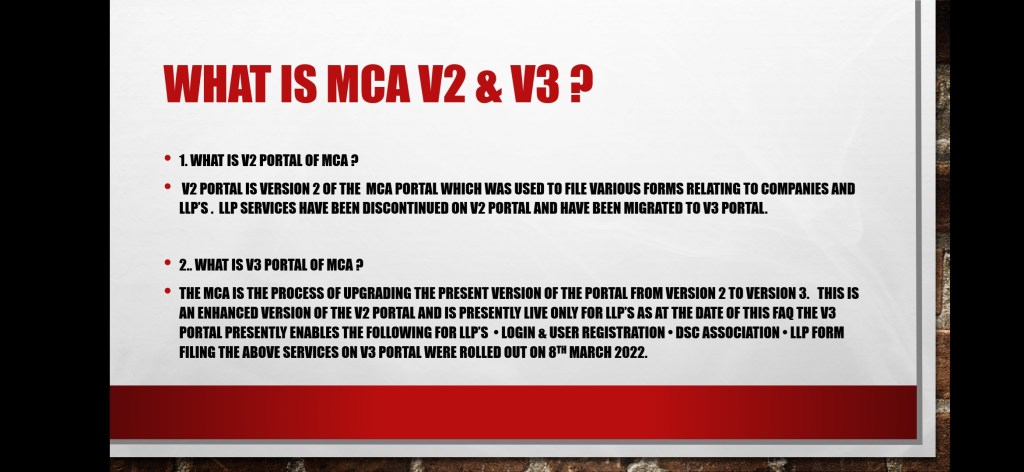

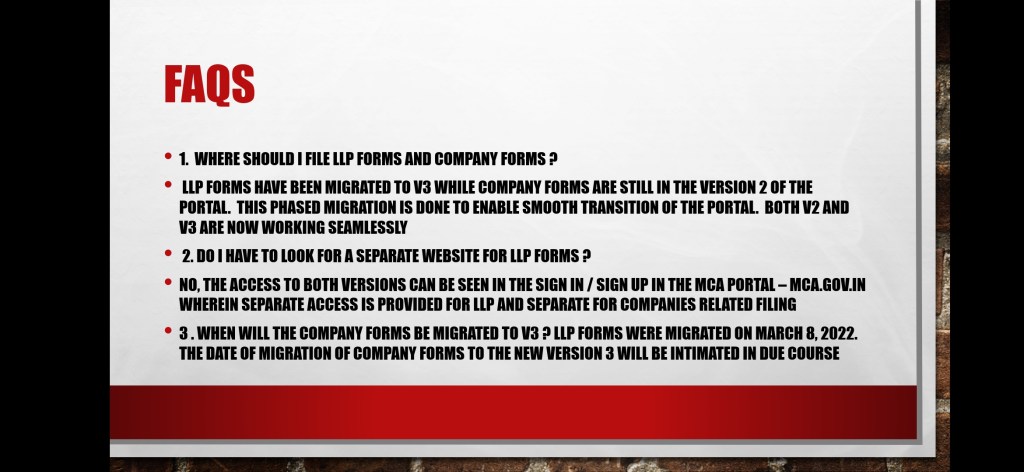

MCA V2 version Vs MCA V3 version (MCA updates 01st April 2022)

Simplifying your business ideas, structures, functionalities, relations & operations

MCA V2 version Vs MCA V3 version (MCA updates 01st April 2022)

Accountability in higher judiciary is maintained through “in-house mechanism”. The Supreme Court of India, in its full Court meeting on 7thMay, 1997, adopted two Resolutions namely (i) ‘The Restatement of Values of Judicial Life” which lays down certain judicial standards and principles to be observed and followed by the Judges of the Supreme Court and High Courts (ii) “in-house procedure’ for taking suitable remedial action against judges who do not follow universally accepted values of Judicial life including those included in the Restatement of Values of Judicial life.

