Supreme Court Dismisses Bharti Air-tel’s Plea For Refund of Rs.923 Crore

Union of India Vs Bharti Airtel Ltd. & Ors (Supreme Court of India) dated 28 Oct 2021

Download judgement copy

Simplifying your business ideas, structures, functionalities, relations & operations

Supreme Court Dismisses Bharti Air-tel’s Plea For Refund of Rs.923 Crore

Union of India Vs Bharti Airtel Ltd. & Ors (Supreme Court of India) dated 28 Oct 2021

Download judgement copy

No section 271D Penalty on wife for receiving money from husband for purchase of family property

Smt. Meera Devi Kumawat Vs JCIT (ITAT Jaipur): ITA No. 1201/JP/2019 dated 21/10/2021

TPO duty bound to determine ALP by following any one of prescribed methods

Firemenich Aromatics Production (India) Pvt. Ltd. Vs ACIT (ITAT Mumbai) dated 26/10/2021

Section 36 deduction permitted if expenditure is not for extension of business activity

CIT Vs Ceebros Hotels P Ltd. (Madras High Court) dated 05/10/2021

Depreciation allowable on home-theatre used for business purpose

DCIT Vs Tally Solutions Pvt. Ltd. (ITAT Bangalore) dated 14/10/2021

If AO made addition on estimated GP basis than other item-wise disallowance should not be made

Devyani Tex Chem Pvt. Ltd. Vs ACIT (ITAT Surat) dated 22/06/2021

Deemed dividend not attracted on Loan Taken on interest

DCIT Vs Heilgers Development & Construction Company Pvt. Ltd (ITAT Kolkata) dated 18/08/2021

Activity of Providing Affordable Housing by MHADA is Charitable in Nature

Maharashtra Housing & Area Development Authority (MHADA) Vs DCIT (ITAT Mumbai) dated 13/10/2021

ROC expense for enhancement of share capital not allowable

Moldtek Packaging Ltd. Vs ACIT (ITAT Hyderabad) dated 02/07/2021

Addition under section 69A unsustainable for cash deposited as facilitator

Ashish Natvarlal Vashi Vs ITO (ITAT Surat) dated 11/05/2021

Regards,

Bipul Kumar

Finance Secretary Dr T.V. Somanathan releases Model Tender Documents (MTDs) for Procurement of Goods and non-Consultancy Services

MTDs specifically cater to needs of e-procurement, easing digitization process of Public Procurement & help in achieving goal of Digital IndiaPosted Date

वित्त सचिव डॉ. टी वी सोमनाथन ने वस्तुओं और गैर-परामर्श सेवाओं की खरीद के लिए मॉडल निविदा दस्तावेज (एमटीडी) जारी किए

एमटीडी से विशेषकर ई-खरीद की जरूरतें पूरी होती हैं, सार्वजनिक खरीद की डिजिटलीकरण प्रक्रिया आसान हो जाती है और डिजिटल इंडिया के लक्ष्य को प्राप्त करने में मदद मिलती है

Finance Secretary & Secretary Expenditure, Dr T.V. Somanathan here today released Model Tender Documents (MTDs) for Procurement of Goods and non-Consultancy Services as part of continuous process of review of existing rules & procedures as emphasised by the Hon’ble Prime Minister in his Independence Day speech this year.

MTDs specifically cater to needs relating to e-procurement thereby easing the process for adoption of e-procurement and furthering the ambition of convenient and efficient e-governance of the Government. Such initiatives shall help in achieving the goal of Digital India by easing and standardising the digitization process of Public Procurement.

Tender documents are the critical touch point for the Government with industry and are, therefore, a critical vehicle for implementing policy initiatives on the ground. Uniform sets of tender documents permit Government to express its policies effectively, consistently and uniformly. Uniformity in interpretation and application of public procurement policies and initiatives reflect clarity of application, thereby, increasing compliance and enhancing public confidence in procurement process. Further, apart from sharing best procurement practices, uniform tender documents amplify the positive impact of policy initiatives, bringing economies of scale and increasing competition. They create more efficient market conditions for realising value for tax payers money. Bidders also get broader market access for their products.

