Centre Revises “Transport and Marketing Assistance” (TMA) scheme for Specified Agriculture Products’

Dairy products, which were not covered under the earlier scheme, will be eligible for assistance

Rates of assistance have been increased, by 50% for exports by sea and by 100% for exports by air Posted Date:- Sep 10, 2021

Centre has revised “Transport and Marketing Assistance” (TMA) scheme for Specified Agriculture Products’.

In February 2019, the Department of Commerce had introduced ‘Transport and Marketing Assistance (TMA) for Specified Agriculture Products Scheme’ to provide assistance for the international component of freight, to mitigate disadvantage of higher freight costs faced by the Indian exporters of agriculture products. The scheme was initially applicable for exports effected during the period from 01.03.2019 to 31.03.2020 and was later extended for exports effected up to 31.03.2021.

Now the Department has notified ‘Revised Transport and Marketing Assistance (TMA) for Specified Agriculture Products Scheme’ for exports effected on or after 01.04.2021 up to 31.03.2022. The existing scheme will remain in operation for exports effected up to 31.03.2021.

Following major changes have been made in the revised scheme:

• Dairy products, which were not covered under the earlier scheme, will be eligible for assistance under the revised scheme.

• Rates of assistance have been increased, by 50% for exports by sea and by 100% for exports by air. Details are as under:

Rates of Assistance (in INR)

Region Amount Per TEU (Normal) Amount Per TEU (Reefer)By Air

(Amount per kilogram)

ExistingRevisedExistingRevisedExistingRevised

West Africa 11200 16800 19600 29400 0.841.68

East Africa 11200 16800 21000 315000.841.68

Europe 9800 14200 21000 31500 1.122.24

Gulf 8400 12600 14000 21000 0.701.40

North America21000 31500 28700 43050 2.805.60

ASEAN 5600 8400 12600 18900 0.701.40

Russia & CIS 12600 18900 22400 33600 0.701.40

Far East 8400 12600 12250 18375 0.841.68

Oceana 16800 25200 24500 36750 2.805.60

China 0012600189000.84 1.68

South America23800 35700 31500 47250 3.507.00

The Directorate General of Foreign Trade (DGFT) will shortly notify the procedure for availing assistance under the revised scheme.

Enhanced assistance under the revised scheme is expected to help Indian exporters of agricultural products to meet rising freight and logistics costs.

Ministry of Commerce & Industry Press Release dated 10th Sept 2021

Rs. 56,027 crore is going to be released under various Export Promotion Schemes

Benefits would be disbursed to more than 45,000 exporters, out of which about 98% are small exporters in the MSME category.

Centre has provided a massive relief to the exporters.

This amount is over and above duty remission of Rs 12,454 crore for the RoDTEP scheme and Rs 6,946 crore for RoSCTL scheme already announced

Benefits would help sectors to maintain cash flows and meet export demand in international market

This support would have a multiplier effect and spur employment generation

Robust export growth is being witnessed in recent months and this decision will lead to an even more rapid export growth in coming months

Under the decisive leadership of Hon’ble Prime Minister Shri NarendraModi, Government of India has decided to budget Rs 56,027 crore in this Financial Year FY 21-22 itself in order to disburse all pending export incentives due to exporters. This amount includes claims relating to MEIS, SEIS, RoSL, RoSCTL, other scrip based schemes relating to earlier policies and the remission support for RoDTEP and RoSCTL for exports made in the 4th quarter of FY 20-21. Benefits would be disbursed to more than 45,000 exporters, out of which about 98% are small exporters in the MSME category.

The amount of Rs 56,027 crores of arrears is for different export promotion and remission schemes: MEIS (Rs 33,010 crore), SEIS (Rs 10,002 crore), RoSCTL (Rs 5,286 cr), RoSL (Rs 330 crore), RoDTEP (Rs 2,568 crore), other legacy Schemes like Target Plus etc (Rs 4,831 crore). This amount is over and above duty remission amount of Rs 12,454 crore for the RoDTEP scheme and Rs 6,946 crore for RoSCTL scheme already announced for exports made in this year i.e. FY 2021-22.

Exports in India have seen robust growth in recent months. Merchandise exports for April-August, 2021 was nearly $164 billion, which is an increase of 67% over 2020-21 and 23% over 2019-20. This decision to clear all pending export incentives within this financial year, will lead to even more rapid export growth in coming months.