As per the established “In-house procedure’ for the Higher Judiciary, the Chief Justice of India is competent to receive complaints against the conduct of Judges of the Supreme Court and the Chief Justices of the High Courts. Similarly, the Chief Justices of the High Courts are competent to receive complaints against the conduct of High Court Judges. The complaints/representations received are forwarded to the Chief Justice of India or to the Chief Justice of the concerned High Court, as the case may be, for appropriate action.

During last 05 years (from 01.01.2017 to 31.12.2021), 1631 complaintswere received in the Centralised Public Grievance Redress and Monitoring System (CPGRAMS) on the functioning of the judiciary including judicial corruption and forwarded to the CJI/Chief Justice of High Courts, respectively, as per the procedure established under “in-house mechanism”.

This information was given by the Union Minister of Law and Justice, Shri Kiren Rijiju in a written reply in Lok Sabha today.

Ministry of Law and Justice Press release April 1, 2022

Chapter 9 of the Manual of the Parliamentary Procedures in the Government of India provides procedures for legislation and the Legislative Department follows the procedure stated in that Manual while drafting laws. The Ministry/ Department to whom a subject matter is allocated under the Government of India (Allocation of Business) Rules, 1961 formulates the legislative proposals in consultation with experts and stake holders as well as all interested persons and authorities concerned. The Legislative Department prepares draft laws in consultation with the administrative Ministry concerned in accordance with the procedure laid down in the Manual of Parliamentary Procedures, ordinarily within thirty days from the date of receipt of the proposal and after clearance from the Department of Legal Affairs. During a meeting of Department-related Parliamentary Standing Committee the then Secretary, Legislative Department pointed out that many a times proposals are sent by the administrative Ministry very late, giving little or no room to examine them from legal and drafting angle. On every such occasion the administrative Departments are suitably advised verbally by the Legislative Department not to submit the proposal at the last moment, since such action compromises the quality of legislative drafting.

This information was given by the Union Minister of Law and Justice, Shri Kiren Rijiju in a written reply in Lok Sabha today.

Ministry of Law and Justice dated 01st April 2022

The sanctioned judge strength of the Supreme Court is 34 (including Chief Justice of India). As on 25.03.2021, 32 Judges are in position, leaving 02 vacancies to be filled. The Supreme Court (Number of Judges) Act 1956, as originally enacted, provided for the maximum number of Judges(excluding the Chief Justice of India) to be 10. This number was increased to 13 by the Supreme Court (Number of Judges), Amendment Act, 1960, and to 17 by the Supreme Court (Number of Judges) Amendment Act, 1977. The SupremeCourt (Number of Judges) AmendmentAct, 1986 augmented the strength of the Supreme Court Judges from 17 to 25 excluding the Chief Justice of India. Subsequently, the Supreme Court (Number of Judges) Amendment Act, 2009 further augmented the strength of the SupremeCourtJudges,from 25 to 30.

The Chief Justice of India vide letter dated 21.6.2019 requested the Government to consider augmenting the Judge-strength in the Supreme Court appropriately. Though there has been no criteria for fixing the judge strength of the Supreme Court, in view of the number of cases pending disposal, an increase in the judge strength was considered by Government. The sanctioned strength of Supreme Court of India has been increased from 30 to 33 (excluding the Chief Justice of India) w.e.f. 09.08.2019. Thereafter, the Government has not received any further proposal for increase in the strength of Supreme Court Judges.

The Government had brought into operation the Constitution (Ninety-Ninth Amendment) Act, 2014 and the National Judicial Appointments Commission Act, 2014 w.e.f.13.04.2015. However, both the Acts were challenged in the Supreme Court. The Supreme Court vide Judgment dated 16.10.2015declaredboth the Acts as unconstitutional and void. The Collegium system as existing prior to the enforcement of the Constitution (Ninety-Ninth Amendment) Act, 2014 was declared to be operative. Subsequently, the Supreme Court vide order dated 16.12.2015 directed the Government to finalize the existing Memorandum of Procedure (MoP) by supplementing it in consultation with the Supreme Court Collegium taking into consideration eligibility criteria, transparency, establishment of secretariat and mechanism to deal with complaints. The MoP is under finalization by the Government in consultation with the Supreme Court Collegium.