Accordingly, Model Tender Documents (MTDs) have now been developed for the procurement of Goods and non-Consultancy Services. These MTDs rationalise and simplify the structure of tender documents. Besides aligning provisions with various procurement policies of the Government, like policies related to Micro and Small Enterprises, preference to Make in India and benefits to Start-ups, MTDs incorporate national and international best practices. The MTDs have been developed after a two stage, extensive consultation with Ministries/ Departments/ Central Public Sector Undertakings, other organisations and individual experts.

MTDs issued by the Department of Expenditure , Ministry of Finance will be guiding templates . In keeping with the Government’s Digital India thrust, the MTDs are being issued in soft template for enabling easy customisation by user departments. Ministries/ Departments shall be competent to suitably customise this document to suit their local/ specialised needs. A separate detailed Guidance Note, as a guide to use of each MTD has also been prepared to help the procuring officials in utilising each MTD. Model Tender Documents, issued by Department of Expenditure (DoE), Ministry of Finance, will be guiding templates.

Government organisations procure various goods and non-consulting services in order to comply with their duties and responsibilities. To improve good governance, transparency, fairness, competition, and value for money in public procurement, the Government of India has taken a number of significant policy initiatives in public procurement in the recent past. The General Financial Rules were issued after comprehensive review in March, 2017. Additionally three procurement Manuals, the Manual for Procurement of Goods, 2017, Manual for Procurement of Consultancy and Other Services, 2017 and Manual for Procurement of Works, 2019, have also been developed.

The formulation and release of these Model Tender Documents are a part of continuous process of review of existing rules and procedures and being monitored by Cabinet Secretary as a special campaign during 2nd October, 2021 to 31st October, 2021.

Documents Links:

Finance Secretary Dr T.V. Somanathan releases guidelines for reforms in Public Procurement and Project Management

Guidelines attempt to incorporate into the realm of Public Procurement, innovative rules for faster, efficient and transparent execution of projectsPosted Date:- Oct 29, 2021

Finance Secretary & Secretary Expenditure, Dr T.V. Somanathan released guidelines to usher in reforms in Public Procurement and Project Management here today. The formulation and release of these guidelines is a part of continuous process of review of existing rules and procedures as emphasised by the Hon’ble Prime Minister during his Independence Day address this year. This is being monitored by Cabinet Secretary as a special campaign during 2nd October, 2021 to 31st October, 2021.

The draft of the guidelines was prepared under the aegis of the Central Vigilance Commission (CVC) after a detailed consultative process involving experts from various fields of public procurement and project management. The Department of Expenditure (DoE), Ministry of Finance, was nominated to issue the guidelines after soliciting and detailed consideration of the comments of Ministries/ Departments.

These guidelines attempt to incorporate into the realm of Public Procurement in India, innovative rules for faster, efficient and transparent execution of projects and to empower executing agencies to take quicker and more efficient decision in public interest. Some of the improvements include prescribing strict timelines for payments when due. Timely release of ad hoc payments (70% or more of bills raised) is expected to improve liquidity with the contractors especially Micro, Small and Medium Enterprises (MSMEs).

As part of Government’s Digital thrust, Electronic Measurement Books have been prescribed as a means of recording progress of works. This system, along with other IT based solutions, proposed in the guidelines, will help in realising the dream of efficient Digital India, facilitate faster payments to contractors and reduce disputes.

Alternative methods for selection of contractors have been permitted, which can improve speed and efficiency in execution of projects. In appropriate cases, quality parameters can be given weightage during evaluation of the proposal in a transparent and fair manner, through a Quality cum Cost Based Selection (QCBS), as an alternative to traditional L1 system.

Executing public projects on time, within the approved cost and with good quality has always been a challenge. As the pace of economic development steps up careful examination of procedures and rules is essential to ensure unwarranted roadblocks are removed and new innovations utilized for increasing value for money of the taxpayer.

The Central Vigilance Commission (CVC), the Comptroller & Auditor General (CAG) and the National Institution for Transforming India (NITI) Aayog had carried out detailed analysis of the procedures and rules for public procurement and project management and had suggested changes in strategies to meet challenges of present and future public procurement.