For merchandise exports, all sectors covered under MEIS, such as Pharmaceuticals, Iron and steel, Engineering, Chemicals, Fisheries, Agriculture and allied Sectors, Auto and Auto Components would be able to claim benefits for exports made in earlier years. Benefits would help such sectors to maintain cash flows and meet export demand in international market, which is recovering fast this financial year.

Service sector exporters, including those in the travel, tourism and hospitality segments will be able to claim SEIS benefits for FY 2019-2020, for which Rs 2,061 crore has been provisioned. The SEIS for FY 2019-20 with certain revisions in service categories and rates is being notified. This support would have a multiplier effect and spur employment generation.

The apparel sector, which is a major labour-intensive sector, would get past arrears under ROSCTL and ROSL, and all stakeholders in the interconnected supply chains would be strengthened to meet the festive season demand in international markets.

Export claims relating to earlier years will need to be filed by the exporters by 31st December 2021 beyond which they will become time barred. The Online IT portal will be enabled shortly to accept MEIS and other scrip based applications and would be integrated with a robust mechanism set up by Ministry of Finance to monitor provisioning and disbursement of the export incentives under a budgetary framework.

A decision to clear all pending export incentives within this Financial Year itself despite other budgetary commitments arising out of the pandemic is with the objective of providing timely and crucial support to this vital pillar of Indian economy.

***

DJN

Ministry of Commerce & Industry Press Release dated 09 Sept 2021

Finance Act, 2021 has amended section 72A of the Income-tax Act, 1961 (the Act) to inter alia provide that in case of an amalgamation of a public sector company (PSU) which ceases to be a PSU (erstwhile public sector company), as part of strategic disinvestment, with one or more company or companies, then, subject to the conditions laid therein, the accumulated loss and the unabsorbed depreciation of the amalgamating company shall be deemed to be the loss, or as the case may be, allowance for unabsorbed depreciation of the amalgamated company for the previous year in which the amalgamation was effected.

In order to facilitate the strategic disinvestment, it has been decided that Section 79 of the Income-tax Act, 1961, shall not apply to an erstwhile public sector company which has become so as a result of strategic disinvestment. Accordingly, loss incurred in any previous year prior to, and including, the previous year of strategic disinvestment shall be carried forward and set off by the erstwhile public sector company. The above relaxation shall cease to apply from the previous year in which the company, that was the ultimate holding company of such erstwhile public sector company immediately after completion of the strategic disinvestment, ceases to hold, directly or through its subsidiary or subsidiaries, fifty-one per cent of the voting power of the erstwhile public sector company.

The term “erstwhile public sector company” and “strategic disinvestment” shall have the meaning in Explanation to clause (d) of sub-section (1) of Section 72A of the Income-tax Act, 1961.

Necessary legislative amendments for the above decision shall be proposed in due course of time.

The Income Tax Department carried out a search and seizure operation on 08.09.2021 on a group based in Ahmedabad. The group is among one of the prominent business houses of Gujarat engaged primarily in the media and real estate sectors. The media arm of the group comprises of electronics, digital as well as print media while the real estate arm comprises of affordable housing projects and urban civic infrastructure. More than 20 premises were covered in the operation.

During the course of the search operation, a large number of incriminating documents, loose sheets, digital evidences etc. have been found and seized, containing detailed records of the group’s unaccounted transactions, spread across multiple financial years. Majority of these evidences indicate huge unaccounted cash receipts in excess of Rs. 500 crore on the sale of Transferable Development Right (TDR) certificates. Evidences of on-money transactions in real estate projects and land deals, in excess of Rs. 350 crore have also been found along with corroborative documents. Incriminating evidences of unaccounted cash-based loan and interest payments/repayments worth more than Rs. 150 crore have also been found. Further, substantial incriminating evidences of unaccounted cash expenses, cash advances received and interest paid in cash has also been unearthed. So far, cash of more than Rs. 1 crore and jewelry amounting to Rs. 2.70 crore have also been seized from different premises. A large number of original documents of properties of the group acquired over the years and held in the names of several dummy individuals and cooperative housing societies have also been found.

Overall, the search and seizure operation has resulted in the detection of unaccounted transactions in excess of Rs. 1000 crore spread over various assessment years so far. 14 lockers have also been found during the course of the search operation which have been put under restraint orders.

