks.

4. Exemptions Regarding Specific Accounts

4.1 Banks are permitted to open and operate the following accounts without any of the restrictions placed in terms of paras 1, 2 and 3 of this Circular:

(a) Specific accounts which are stipulated under various statutes and specific instructions of other regulators/ regulatory departments/ Central and State Governments. An indicative list of such accounts is given below:

Accounts for real estate projects mandated under Section 4 (2) l (D) of the Real Estate (Regulation and Development) Act, 2016 for the purpose of maintaining 70 per cent of advance payments collected from the home buyers

Nodal or escrow accounts of payment aggregators/ prepaid payment instrument issuers for specific activities as permitted by Department of Payments and Settlement Systems (DPSS), Reserve Bank of India under Payment and Settlement Systems Act, 2007

Accounts for the purpose of IPO/ NFO/ FPO/ share buyback/ dividend payment/ issuance of commercial papers/ allotment of debentures/ gratuity etc. which are mandated by respective statutes or by regulators and are meant for specific/ limited transactions only

(b) Accounts opened as per the provisions of Foreign Exchange Management Act, 1999 (FEMA) and notifications issued thereunder including any other current account if it is mandated for ensuring compliance under the FEMA framework

(c) Accounts for payment of taxes, duties, statutory dues, etc. opened with banks authorized to collect the same, for borrowers of such banks which are not authorized to collect such taxes, duties, statutory dues, etc.

(d) Accounts for settlement of dues related to debit card/ ATM card/ credit card issuers/ acquirers

(e) Accounts of White Label ATM Operators and their agents for sourcing of currency

(f) Accounts of Cash-in-Transit (CIT) Companies/ Cash Replenishment Agencies (CRAs) for providing cash management services

(g) Accounts opened by a bank funding a specific project for receiving/monitoring cash flows of that specific project, provided the borrower has not availed any CC/OD facility for that project

(h) Inter-bank accounts

(i) Accounts of All India Financial Institutions (AIFIs), viz., EXIM Bank, NABARD, NHB, and SIDBI

(j) Accounts attached by orders of Central or State governments/ regulatory body/ Courts/ investigating agencies etc. wherein the customer cannot undertake any discretionary debits

4.2 Banks maintaining accounts listed in para 4.1 shall ensure that these accounts are used for permitted/ specified transactions only. Further, banks shall flag these accounts in the CBS for easy monitoring. Lenders to such borrowers may also enter into agreements/ arrangements with the borrowers for monitoring of cash flows/ periodic transfer of funds (if permissible) in these accounts.

5. Other Instructions

5.1 In case of borrowers covered under guidelines on loan system for delivery of bank credit issued vide circular DBR.BP.BC.No.12/21.04.048/2018-19 dated December 5, 2018, bifurcation of working capital facility into loan component and cash credit component shall continue to be maintained at individual bank level in all cases, including consortium lending

5.2 All banks, whether lending banks or otherwise, shall monitor all accounts regularly, at least on a half-yearly basis, specifically with respect to the aggregate exposure of the banking system to the borrower, and the bank’s share in that exposure, to ensure compliance with these instructions. If there is a change in exposure of a particular bank or aggregate exposure of the banking system to the borrower which warrants implementation of new banking arrangements, such changes shall be implemented within a period of three months from the date of such monitoring.

5.3 Banks shall put in place a monitoring mechanism, both at head office and regional/ zonal office levels to monitor non-disruptive implementation of the circular and to ensure that customers are not put to undue inconvenience during the implementation process.

5.4 Banks should not route drawal from term loans through CC/ OD/ Current accounts of the borrower. Since term loans are meant for specific purposes, the funds should be remitted directly to the supplier of goods and services. In cases where term loans are meant for purposes other than for supply of goods and services and where the payment destination is identifiable, banks shall ensure that payment is made directly, without routing it through an account of the borrower. However, where the payment destination is unidentifiable, banks may route such term loans through an account of the borrower opened as per the provisions of the circular. Expenses incurred by the borrower for day-to-day operations may be routed through an account of the borrower.