This information was given by the Union Minister of Law and Justice, Shri Kiren Rijiju in a written reply in Lok Sabha today

Ministry of Law and Justice Press release dated 01 April 2022

The Government has taken several initiatives to support and protect the interest of women and other entrepreneurs through stimulus given under Aatma Nirbhar Bharat Packages to combat the impact of the COVID-19 pandemic in India. The packages comprise of schemes for various sectors of the economy and also schemes having impact across sectors. The specific initiatives taken to protect women entrepreneurs and MSMEs are as under:

Under the ECLGS Scheme as on 28.02.2022, 81.18 lakhs women beneficiaries have been provided guarantees for loan. The State-wise details are at Annexure.

This information was given by the Union Minister of Women and Child Development, Smt. Smriti Zubin Irani, in a written reply in Lok Sabha today.

Ministry of Women and Child Development Press Release dated 01 April 2022

Annexure

Financial Package To Women Entrepreneurs

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1812411&RegID=3&LID=1

The gross GST revenue collected in the month of March 2022 is ₹ 1,42,095 crore of which CGST is ₹ 25,830 crore, SGST is ₹ 32,378 crore, IGST is ₹ 74,470 crore (including ₹ 39,131 crore collected on import of goods) and cess is ₹ 9,417 crore (including ₹ 981 crore collected on import of goods). The gross GST collection in March’2022 is all time high breaching earlier record of ₹ 1,40,986 crore collected in the Month of January 2022.

The government has settled ₹ 29,816 crore to CGST and ₹ 25,032 crore to SGST from IGST as regular settlement. In addition, Centre has also settled Rs. 20,000 crore of IGST on ad-hoc basis in the ratio of 50:50 between Centre and States/UTs in this month. The total revenue of Centre and the States in the month of March 2022 after regular and ad-hoc settlements is ₹ 65646 crore for CGST and ₹ 67410 crore for the SGST. Centre also released GST compensation of ₹ 18,252 crore to States/UTs during the month.

The revenues for the month of March2022 are 15% higher than the GST revenues in the same month last year and 46% higher than the GST revenues in March 2020. During the month, revenues from import of goods was 25% higher and the revenues from domestic transaction (including import of services) are 11% higher than the revenues from these sources during the same month last year. Total number of e-way bills generated in the month of February 2022 is 6.91 crore as compared to e-way bills generated in the month of January 2022 (6.88 crore) despite being a shorter month, which indicates recovery of business activity at faster pace.

The average monthly gross GST collection for the last quarter of the FY 2021-22 has been ₹ 1.38 lakh crore against the average monthly collection of ₹ 1.10 lakh crore, ₹ 1.15 lakh crore and 1.30 lakh crore in the first, second and third quarters respectively. Coupled with economic recovery, anti-evasion activities, especially action against fake billers have been contributing to the enhanced GST. The improvement in revenue has also been due to various rate rationalization measures undertaken by the Council to correct inverted duty structure.

The chart below shows trends in monthly gross GST revenues during the current year. The table shows the state-wise figures of GST collected in each State during the month of March 2022 as compared to March 2021.

The Ministry/ Department to whom a subject matter is allocated under the Government of India (Allocation of Business) Rules, 1961 formulates the legislative proposals in consultation with experts and stake holders as well as all interested persons and authorities concerned. The Legislative Department prepares draft laws in consultation with the administrative Ministry concerned in accordance with the procedure laid down in the Manual of Parliamentary Procedures.

Chapter 9 of the Manual of the Parliamentary Procedures in the Government of India provides procedures for legislation and the Legislative Department follows the procedure stated in that Manual while drafting laws.