The search operation is still continuing and further investigations are in progress.

The Income Tax Department conducted search and seizure operations on 08.09.2021 on three prominent Commission agent groups based in Punjab, covering many premises across Punjab & Haryana. These groups are also engaged in the business of running Steel Rolling Mill, cold storage, General Mills, Jewellery shop, Poultries, Rice Mills, Oil Mill, Flour Mill apart from the business of Commission Agents.

The search action revealed that these Groups are suppressing their business receipts and inflating expenses. They also do not account for most of the sums received and paid in cash. Further, certain documents showing payments of on-money in cash in acquiring immoveable properties have been recovered and seized. In one of the groups, it has been found that the purchases of fruits have been done during the harvest period at low cost, whereas the sales have been done in odd period at very high rates after storing the goods in cold storage. Similar modus operandi has been found in other Groups. Major findings are as under:

Books of accounts (Kacha Khata Bahi) in Laddo script have been found, which show substantial unaccounted transactions running into crores. These books of account are being deciphered with the help of an expert. Parallel sets of books of accounts of some of the business concerns have also been found which show suppression of gross business receipts running into crores on yearly basis.

It is found that advances in cash aggregating to crores are given to farmers and interest rates of 1.5 % to 3.00% per month is charged. The interest is received in cash and not shown in the books of account.

Cash purchase and sale related to poultry business and Rice sheller worth more than Rs. 9.00 crore has been found. Unaccounted purchases amounting to Rs. 1.29 crore have been found from one of the premises situated in Jalandhar. Details of unaccounted sales have also been found.

Two suspected benami firms in the names of employees have been unearthed, whose turnovers are in crores per year.

In one of the concerns, the main assessee has accepted that payments in violation of Section 40A(3) of the Income-tax Act, 1961 have been made running into crores over the years, by accounting the same after splitting the payments in the books of account.

In Steel Rolling Mills, discrepancy in stock of finished goods has been found and stock taking of raw material (scrap) is underway. Unaccounted stock of finished goods of more than Rs.25 lakh has been worked out as yet.

Unaccounted investment in immovable property amounting to Rs. 3.40 crore has been detected and has also been accepted by the owners of the properties covered during the search.

At some premises, the digital evidence found has been seized, analysis of which is in progress.

Diversion of business funds as interest free loans/advances to family members of one of the Groups has been detected by the search team.

Unaccounted Cash aggregating to Rs.1.70 crore has been found in these groups. Unexplained jewellery valued at Rs. 1.50 crore has been found. Unexplained stock of Flour valued at Rs.1.50 crore has also been found. Eight Bank lockers have been put under restraint, which are being operated today.

The search operation is still continuing and further investigations are in progress.

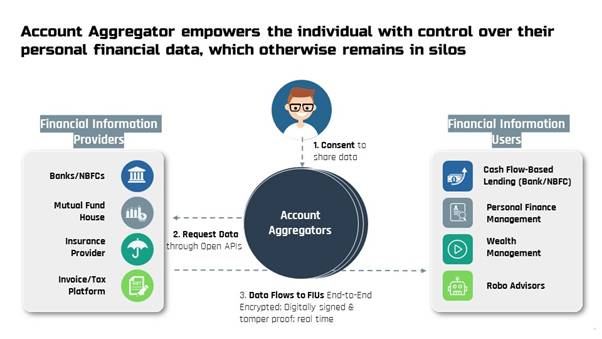

Last week India unveiled the Account Aggregator (AA) network, a financial data-sharing system that could revolutionize investing and credit, giving millions of consumers greater access and control over their financial records and expanding the potential pool of customers for lenders and fintech companies. Account Aggregator empowers the individual with control over their personal financial data, which otherwise remains in silos.

This is first step towards bringing open banking in India and empowering millions of customers to digitally access and share their financial data across institutions in a secure and efficient manner.

The Account Aggregator system in banking has been started off with eight of the India’s largest banks. The Account Aggregator system can make lending and wealth management a lot faster and cheaper.