Order Link:

****

RM/KMN

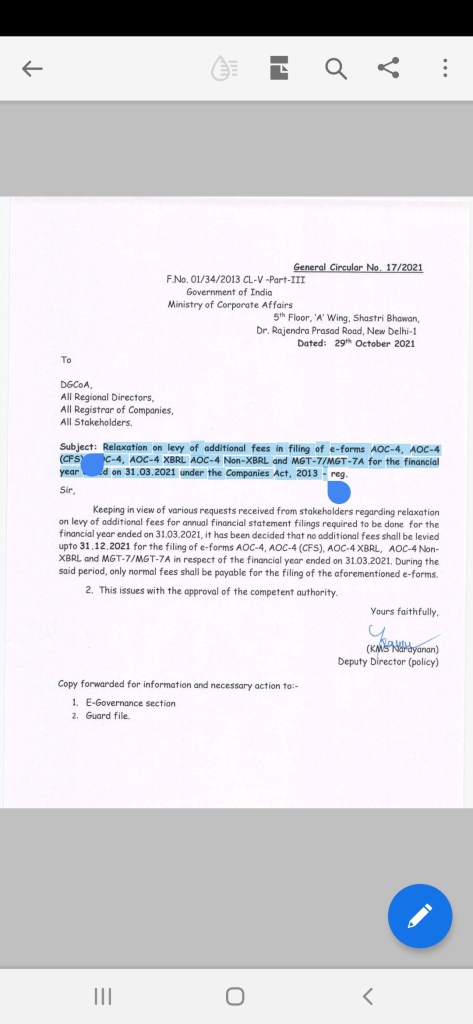

*Relaxation of additional fees of e form AOC 4, AOC 4 (CFS), AOC 4 (Xbrl), non xbrl, MGT 7/7A till 31.12.2021*

Please note in case of one day delay from 31.12.2021, additional fees will be leviable from original event date.

Summary Order in GST DRC-07 quashed by Patna HC for violating principles of natural justice

K. R. Steel Traders Vs State of Bihar (Patna High Court) dated 21/10/2021

Bombay HC directs GST Authority to process Application for IGST Refund as no order was passed

Evertime Overseas Private Limited Vs Union of India and ors. (Bombay High Court) dated 08/10/2021

No ITC on gifts to retailers for personal consumption for sales promotion

In re GRB Dairy Foods Pvt. Ltd (GST AAR Tamilnadu) dated 30/09/2021

It is illegal to attach Director’s personal property for recovery of sales tax dues

Manharlal Hirjibhai Virdiya Vs Assistant Commissioner of Commercial Tax (Gujarat High Court) dated 08/10/2021

18% GST payable on Electronic Toys

In re Joshna ChandresJ1 Shah (GST AAR Tamilnadu) dated 30/09/2021

GST not Payable on Ambulances Services to MCGM

In re Geetee Tours Private Limited (GST AAR Maharashtra) dated 25/10/2021

ITC cannot be availed on second hand car if applicant opted for concessional rate

In re Deccan Wheels (GST AAR Maharashtra) dated 25/10/2021

Recipient of services/Goods or both cannot apply for advance ruling

In re Godavari Marathwada Irrigation Development Corporation (GST AAR Maharashtra) dated 25/10/2021

18% GST Payable on activity of reshelling of old sugar mill rollers

In re S.B. Reshellers Pvt.Ltd. (GST AAR Maharashtra) dated 25/10/2021

Regards

Bipul Kumar

Download judgment copy:

The Ministry of Finance has released ₹44,000 crore today to the States and UTs with Legislature under the back-to-back loan facility in lieu of GST Compensation. After taking into account earlier release of ₹ 1,15,000 crore (₹ 75,000 crore released on 15th July, 2021 and ₹ 40,000 crore released on 07th October, 2021), total amount released in the current financial year as back-to-back loan in-lieu of GST compensation is ₹1,59,000 crore. This release is in addition to normal GST compensation being released every 2 months out of actual cess collection.

Subsequent to the 43rd GST Council Meeting held on 28.05.2021, it was decided that the Central Government would borrow ₹1.59 lakh crore and release it to States and UTs with Legislature on a back-to-back basis to meet the resource gap due to the short release of Compensation on account of inadequate amount in the Compensation Fund. This amount is as per the principles adopted for a similar facility in FY 2020-21, where an amount of ₹1.10 lakh crore was released to States under a similar arrangement. This amount of ₹1.59 lakh crore would be over and above the compensation in excess of ₹1 lakh crore (based on cess collection) that is estimated to be released to States/UTs with Legislature during this financial year. The sum total of ₹2.59 lakh crore is expected to exceed the amount of GST compensation accruing in FY 2021-22.