Paragraph 9.3 of Chapter 9 of the Manual of the Parliamentary Procedures provides as under:-

“The Ministry of Law and Justice (Legislative Department) will prepare a draft Bill ordinarily within 30 days from the date of receipt of the proposal after clearance from the Department of Legal Affairs, unless any clarifications are required or it is not possible to do so for contingencies such as the draftsman being busy with budget proposals etc., on the basis of the material made available by the concerned Ministry/Department, holding discussions with the officers of that Ministry/Department for getting various aspects of the Bill clarified, wherever considered necessary”.

This information was given by the Union Minister of Law and Justice, Shri Kiren Rijiju in a written reply in Rajya Sabha, today.

On consideration of difficulties in electronic filing of Form No.10AB as stipulated in Rule 2C or 11AA or 17A of the Income-tax Rules, 1962, the Central Board of Direct Taxes (CBDT), extends the last date for electronic filing of Form No.10AB.

The application for registration or approval under Section 10(23C), 12A or 80G of the Act in Form No.10AB, for which the last date for filing falls on or before 29th September, 2022, is extended to 30th September, 2022.

CBDT’s Circular No.08/2022 in F. No. 197/59/2022-ITA-I dated 31.03.2022 has also been issued.

The Income Tax Department conducted a search and seizure operation on a leading automobile manufacturer group along with a company operating chartered flights and a real estate group of Delhi-NCR covering more than 35 premises across Delhi-NCR, on 23.03.2022.

During the course of the search operation, various incriminating documents and digital evidence have been found and seized indicating that the expenses ostensibly shown to have been claimed towards business purposes are not fully supported by evidences. Expenditure aggregating to more than Rs. 800 crore has been booked in the guise of purchase of services from a specific event management entity. This entity has siphoned-off the money by way of layering. Such claims towards non-business purposes are inadmissible expenditure under the provisions of the Income-tax Act, 1961.

In the search, it was also found that 10 acres of farm land at Delhi was purchased through few paper companies. In such transactions, unaccounted cash component of over Rs. 60 crore was purportedly involved. The ultimate/ real beneficiary of the land deal is a prominent person of the automobile manufacturer group. The intermediary who facilitated the said deal has admitted in his statement that major part of the sale consideration was paid in cash.

Apart from this, several incriminating documents have been unearthed from the premises of persons involved in the real estate business. These contain records of on-money transactions where cash was being received in lieu of sale of units in their various real estate projects across Delhi.

In the case of the company operating chartered flights, evidence related to booking of bogus expenses and non-recognition of income totalling to over Rs. 50 crore, rotation of funds and suspicious loans through a dubious NBFC floated by a key person, layering and re-routing of funds through paper companies and claiming bogus interest expenses, etc. have also been unearthed.

Undisclosed cash exceeding Rs. 1.35 crore has been seized and jewellery over Rs. 3 crore has been kept provisionally under restraint.

Further investigations are in progress.

The Central Board of Direct Taxes (CBDT) has entered into 62 Advance Pricing Agreements (APA) in FY 2021-22 with Indian taxpayers. This includes 13 Bilateral APAs (consequent to Mutual Agreement between India and its treaty partners) and 49 Unilateral APAs. With this, the total number of APAs since inception of the APA program has gone up to 421.

Despite severe economic and social disruption caused by the CoVID-19 pandemic in first part of the financial year, the number of APAs signed compares very well with the APAs signed in the preceding two years (31 APAs in FY 2020-21 and 57 APAs in FY 2019-20).

The APA Scheme endeavours to provide certainty to taxpayers in the domain of transfer pricing by specifying the methods of pricing and determining the arm’s length price of international transactions in advance for the maximum of five future years. Further, the taxpayer has the option to rollback the APA for four preceding years, as a result of which, total nine years of tax certainty is provided.

The progress of the APA scheme strengthens the Government’s resolve of fostering a non-adversarial tax regime and increasing the ease of doing business in India. CBDT appreciates the cooperative and transparent attitude of taxpayers in this regard.