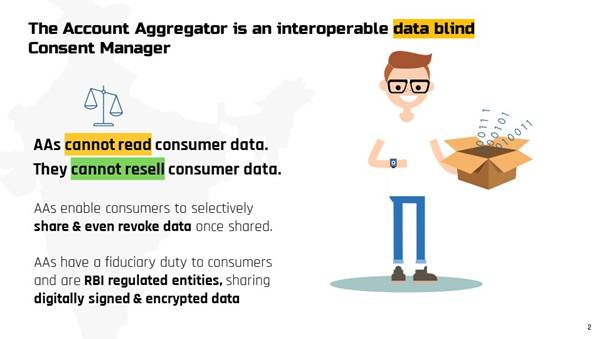

What is an Account Aggregator?

An Account Aggregator (AA) is a type of RBI regulated entity (with an NBFC-AA license) that helps an individual securely and digitally access and share information from one financial institution they have an account with to any other regulated financial institution in the AA network. Data cannot be shared without the consent of the individual.

There will be many Account Aggregators an individual can choose between.

Account Aggregator replaces the long terms and conditions form of ‘blank cheque’ acceptance with a granular, step by step permission and control for each use of your data.

2)How will the new Account Aggregator network improve an average person’s financial life?

India’s financial system involves many hassles for consumers today — sharing physical signed and scanned copies of bank statements, running around to notarise or stamp documents, or having to share your personal username and password to give your financial history to a third party. The Account Aggregator network would replace all these with a simple, mobile-based, simple, and safe digital data access & sharing process. This will create opportunities for new kinds of services — eg new types of loans.

The individual’s bank just needs to join the Account Aggregator network. Eight banks already have — four are already sharing data based on consent (Axis, ICICI, HDFC, and IndusInd Banks) and four are going to be able to shortly (State Bank of India, Kotak Mahindra Bank, IDFC First Bank, and Federal Bank).

3) How is Account Aggregator different to Aadhaar eKYC data sharing, credit bureau data sharing, and platforms like CKYC?

Aadhaar eKYC and CKYC only allow sharing of four ‘identity’ data fields for KYC purposes (eg name, address, gender, etc). Similarly, credit bureau data only shows loan history and/or a credit score. The Account Aggregator network allows sharing of transaction data or bank statements from savings/deposit/current accounts.

4) What kind of data can be shared?

Today, banking transaction data is available to be shared (for example, bank statements from a current or savings account) across the banks that have gone live on the network.

Gradually the AA framework will make all financial data available for sharing, including tax data, pensions data, securities data (mutual funds and brokerage), and insurance data will be available to consumers. It will also expand beyond the financial sector to allow healthcare and telecom data to be accessible to the individual via AA.

5) Can AAs view or ‘aggregate’ personal data? Is the data sharing secure?

Account Aggregators cannot see the data; they merely take it from one financial institution to another based on an individual’s direction and consent. Contrary to the name, they cannot ‘aggregate’ your data. AAs are not like technology companies which aggregate your data and create detailed profiles of you.

The data AAs share is encrypted by the sender and can be decrypted only by the recipient. The end to end encryption and use of technology like the ‘digital signature’ makes the process much more secure than sharing paper documents.

6) Can a consumer decide they don’t want to share data?

Yes. Registering with an AA is fully voluntary for consumers. If the bank the consumer is using has joined the network, a person can choose to register on an AA, choose which accounts they want to link, and share their data from one of their accounts for some specific purpose to a new lender or financial institution at the stage of giving ‘consent’ via one of the Account Aggregators. A customer can reject a consent to share request at any time. If a consumer has accepted to share data in a recurring manner over a period (eg during a loan period), it can also be revoked at any time later as well by the consumer.

7) If a consumer has shared my data once with an institution, for how long can they use it?

The exact time period for which the recipient institution will have access will be shown to the consumer at the time of consent for data sharing.

8) How can a customer get registered with an AA?

You can register with an AA through their app or website. AA will provide a handle (like username) which can be used during the consent process.

Today, four apps are available for download (Finvu, OneMoney, CAMS Finserv, and NADL) with operational licenses to be AAs. Three more have received in principle approval from RBI (PhonePe, Yodlee, and Perfios) and may be launching apps soon.

9) Does a customer need to register with every AA?

No, a customer can register with any AA to access data from any bank on the network.

10) Does a customer need to pay the AA for using this facility?

This will depend on the AA. Some AAs may be free because they are charging a service fee to financial institutions. Some may charge a small user fee.

11) What new services can a customer access if their bank has joined the AA network of data sharing?