All eligible States and UTs (with Legislature) have agreed to the arrangements of funding of the compensation shortfall under the back-to-back loan facility. For effective response and management of COVID-19 pandemic and a step-up in capital expenditure all States and UTs have a very important role to play. For assisting the States/UTs in their endeavour, Ministry of Finance has frontloaded the release of assistance under the back-to-back loan facility during FY 2021-22 of ₹1,59,000 crore.

The release of ₹44,000 crore being made now is funded from borrowings of GoI in 5-year securitiesissued in the current financial year, at a Weighted Average Yield of 5.69%. No additional market borrowing by Central Government is envisaged on account of this release.

It is expected that this release will help the States/UTs in planning their public expenditure among other things, for improving, health infrastructure and taking up infrastructure projects.

****

State/ UTs wise amount released as “Back to Back Loan in lieu of GST Compensation Shortfall” on 28.10.2021

Refer link

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1767194&RegID=3&LID=1

The Gurugram Zonal Unit (GZU) of Directorate General of GST Intelligence (DGGI) has arrested three persons under the provisions of the GST Act on charges of running multiple fake firms on the strength of fake documents in two different cases.

Two persons were arrested from Delhi on 5th and 9th October 2021 on charges of orchestrating a fake billing racket involving more than 20 fake firms where more than Rs 22 crore of fraudulent input tax credit was taken thereby defrauding the exchequer. Both persons were arrested and produced before CMM, Delhi, and were subsequently sent to 14 days Judicial Custody.

In another case of fake billing a resident of Pataudi, Haryana, was also arrested. He was found to be in possession of huge cache of incriminating documents like fake stamps of Government Departments, cheque books and ATMs of multiple fake firms, toll receipt book, “Dharam Kanta” or Weighing station booklets, fictitious transporters booklets etc. The same were being used to show evidence of fake supply of goods on which fake input tax credit was generated and passed on through these slew of fake firms.

Based on the evidence, the person was arrested on 23rd October 2021 under the provisions of the GST Act on charges for defrauding the Government of more than Rs 26 crore of GST. The arrested person has been sent to 14 days Judicial Custody.

Further investigations in both the cases are underway.

SC: Nature of levy cannot be determined with nomenclature ascribed to Tax

Jalkal Vibhag Nagar Nigam dated SC 22 Oct 2021

Opinion under Section 83 of CGST Act should be strictly based upon material facts

Mutharamman & Co. (Madras HC dated 05/10/2021)

Section 12AA registration cannot be denied without examining the activities

ICRW Group Gratuity Trust Vs CIT (Exemption) (ITAT Delhi) dated 21/10/2021

ITAT explains basic conditions for Satisfaction of reimbursement Claim

Rieter Machine Works Limited Vs ACIT (ITAT Pune) dated 21/10/2021

No attribution of profit in absence of permanent establishment

ESPN Star Sports Mauritius Vs DCIT (ITAT Delhi) dated 20/10/2021

HC dismisses writ petition as petitioner is having alternative statutory remedy of appeal

Ankit Gupta Vs National Faceless Assessment Centre (Rajasthan High Court) dated 21/10/2021

Sec 138 NI Act: Complaint comes to an end Once Accused & Complainant Enter into a Settlement Agreement: SC

Gimpex Private Limited Vs Manoj Goel (Supreme Court of India) dated 08/10/2021

Authorities shall provide opportunity of hearing before arriving at any figure in demand Notice

Golden Trees Plantation Limited Vs Securities And Exchange Board of India (Gujarat High Court) dated 06/09/2021

Calculating limitation period for proceedings under IBC?

V Nagarajan Vs SKS Ispat and Power Ltd.& Ors. (Supreme Court of India) dated 21/10/2021

HC asks govt to keep vigil on ‘Rising Frauds in Aadhaar Enrollment

Naresh Kumar R.P. Vs State of Karnataka (Karnataka High Court) dated 30/09/2021

Benami Act, 1988, would not extend to properties purchased by the company

Kalyan Buildmart Pvt. Ltd. Vs Initiating Officer (Rajasthan High Court) dated 06/10/2021

Regards

Bipul Kumar