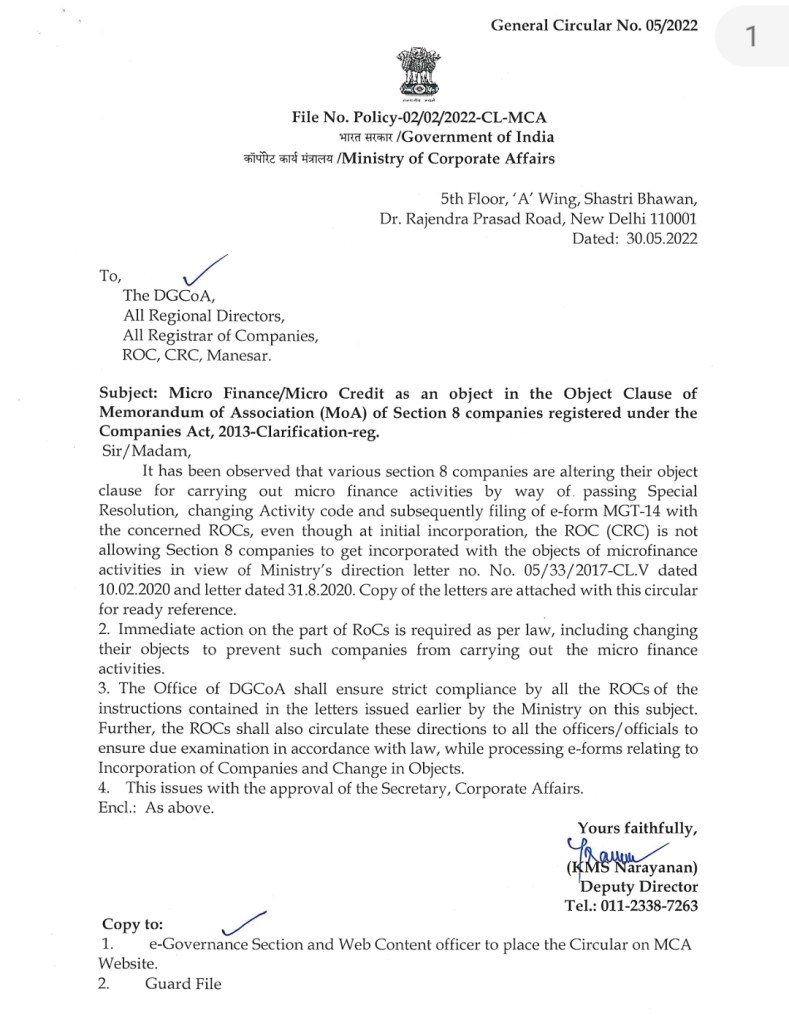

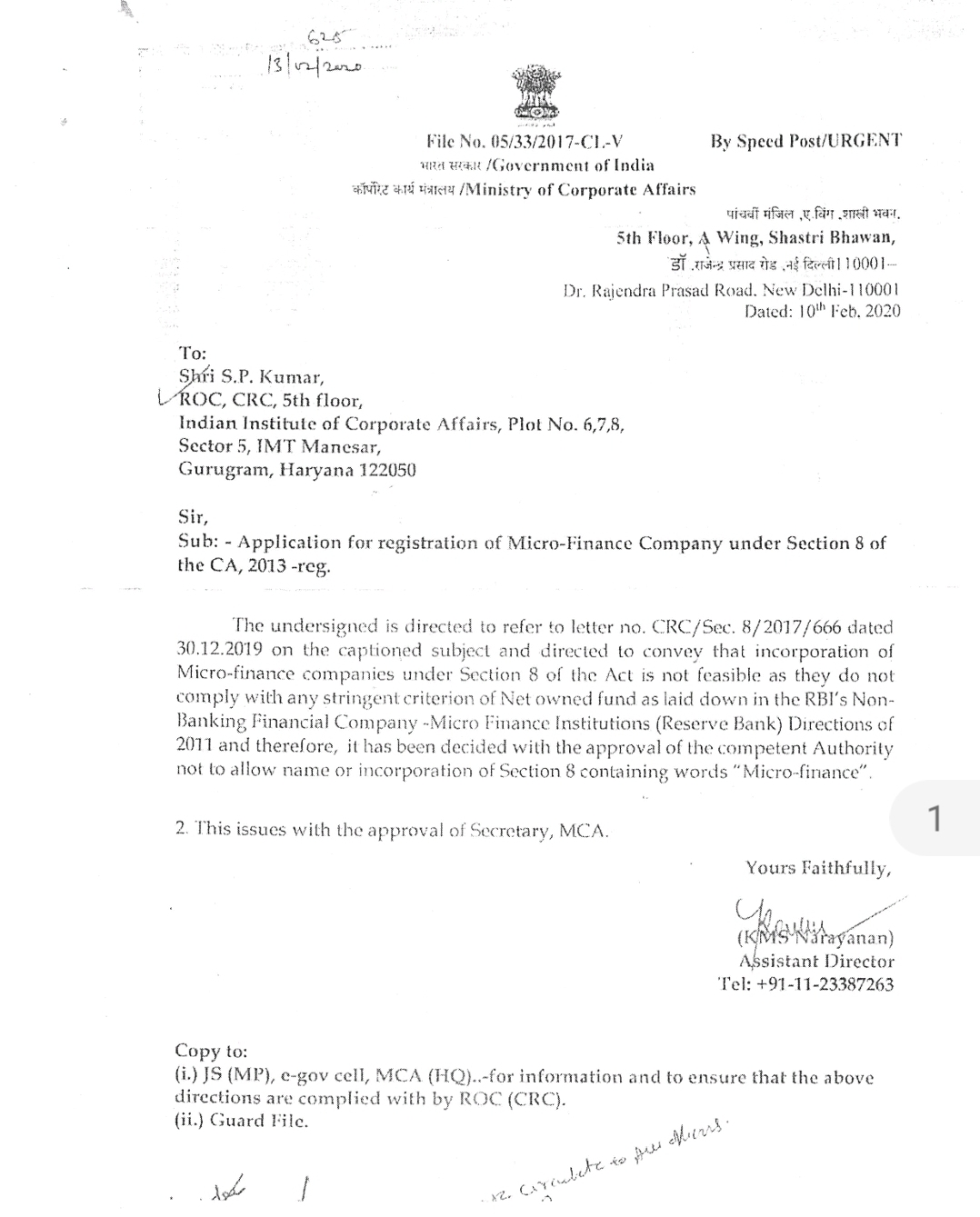

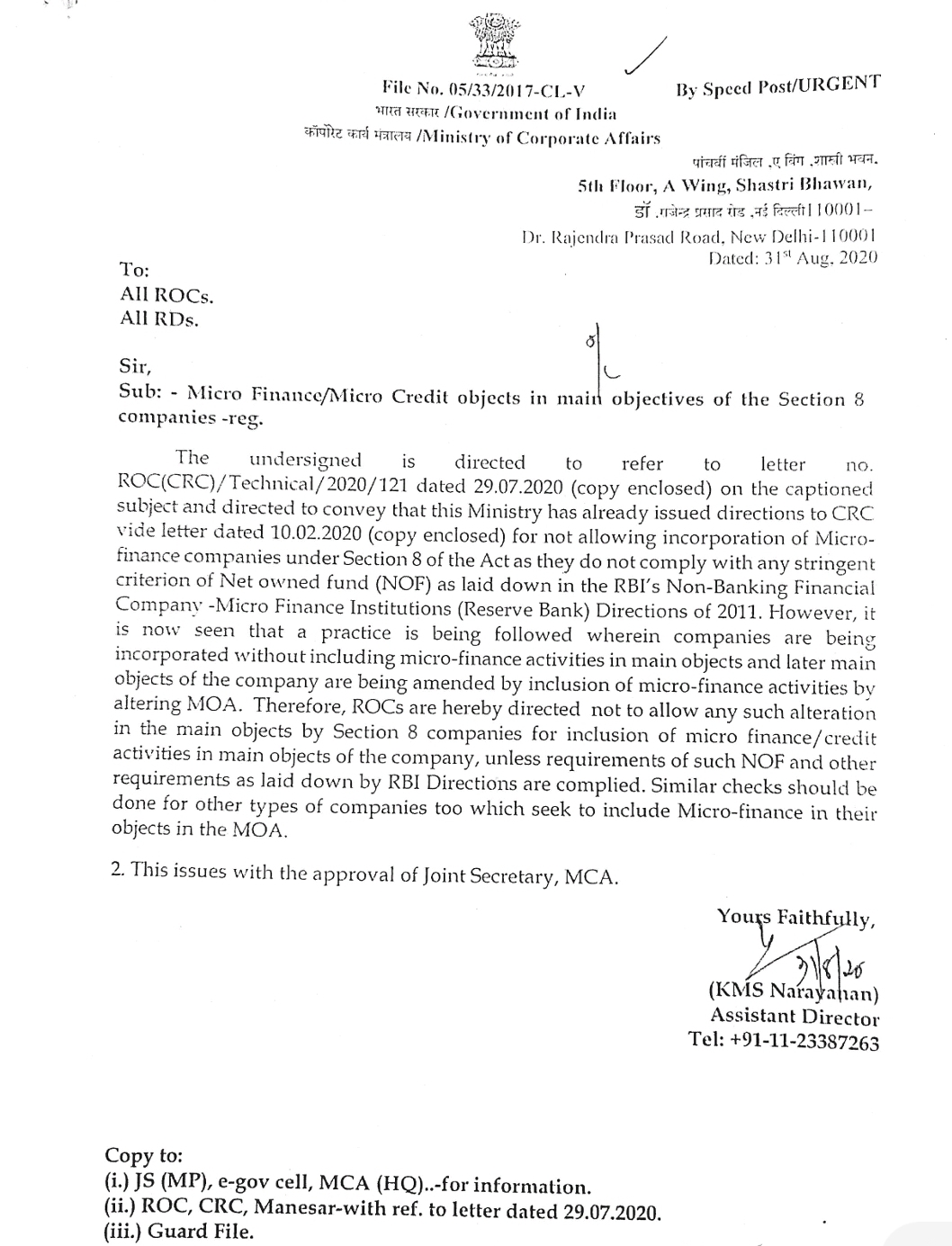

MCA issued General Circular on 30 May 2022 giving Clarification on Micro Finance/Micro Credit as an Object in the Object Clause of MOA of Section 8 companies registered under the CA 2013 :

Refer MCA Circular

Simplifying your business ideas, structures, functionalities, relations & operations

Company Law Articles, Video, PPT, Discussion, Expert Analysis

MCA issued General Circular on 30 May 2022 giving Clarification on Micro Finance/Micro Credit as an Object in the Object Clause of MOA of Section 8 companies registered under the CA 2013 :

Refer MCA Circular

Order passed by Adjudicating Authority without application of resolution professional’s for initiation of proceedings u/s 43 of IBC is unsustainable

Case Reference :

Sahara India Vs Nandkishor Vishnupant Despande (Delhi- NCLAT) dated 09 May 2022

Conclusion of the case:

When a statutory functionary makes an order based on certain grounds, its validity must be judged by the reasons so mentioned and cannot be supplemented by fresh reasons in the shape of affidavit or otherwise. Otherwise, an order bad in the beginning may, by the time it comes to court on account of a challenge, get validated by additional grounds later brought out…”