The two key services that will be improved for an individual is access to loans and access to money management. If a customer wants to get a small business or personal loan today, there are many documents that need to be shared with the lender. This is a cumbersome and manual process today, which affects the time taken to procure the loan and access to a loan. Similarly, money management is difficult today because data is stored in many different locations and cannot be brought together easily for analysis.

Through Account Aggregator, a company can access tamper-proof secure data quickly and cheaply, and fast track the loan evaluation process so that a customer can get a loan. Also, a customer may be able to access a loan without physical collateral, by sharing trusted information on a future invoice or cash flow directly from a government system like GST or GeM.

On consideration of difficulties reported by the taxpayers and other stakeholders in filing of Income Tax Returns and various reports of audit for the Assessment Year 2021-22 under the Income-tax Act, 1961(the “Act”), Central Board of Direct Taxes (CBDT) has decided to further extend the due dates for filing of Income Tax Returns and various reports of audit for the Assessment Year 2021-22. The details are as under:

The due date of furnishing of Return of Income for the Assessment Year 2021-22, which was 31st July, 2021 under sub-section (1) of section 139 of the Act, as extended to 30th September, 2021 vide Circular No.9/2021 dated 20.05.2021, is hereby further extended to 31st December, 2021;

The due date of furnishing of Report of Audit under any provision of the Act for the Previous Year 2020-21, which is 30th September, 2021, as extended to 31st October, 2021 vide Circular No.9/2021 dated 20.05.2021, is hereby further extended to 15th January, 2022;

The due date of furnishing Report from an Accountant by persons entering into international transaction or specified domestic transaction under section 92E of the Act for the Previous Year 2020-21, which is 31st October, 2021, as extended to 30th November, 2021 vide Circular No.9/2021 dated 20.05.2021, is hereby further extended to 31st January, 2022;

The due date of furnishing of Return of Income for the Assessment Year 2021-22, which is 31st October, 2021 under sub-section (1) of section 139 of the Act, as extended to 30th November, 2021 vide Circular No.9/2021 dated 20.05.2021, is hereby further extended to 15th February, 2022;

The due date of furnishing of Return of Income for the Assessment Year 2021-22, which is 30th November, 2021 under sub-section (1) of section 139 of the Act, as extended to 31st December, 2021 vide Circular No.9/2021 dated 20.05.2021, is hereby further extended to 28th February, 2022;

The due date of furnishing of belated/revised Return of Income for the Assessment Year 2021-22, which is 31st December, 2021 under sub-section (4)/sub-section (5) of section 139 of the Act, as extended to 31st January, 2022, vide Circular No.9/2021 dated 20.05.2021, is hereby further extended to 31st March, 2022;

It is also clarified that the extension of the dates as referred to in clauses (9), (12) and (13) of Circular No.9/2021 dated 20.05.2021 and in clauses (1), (4) and (5) above shall not apply to Explanation 1 to section 234A of the Act, in cases where the amount of tax on the total income as reduced by the amount as specified in clauses (i) to (vi) of sub-section (1) of that section exceeds rupees one lakh. Further, in case of an individual resident in India referred to in sub-section (2) of section 207 of the Act, the tax paid by him under section 140A of the Act within the due date (without extension under Circular No.9/2021 dated 20.05.2021 and as above) provided in that Act, shall be deemed to be the advance tax.

CBDT Circular No.17/2021 in F.No.225/49/2021/ITA-II dated 09.09.2021 issued. The said Circular is available on http://www.incometaxindia.gov.in.

The e-Filing portal of the Income Tax Department (www.incometax.gov.in) was launched on 7th June, 2021. Taxpayers and professionals have reported glitches and difficulties in the portal since then. The Ministry of Finance has been regularly monitoring the resolution of issues with Infosys Ltd which is the Managed Services Provider for the project.

A number of technical issues are being progressively addressed and there has been a positive trend reflected in the statistics of the various filings on the portal. Over 8.83 crore unique taxpayers have logged in till 7th September, 2021 with a daily average of over 15.55 lakh in September, 2021. The Income Tax Return (ITR) filing has increased to 3.2 lakh daily in September, 2021 and 1.19 crore ITRs for AY 2021-22 have been filed. Of these, over 76.2 lakh taxpayers have used the online utility of the portal to file the returns.

It is encouraging to note that over 94.88 lakh ITRs have also been e-verified, which is necessary for processing by the Centralized Processing Center. Of this, 7.07 lakh ITRs have been processed.

Taxpayers have been able to view over 8.74 lakh Notices issued by the Department under the Faceless Assessment/Appeal/Penalty proceedings, to which, over 2.61 lakh responses have been filed. An average of 8,285 Notices for e-proceedings are being issued and 5,889 responses are being filed in September, 2021 on a daily basis.

Over 10.60 lakh Statutory Forms have been submitted including 7.86 lakh TDS statements, 1.03 lakh Form 10A for registration of Trusts/institutions, 0.87 lakh Form 10E for arrears of salary, 0.10 lakh Form 35 for Appeal.

Aadhaar- PAN linking has been done by 66.44 lakh taxpayers and over 14.59 lakh e-PAN have been allotted. These two facilities are being availed of by over 0.50 lakh taxpayers on a daily basis in September, 2021.

It is reiterated that the Department is continuously engaged with Infosys to ensure a smooth filing experience to taxpayers.

The Finance Act, 2021 has amended the provisions of the Income-tax Act, 1961 (“the Act”) to inter alia provide that the Income-tax Settlement Commission (“ITSC”) shall cease to operate with effect from 01.02.2021. Further, it has also been provided that no application for settlement can be filed on or after 01.02.2021, which was the date on which the Finance Bill, 2021 was laid before the Lok Sabha. In order to dispose off the pending settlement applications as on 31.01.2021, the Central Government has constituted Interim Board for Settlement (hereinafter referred to as the “Interim Board”), vide Notification no. 91 of 2021 dated 10.08.2021. The taxpayers, in the pending cases, have the option to withdraw their applications within the specified time and intimate the Assessing Officer about such withdrawal.

It has been represented that a number of taxpayers were in advanced stages of filing their application for settlement before the ITSC as on 01.02.2021. Further, some taxpayers have approached High Courts requesting that their applications for settlement may be accepted. In some cases, the Hon’ble High Courts have given interim relief and directed acceptance of applications of settlement even after 01.02.2021. This has resulted in uncertainty and protracted litigation.

In order to provide relief to the taxpayers who were eligible to file application as on 31.01.2021, but could not file the same due to cessation of ITSC vide Finance Act, 2021, it has been decided that applications for settlement can be filed by the taxpayers by 30th September, 2021 before the Interim Board if the following conditions are satisfied:-

The assessee was eligible to file application for settlement on 31.01.2021 for the assessment years for which the application is sought to be filed (relevant assessment years); and

all the relevant assessment proceedings of the assessee are pending as on the date of filing the application for settlement.

Such applications, subject to their validity, shall be deemed to be “pending applications” under clause (eb) of section 245A of the Act and shall be disposed of by the Interim Board as per the provisions of the Act.

It is clarified that taxpayers who have filed such applications shall not have the option to withdraw such applications as per the provisions of section 245M of the Act. Further, the taxpayers who have already filed application for settlement on or after 01.02.2021 as per the direction of the various High Courts and who are otherwise eligible to file such application, as per para 3 above, on the date of filing of the said application shall not be required to file such application again.

Legislative amendments in this regard shall be proposed in due course.

For easing the process of authentication of electronic records in faceless assessment proceedings, the Government has amended Income-tax Rules, 1962 (‘the Rules’) vide notification no G.S.R. 616(E) dated 6th September, 2021. The amended Rules provides that electronic records submitted through registered account of the taxpayers in the Income-tax Department’s portal shall be deemed to have been authenticated by the taxpayer by electronic verification code (EVC). Therefore, where a person submits an electronic record by logging into his registered account in designated portal of the Income-tax Department, it shall be deemed that the electronic record has been authenticated by EVC for the purposes of section 144B(7)(i)(b) of the Income-tax Act, 1961 (‘the Act’).

However, under the existing provisions of section 144B(7)(i)(b) of the Act, this simplified process of authentication by EVC is not available to certain persons (such as companies, tax audit cases, etc.) and they are mandatorily required to authenticate the electronic records by digital signature. In order to provide the benefit of the simplified process of authentication by EVC to these persons, it has been decided to extend the simplified process of authentication by EVC to these persons also. Hence, the persons who are mandatorily required to authenticate electronic records by digital signature shall be deemed to have authenticated the electronic records when they submit the record through their registered account in the Income-tax Department’s portal. Legislative amendments in this regard shall be proposed in due course.