It reflects that the Resolution Professional, a statutory functionary, has not filed an application for initiation of proceedings under Section 43 of the Code in respect of preferential transactions and the Adjudicating Authority has passed the order, then it is supplementing it by fresh reason in through affidavit or otherwise. This is also not acceptable in the case of the Code.

Facts in brief:

The Appellant has remitted the principal amount of Rs. 39,95,00,000/- in various tranches commencing from April, 2018 to February, 2019 in accordance with the ‘Memorandum of Understanding’ (MOU) dated 07th March, 2017 with the Corporate Debtor (CD)/Respondent (in CIRP) for supply of future goods in the form of gold coins/Gold ornaments. The golds were supposed to be supplied by the CD any time after January, 2019. As per MoU vide para 1 reflects clearly that all such advance payments will not attract any interest. It is also stated at para 3 of the MOU that both the parties have agreed to fix the price of Gold coin/Gold ornaments at the prevailing market rate of the day when Gold coin/Gold Ornaments demanded is physically delivered to the Buyer as per the location(s) specified by the Buyer. The Seller also agrees to give 2% discount on the prevailing market price of Gold and will not charge making charges and delivery charges on the future demand by the Buyer (after January, 2019) and at the time of delivery of quantity. The Buyer has a right to assign its obligations and rights as per this MOU to its nominee(s) without taking prior consent of the Seller and the Seller shall not cause any hindrance are raise any objection in the same. The Seller gives at least 30 days’ notice showing its unwillingness to continue the understanding as reached between the parties and the buyer is ready to give a mutually agreed compensation as well as refund the excess amount, if any. The Ld. Counsel for the Appellant has submitted that they have informed the CD vide its letter dated 04th February, 2019 to supply of 10 kg Gold coins (100 points of 100 gram each) as obligation in accordance with the MOU. Even after long wait CD didn’t supplied, accordingly, the Appellant vide its letter dated 05th March, 2019 asked the CD to refund the amount as there is too much delay. The CD informed the Appellant vide its letter dated 11th March, 2019 to convert the advance amount of the Appellant into unsecured loan with 10% p.a. rate of interest on outstanding amount till full and final payment of the same are made to them. However, the Appellant accepted the offer after communicating the notice of default to the CD in between there are other correspondence also. ‘Corporate Insolvency Resolution Process’ was initiated against CD on 13th November 2019. Accordingly, the appellant submitted its claim in Form C. Resolution Professional considered the claims of the appellant, not in the category of ‘Financial Debt’ and as a result the appellant challenged the decision.

As per Companies (Accounts) Third Amendment Rules, 2022 a sub rule & provisio inserted in rule 12 as under:

Sub-rule (1B)

(i) for the figures, letters and word “31st May, 2022”, the figures, letters and word “30th June, 2022”, shall be substituted;

Proviso

(ii) “Provided further that for the financial year 2021-2022, Form CSR-2 shall be filed separately on or before 31st March, 2023 after filing Form AOC-4 or AOC-4 XBRL or AOC-4 NBFC (Ind AS), as the case may be”.

Refer notification:

Case Reference

Mahima Datla Vs Dr. Renuka Datla (Supreme Court of India) dated 06/04/2022

The *Duomatic Principle* can be briefly stated as ‘anything the members of a company can do by formal resolution in a general meeting, they can also do informally, if all of them assent to it.’

It is noted that application of Duomatic Principle is only applicable in those cases wherein bona fide transactions are involved. Fraud is a clear exception to application of these principles, be it Duomatic Principle or Doctrine of Indoor Management.

Ministry of Finance and Ministry of Corporate Affairs today held a Curtain Raiser press conference of their ‘Iconic Week’ celebrations as part of the ‘Azadi Ka Amrit Mahotsav’ (AKAM) during the week of 6th to 11th June, 2022.

Prime Minister Shri Narendra Modi had inaugurated the “Azadi Ka Amrit Mahotsav” (AKAM) on 12th March 2021, marking a 75-week countdown to the 75th Anniversary of India’s Independence on 15th August, 2022. The AKAM celebrations will continue for a year, thereafter, till 15th August, 2023.

As part of celebration of 75th anniversary of India’s 75th year of Independence, a ‘Thank You’ (Shukriya) song was released which celebrates the unsung heroes of the battle against COVID-19 Pandemic and those who kept the financial system running during the most challenging times.

An e-booklet was also presented to provide a snapshot of the events unfolding during the week in which the two Ministries – Corporate Affairs and Finance, will not only showcase their achievements, new initiatives, but also traverse through an interesting journey of their growth and evolution over the years. CLICK HERE to acesss the schedule of events.

Prime Minister Shri Narendra Modi will grace the inaugural function on the 6th of June 2022 in Vigyan Bhavan, New Delhi. The 6th June ceremony would be celebrated live simultaneously in 75 cities across India keeping up with the spirit of 75years of India’s Independence.

During the Iconic week of Azadi ka Amrit Mahotsav, Ministry of Corporate Affairs and each Department of Ministry of Finance will showcase their rich history and legacy as well as readiness to face the challenges ahead. For example, a documentary will be released on the Development of Securities Market in India on the third day, i.e. 8th June 2022; and on the last day, 11th June 2022, the National Customs and GST Museum, ‘Dharohar’, which showcases an array of seized goods, antiques, and customs heritage will be dedicated to the nation.

Some other notable events during the Iconic Week celebrations of the Ministry of Finance & Ministry of Corporate Affairs include the International Conference on data analytics in public procurement that will deliberate on the best international practices in the field of public procurement and way forward to harness modern tech to bring more value for money in public procurement. Some major initiatives in public expenditure management and taxation, both direct and indirect will also be showcased.

The kick off celebrations of Iconic Week of Ministry of Finance & Ministry of Corporate Affairs was presided over by Finance Secretary & Secretary Expenditure, Dr T.V. Somanathan. Among attendees were Shri Tuhin Kanta Pandey, Secretary, DIPAM; Shri Ajay Seth, Secretary, Economic Affairs; Shri Rajesh Verma, Secretary, Ministry of Corporate Affairs; Shri Ali Raza Rizvi, Secretary, DPE; Shri Sanjay Malhotra, Secretary, DFS; Shri Vivek Johri, Chairperson, CBIC and Smt. Sangeeta Singh, Chairperson (addl. Charge), CBDT, besides other senior officers of the Ministry of Finance & Corporate Affairs.

E-booklet for Ministry of Finance and Ministry of Corporate Affairs for Iconic Week celebrations of Azadi Ka Amrit Mahotsav:

Watch Press conference on PIB_India:

Refer Press release dated 30 May 2022

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1829415&RegID=3&LID=1

Delhi ROC Penalty order for non appointment of whole time Company Secretary in the matter of Pitchers Internet Private Limited dated 25 May 2022

Total Penalty imposed :

On Company: Rs.5 Lakhs

On officer in defaults: 13.23 Lakhs

APPELLANT: SEBI

RESPONDENTS: R.T. AGRO PRIVATE LIMITED & ORS.

| Legal provisions: 188. Related party transactions (1) Except with the consent of the Board of Directors given by a resolution at a meeting of the Board and subject to such conditions as may be prescribed, no company shall enter into any contract or arrangement with a related party with respect to— (a) sale, purchase or supply of any goods or materials; (b) selling or otherwise disposing of, or buying, property of any kind; (c) leasing of property of any kind; ——————————————————— [Provided that no contract or arrangement, in the case of a company having a paid-up share capital of not less than such amount, or transactions exceeding such sums, as may be prescribed, shall be entered into except with the prior approval of the company by a Special resolution ( Resolution substituted by Companies (Amendment) Act, 2015 and is effective from 29th May, 2015.): [Provided further that no member of the company shall vote on such [resolution], to approve any contract or arrangement which may be entered into by the company, if such member is a related party:]] |

Having heard learned counsel for the appellant-Securities and Exchange Board of India (‘SEBI’) and having perused the material placed on record, we find absolutely no reason to entertain this appeal.

The company R. T. Exports Limited proposed to enter into a transaction with one Neelkanth Realtors Private Limited for purchase of 40,000 sq. ft. of residential space. This proposal was treated as a related party transaction and was required to be approved by the shareholders of the Company. Accordingly, a special resolution was approved by R. T. Exports Limited on 15.07.2014. In terms of Section 188 of the Companies Act, 2013, the related parties abstained from voting on this special resolution. Thereafter, an Extra-Ordinary General Meeting was convened on 16.12.2016 for rescinding the resolution dated 15.07.2014 in which, the related parties also voted.

However, the appellant-SEBI took up the matter on a complaint and issued notice alleging violation of Regulation 23 of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015. The Adjudicating Officer, ultimately, proceeded to penalise the present respondents 1 with a cumulative sum of Rs. 35 lakhs for the alleged violation of the said Regulation 23.

The Securities Appellate Tribunal has not approved this order passed by the Adjudicating Officer and has allowed the appeal filed by the present respondents while, inter alia, holding that the bar of voting as per Section 188 of the Companies Act, 2013 on related parties operated only at the time of entering into a contract or arrangement, i.e., when the resolution dated 15.07.2014 was passed; and therein the said related parties indeed abstained from voting. The Appellate Tribunal found no fault in the said parties voting in the recalling/rescinding of the said resolution.

The view, as taken by the Appellate Tribunal, in the given set of facts and circumstances of the present case, appears to be a plausible view of the matter. In fact, nothing of ill-intent on the part of the respondents has been established in the present case. The hyper-technical stance of the appellant could have only been, and has rightly been, disapproved on the given set of facts and circumstances.

The appeal fails and is, therefore, dismissed.

All pending applications stand disposed of.

This Ministry has received representation seeking extension on timelines for filing the Annual Return (Form 11) by LLPs without paying additional fees. In view of transition from version-2 of MCA-21 to version-3 and to promote compliance on part of LLPs, it has been decided to allow LLPs to file e-Form 12 (Annual Return of Limited Liability Partnership) for the Financial Year 2021-2022 without paying additional fees upto 30th June,2022.

Refer MCA Circular

Kolkata ROC adjudication order for violation of Section 134 of the Companies Act, 2013 in the matter of M/s Kejriwal Castings Limited

Facts

Suo motu application filed by Co. & MD for adjudication of offence for contravention of Section 134 of CA 2013 for Board Report not prepared on due time

Penalty imposed

On Company : Rs. 6 Lakhs

On MD : Rs. 1 Lakh

Refer Rulings:

Law(s) Governing the eForm DPT-3

eForm DPT-3 is required to be filed pursuant to rule 16 of the of the Companies (Acceptance of Deposits) Rules, 2014 which are reproduced for your reference.

Rule 16: Return of deposits to be filed with the Registrar:

Every company other than Government company to which these rules apply, shall on or before the 30th day of June, of every year, file with the Registrar, a return in Form DPT-3 along with the fee as provided in Companies (Registration Offices and Fees) Rules, 2014 and furnish the information contained therein as on the 31st day of March of that year duly audited by the auditor of the company.

Form DPT-3 shall be used for filing return of deposit or particulars of transaction not considered as deposit or both by every company other than Government company.

Purpose of the Form: