The International Financial Services Centres Authority (IFSCA), in furtherance of its mandate to develop and regulate financial products, financial services and financial institutions in the International Financial Services Centres (IFSC) and to encourage promotion of financial technologies (‘FinTech’) across the spectrum of banking, insurance, securities, and fund management in IFSC has issued a detailed “Framework for FinTech Entity in the IFSCs”.

The “Framework for FinTech Entity in the IFSCs” is aimed at givingboost to the establishment of a world class FinTech Hub at GIFT IFSC comparable with other International Financial Centers (IFCs). The framework proposes to cover (i) financial technology (FinTech) solutions resulting in new business models, applications, process or productsin areas/activities linked to financial services regulated by IFSCA and (ii) advanced/innovative technological solutions which aid and assist activities in relation to financial products, financial services and financial institutions (TechFin).

The framework provides for a dedicated Regulatory Sandbox for FinTech products or solutions namely IFSCA FinTech Regulatory Sandbox and empowers IFSCA to grant Limited Use Authorization within FinTech Regulatory Sandbox to the eligible financial technology entities in IFSC. This would enable them to apply and avail Grants under the IFSCA FinTech Incentive Scheme 2022.

Further, it also enables some class/categories of technology companies having (i) a deployable advanced/innovative technology solution which aids and assists activities in relation to financial products, financial services, financial institutions and, (ii) credible track record including financial performance, to obtain Direct Entry (Authorization by IFSCA) by IFSCAwithout entering into the Regulatory Sandbox.

The framework also incorporates the Inter Operable Regulatory Sandbox (IoRS) mechanism. IoRS is a proposed mechanism to facilitate testing of innovative hybrid financial products / services falling within the regulatory ambit of more than one financial sector regulators. IFSCA will facilitate Indian FinTech’s seeking access to foreign markets and foreign FinTech’s seeking entry into India.

The framework proposes a Regulatory Referral mechanism which shall be governed as per the provisions of the Memorandum of Understanding (MoU) or collaboration or special arrangement between IFSCA and corresponding overseas Regulator(s)

IFSCA endeavors to support FinTech firms for proof of concept (PoC), minimum viable product (MVP), prototype development, product trials, commercialization, and global market access etc.

The GIFT-IFSC offers the unique advantage of being a separate financial jurisdiction within India which is treated like an offshore jurisdiction from FEMA angle with no restriction on currency convertibility. The framework issued by IFSCA, a unified regulator for Banking, Capital Markets, Insurance and Funds Management in IFSC, would enable FinTech firms having innovative ideas or solutions across the banking, capital or insurance sector to have seamless interaction with a single regulator.

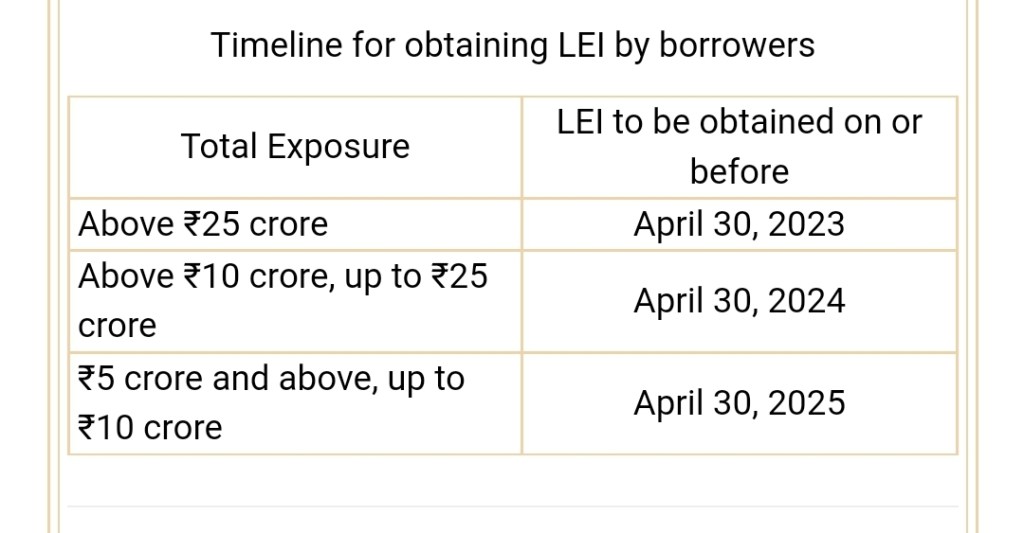

It has been decided that the guidelines on LEI stand extended to Primary (Urban) Co-operative Banks (UCBs) and Non-Banking Financial Companies (NBFCs).

It is further advised that non-individual borrowers enjoying aggregate exposure of ₹5 crore and above from banks and financial institutions (FIs) shall be required to obtain LEI codes as per the timeline given below:

“Exposure” for this purpose shall include all fund based and non-fund based (credit as well as investment) exposure of banks/FIs to the borrower. Aggregate sanctioned limit or or outstanding balance, whichever is higher, shall be reckoned for the purpose. Lenders may ascertain the position of aggregate exposure based on information available either with them, or CRILC database or declaration obtained from the borrower.

Borrowers who fail to obtain LEI codes from an authorized Local Operating Unit (LOU) shall not be sanctioned any new exposure nor shall they be granted renewal/enhancement of any existing exposure. However, Departments/Agencies of Central and State Governments (not Public Sector Undertakings registered under Companies Act or established as Corporation under the relevant statute) shall be exempted from this provision.

These directions are issued under sections 21, 35A and 56 of the Banking Regulation Act, 1949, sections 45JA and 45L of the Reserve Bank of India Act, 1934, section 30A of the National Housing Bank Act, 1987 and section 6 of the Factoring Regulation Act, 2011.

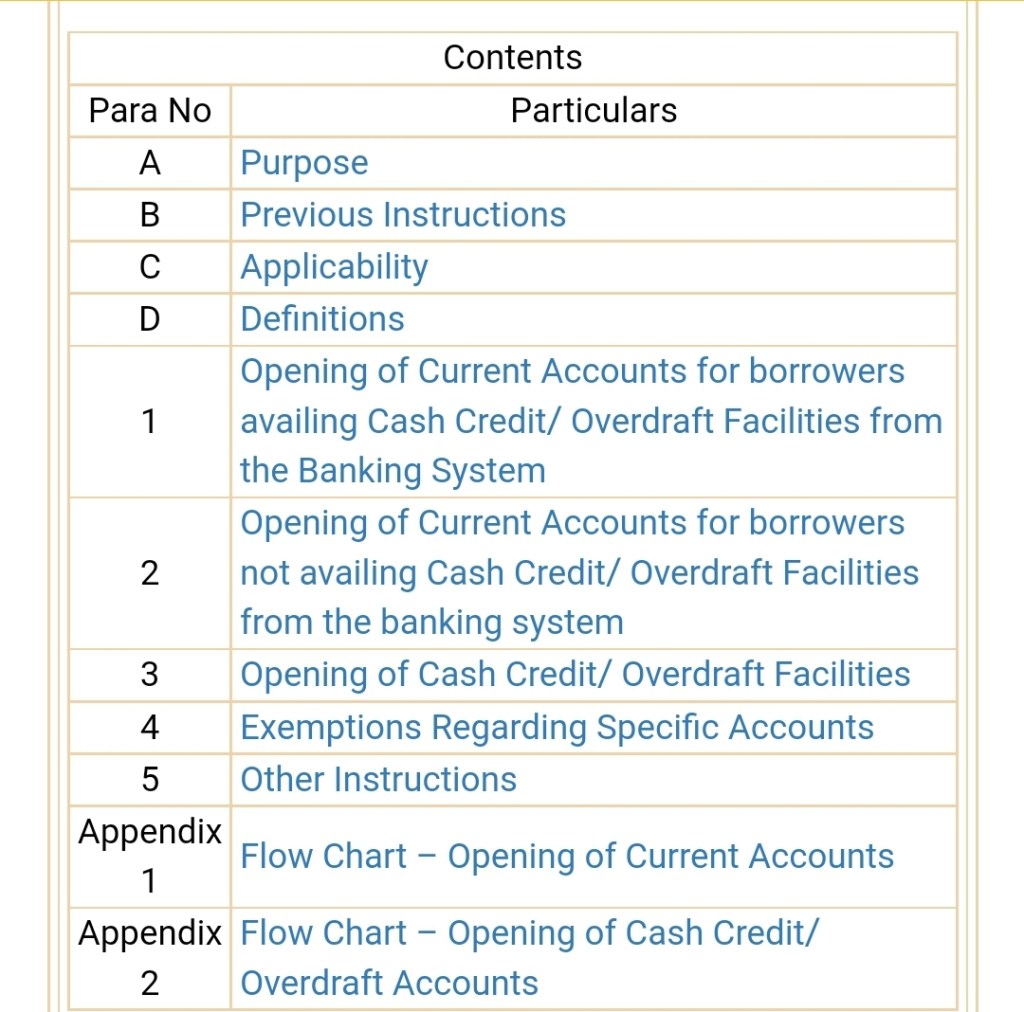

This Circular consolidates earlier instructions issued by the Reserve Bank of India, on opening and operation of current accounts and CC/OD accounts with a view to enforce credit discipline amongst the borrowers as well as to facilitate better monitoring by the lenders.

B. Previous Instructions

This circular consolidates instructions contained in the following circulars issued on the above subject:

The provisions of these instructions shall apply to current accounts and CC/OD accounts opened or maintained with the following Regulated Entities (REs):

All Scheduled Commercial Banks

All Payments Banks

D. Definitions

“Exposure” for the purpose of these instructions shall mean sum of sanctioned fund based and non-fund-based credit facilities availed by the borrower2. All such credit facilities carried in their Indian books shall be included for the purpose of exposure calculation.

“Banking System” for the purpose of these instructions, shall include Scheduled Commercial Banks and Payments Banks only.

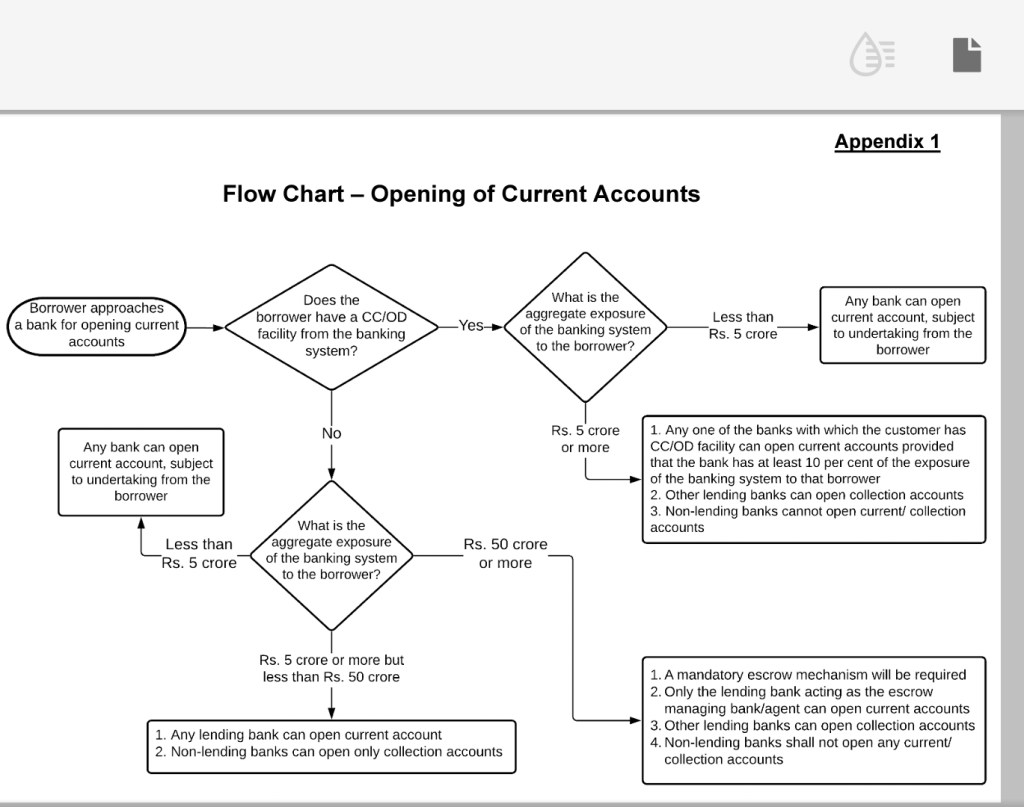

1. Opening of Current Accounts for borrowers availing Cash Credit/ Overdraft Facilities from the Banking System

1.1 For borrowers, where the aggregate exposure3 of the banking system is less than ₹5 crore, banks can open current accounts without any restrictions placed vide this circular subject to obtaining an undertaking from such customers that they (the borrowers) shall inform the bank(s), if and when the credit facilities availed by them from the banking system becomes ₹5 crore or more.

1.2 Where the aggregate exposure of the banking system is ₹5 crore or more:

1.2.1 Borrowers can open current accounts with any one of the banks with which it has CC/OD facility, provided that the bank has at least 10 per cent of the aggregate exposure of the banking system to that borrower. In case none of the lenders has at least 10 per cent of the aggregate exposure, the bank having the highest exposure among CC/OD providing banks may open current accounts.

1.2.2 Other lending banks may open only collection accounts subject to the condition that funds deposited in such collection accounts will be remitted within two working days of receiving such funds, to the CC/OD account maintained with the above-mentioned bank (para 1.2.1) maintaining current accounts for the borrower. The balances in such collection accounts shall not be used for repayment of any credit facilities provided by the bank, or as collateral/ margin for availing any fund or non-fund based credit facilities. However, banks maintaining collection accounts are permitted to debit fees/ charges from such accounts before transferring funds to CC/OD account.

1.2.3 Non-lending banks are not permitted to open current/ collection accounts.

2. Opening of Current Accounts for borrowers not availing Cash Credit/ Overdraft Facilities from the banking system

2.1 In case of borrowers where aggregate exposure of the banking system is ₹50 crore or more:

2.1.1 Banks shall be required to put in place an escrow mechanism. Borrowers shall be free to choose any lending bank as their escrow managing bank. All lending banks should be part of the escrow agreement. The terms and conditions of the agreement may be decided mutually by lending banks and the borrower.

2.1.2 Current accounts of such borrowers can only be opened/ maintained by the escrow managing bank.

2.1.3 Other lending banks can open ‘collection accounts’ subject to the condition that funds will be remitted from these accounts to the said escrow account at the frequency agreed between the bank and the borrower. Further, balances in such collection accounts shall not be used for repayment of any credit facilities provided by the bank, or as collateral/ margin for availing any fund or non-fund based credit facilities. While there is no prohibition on amount or number of credits in ‘collection accounts’, debits in these accounts shall be limited to the purpose of remitting the proceeds to the said escrow account. However, banks maintaining collection accounts are permitted to debit fees/ charges from such accounts before transferring funds to the escrow account.

2.1.4 Non-lending banks shall not open any current account for such borrowers.

2.2 In case of borrowers where aggregate exposure of the banking system is ₹5 crore or more but less than ₹50 crore, there is no restriction on opening of current accounts by the lending banks. However, non-lending banks may open only collection accounts as detailed at para 2.1.3 above.

2.3 In case of borrowers where aggregate exposure of the banking system is less than ₹5 crore, banks may open current accounts subject to obtaining an undertaking from them that they (the customers) shall inform the bank(s), if and when the credit facilities availed by them from the banking system becomes ₹5 crore or more. The current account of such customers, as and when the aggregate exposure of the banking system becomes ₹5 crore or more, and ₹50 crore or more, will be governed by the provisions of para 2.2 and para 2.1 respectively.

2.4 Banks are free to open current accounts of prospective customers who have not availed any credit facilities from the banking system, subject to necessary due diligence as per their Board approved policies.

2.5 Banks are free to open current accounts, without

any of the restrictions placed in this Circular, for borrowers having credit facilities only from NBFCs/ FIs/ co-operative banks/ non-bank institutions, etc. However, if such borrowers avail aggregate credit facilities of ₹5 crore or above from the banks covered under these guidelines, the provisions of the Circular shall be applicable.

3. Opening of Cash Credit/ Overdraft Facilities

3.1 When a borrower approaches a bank for availing CC/OD facility, the bank can provide such facilities without any restrictions placed vide this circular if the aggregate exposure of the banking system to that borrower is less than ₹5 crore. However, the bank must obtain an undertaking from such borrowers that they (the borrowers) shall inform the bank(s), if and when the credit facilities availed by them from the banking system becomes ₹5 crore or more.

3.2 For borrowers, where the aggregate exposure of the banking system is ₹5 crore or more:

3.2.1 Banks having a share of 10 per cent or more in the aggregate exposure of the banking system to such borrower can provide CC/OD facility without any restrictions placed vide this circular.

3.2.2 In case none of the banks has at least 10 per cent exposure, bank having the highest exposure among CC/OD providing banks can provide such facility without any restrictions.

3.2.3 Where a bank’s exposure to a borrower is less than 10 per cent of the aggregate exposure of the banking system to that borrower, while credits are freely permitted, debits to the CC/OD account can only be for credit to the CC/OD account of that borrower with a bank that has 10 per cent or more of aggregate exposure of the banking system to that borrower. Funds will be remitted from these accounts to the said transferee CC/OD account at the frequency agreed between the bank and the borrower. Further, the credit balances in such collection accounts shall not be used for repayment of any credit facilities provided by the bank, or as collateral/ margin for availing any fund or non-fund based credit facilities. However, banks are permitted to debit interest/ charges pertaining to the said CC/OD account and other fees/ charges before transferring the funds to the CC/OD account of the borrower with bank(s) having 10 per cent or more of the aggregate exposure. It may be noted that banks with exposure to the borrower of less than 10 per cent of the aggregate exposure of the banking system can offer working capital demand loan (WCDL)/ working capital term loan (WCTL) facility to the borrower.

3.2.4 In case there is more than one bank having 10 per cent or more of the aggregate exposure, the bank to which the funds are to be remitted may be decided mutually between the borrower and the banks.

4. Exemptions Regarding Specific Accounts

4.1 Banks are permitted to open and operate the following accounts without any of the restrictions placed in terms of paras 1, 2 and 3 of this Circular:

(a) Specific accounts which are stipulated under various statutes and specific instructions of other regulators/ regulatory departments/ Central and State Governments. An indicative list of such accounts is given below:

Accounts for real estate projects mandated under Section 4 (2) l (D) of the Real Estate (Regulation and Development) Act, 2016 for the purpose of maintaining 70 per cent of advance payments collected from the home buyers

Nodal or escrow accounts of payment aggregators/ prepaid payment instrument issuers for specific activities as permitted by Department of Payments and Settlement Systems (DPSS), Reserve Bank of India under Payment and Settlement Systems Act, 2007

Accounts for the purpose of IPO/ NFO/ FPO/ share buyback/ dividend payment/ issuance of commercial papers/ allotment of debentures/ gratuity etc. which are mandated by respective statutes or by regulators and are meant for specific/ limited transactions only

(b) Accounts opened as per the provisions of Foreign Exchange Management Act, 1999 (FEMA) and notifications issued thereunder including any other current account if it is mandated for ensuring compliance under the FEMA framework

(c) Accounts for payment of taxes, duties, statutory dues, etc. opened with banks authorized to collect the same, for borrowers of such banks which are not authorized to collect such taxes, duties, statutory dues, etc.

(d) Accounts for settlement of dues related to debit card/ ATM card/ credit card issuers/ acquirers

(e) Accounts of White Label ATM Operators and their agents for sourcing of currency

(f) Accounts of Cash-in-Transit (CIT) Companies/ Cash Replenishment Agencies (CRAs) for providing cash management services

(g) Accounts opened by a bank funding a specific project for receiving/monitoring cash flows of that specific project, provided the borrower has not availed any CC/OD facility for that project

(h) Inter-bank accounts

(i) Accounts of All India Financial Institutions (AIFIs), viz., EXIM Bank, NABARD, NHB, and SIDBI

(j) Accounts attached by orders of Central or State governments/ regulatory body/ Courts/ investigating agencies etc. wherein the customer cannot undertake any discretionary debits

4.2 Banks maintaining accounts listed in para 4.1 shall ensure that these accounts are used for permitted/ specified transactions only. Further, banks shall flag these accounts in the CBS for easy monitoring. Lenders to such borrowers may also enter into agreements/ arrangements with the borrowers for monitoring of cash flows/ periodic transfer of funds (if permissible) in these accounts.

5. Other Instructions

5.1 In case of borrowers covered under guidelines on loan system for delivery of bank credit issued vide circular DBR.BP.BC.No.12/21.04.048/2018-19 dated December 5, 2018, bifurcation of working capital facility into loan component and cash credit component shall continue to be maintained at individual bank level in all cases, including consortium lending

5.2 All banks, whether lending banks or otherwise, shall monitor all accounts regularly, at least on a half-yearly basis, specifically with respect to the aggregate exposure of the banking system to the borrower, and the bank’s share in that exposure, to ensure compliance with these instructions. If there is a change in exposure of a particular bank or aggregate exposure of the banking system to the borrower which warrants implementation of new banking arrangements, such changes shall be implemented within a period of three months from the date of such monitoring.

5.3 Banks shall put in place a monitoring mechanism, both at head office and regional/ zonal office levels to monitor non-disruptive implementation of the circular and to ensure that customers are not put to undue inconvenience during the implementation process.

5.4 Banks should not route drawal from term loans through CC/ OD/ Current accounts of the borrower. Since term loans are meant for specific purposes, the funds should be remitted directly to the supplier of goods and services. In cases where term loans are meant for purposes other than for supply of goods and services and where the payment destination is identifiable, banks shall ensure that payment is made directly, without routing it through an account of the borrower. However, where the payment destination is unidentifiable, banks may route such term loans through an account of the borrower opened as per the provisions of the circular. Expenses incurred by the borrower for day-to-day operations may be routed through an account of the borrower.

Delhi Customs seize 5.85 kg cocaine, the biggest at any airport in India, on 6th April 2022 night

In past six months, Delhi Airport Customs seized 33.70 kg of Heroin and 12.60 kg Cocaine at IGI Airport

35 cases booked by Customs at IGI Airport, with street value of drug seized at Rs. 887.35 crore and 34 passengers arrested in 2021-22 alonePosted Date:- Apr 07, 2022

The Delhi Airport Customs seized 5.85 kg cocaine, the biggest at any airport in India, on 6th April 2022 night at the IGI International Airport. The seizure last night by the Delhi Customs signifies the fight carried out by the Indian Customs against the menace of drugs.

5.85 kg cocaine was seized by Delhi Customs at IGI Airport on 6th April 2022.

Continuous flow from source countries have made drug accessibility easy. IGI Airport, being the premier Capital airport of the country receives lakhs of passengers annually, some of whom are actively operating as drugs carriers. Customs at IGI Airport is waging a relentless fight against such carriers and their handlers.

In the past six months, Customs at the IGI Airport alone has booked no less than 16 cases under NDPS Act, the highest number at any airport in the Country. In the process, almost 33.70 kg of Heroin and 12.60 kg of Cocaine has been seized from International passengers, mostly nationals of African origin. For the entire 2021-22, 35 cases booked by Customs at IGI Airport, with a street value of drugs estimated at Rs. 887.35 crore. 34 passengers have also been arrested in the process.

Two distinct modus operandi have been observed in these seizures. Some of the passengers pack the drugs inside latex capsules, which are then swallowed by them in order to get past Customs officers easily at the Airport. Later, they eject these capsules after consuming laxatives, running a great risk to their own lives. This modus operandi is not only very difficult to detect, but also very difficult to retrieve. The suspected passengers need to be admitted to government hospitals, where the extraction is conducted under medical supervision. This process often takes 4 to 5 days, sometimes longer. Needless to add, these passengers are kept constantly under strict observation and guarded day-and-night by the Customs officers, at great risk to their own lives due to COVID-19 pandemic. The seizure of narcotics drugs at the airport is just the beginning of a tough, long legal battle that ensues later.

In the second method, the drug is concealed in specially made cavities in the hand-baggage or Checked-in baggage being carried by the passengers. Such cases are detected by the combined use of the Customs Canine Squad and High-resolution X-ray. Both these modus operandi have been detected at IGI Airport. The expanding market and the remunerative lucrativeness has ensured that there is no reduction in the relentless flow of drugs attempted to be smuggled into India though the airports.

More than Rs 30,160 crore loans sanctioned to over 1,33,995 accounts under Stand-Up India Scheme in 6 years

“As more and more beneficiaries from underserved segments of entrepreneurs are targeted for coverage, we would make significant strides towards building an Atmanirbhar Bharat”: Finance Minister

As we celebrate the sixth anniversary of Stand Up India Scheme, let us take a look at how this scheme has fulfilled the aspirations entrepreneurs, particularly women and Scheduled Castes (SCs), Scheduled Tribes (STs) and also sift through the achievements, salient features and enhancement to the scheme over the years.

Recognizing the challenges faced by Aspiring SC, ST and women entrepreneurs, Stand up India Scheme was launched on 5th April 2016 to promote entrepreneurship at grassroot level focusing on economic empowerment and job creation. In 2019-20, the Stand Up India scheme was extended for the entire period coinciding with the 15th Finance Commission period of 2020-25.

On the occasion, Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman said, “As we commemorate the sixth anniversary of the Stand-Up India Scheme, it is heartening to see that more than 1.33 lakh new job-creators and entrepreneurs have so far been facilitated under this Scheme.”

Smt. Sitharaman further said, “More than 1 lakh women promoters have benefitted from this Scheme during its six years of operation. The Government understands the potential these rising entrepreneurs have in driving economic growth through their roles as not just wealth-creators but also job-creators.”

“As more and more beneficiaries from the underserved segments of entrepreneurs are targeted for coverage, we would make significant strides towards building an Atmanirbhar Bharat,” the Finance Minister added.

As India is growing rapidly, hopes, aspirations and expectations of a large group of potential entrepreneurs, particularly women and Scheduled Castes (SCs), Scheduled Tribes (STs), are rising. They want to set up an enterprise of their own to allow themselves to thrive and grow. Such entrepreneurs are spread across country and are bubbling with ideas on what they can do for themselves and their families. The scheme envisages to facilitate the dreams of aspiring SC, ST and women entrepreneurs to reality by supporting their energy and enthusiasm and removing many hurdles from their path.

As we celebrate the sixth anniversary of Stand Up India Scheme, let us take a look at the features and achievement of this Scheme.

Theobjective of Stand-Up India is to promote entrepreneurship amongst women, Scheduled Castes (SC) & Scheduled Tribes (ST) categories, to help them in starting a greenfield enterprise in manufacturing, services or the trading sector and activities allied to agriculture.

The purpose of Stand-Up India is to:

promote entrepreneurship amongst women, SC & ST category;

provide loans for greenfield enterprises in manufacturing, services or the trading sector and activities allied to agriculture;

facilitate bank loans between Rs.10 lakh and Rs.1 crore to at least one Scheduled Caste/ Scheduled Tribe borrower and at least one woman borrower per bank branch of Scheduled Commercial Banks.

Why Stand-Up India?

The Stand-Up India scheme is based on recognition of the challenges faced by SC, ST and women entrepreneurs in setting up enterprises, obtaining loans and other support needed from time to time for succeeding in business. The scheme therefore endeavors to create an eco-system which facilitates and continues to provide a supportive environment for doing business. The scheme seeks to give access to loans from bank branches to borrowers to help them set up their own enterprise. The scheme, which covers all branches of Scheduled Commercial Banks, will be accessed in three potential ways:

SC/ST and/or women entrepreneurs, above 18 years of age;

Loans under the scheme are available for only green field projects. Green field signifies; in this context, the first time venture of the beneficiary in manufacturing, services or the trading sector and activities allied to agriculture;

In case of non-individual enterprises, 51% of the shareholding and controlling stake should be held by either SC/ST and/or Women Entrepreneur;

Borrowers should not be in default to any bank/financial institution;

The Scheme envisages ‘upto 15%’ margin money which can be provided in convergence with eligible Central/State schemes. While such schemes can be drawn upon for availing admissible subsidies or for meeting margin money requirements, in all cases, the borrower shall be required to bring in minimum of 10 % of the project cost as own contribution.

Handholding Support:

Apart from linking prospective borrowers to banks for loans, the online portal http://www.standupmitra.in developed by Small Industries Development Bank of India (SIDBI) for Stand Up India Scheme is also providing guidance to prospective entrepreneurs in their endeavour to set up business enterprises, starting from training to filling up loan applications as per bank requirements. Through a network of more than 8,000 Hand Holding Agencies, this portal facilitates step by step guidance for connecting prospective borrowers to various agencies with specific expertise viz. Skilling Centres, Mentorship support, Entrepreneurship Development Program Centres, District Industries Centre, together with addresses and contact number.

Changes to Stand Up India Scheme

Pursuant to an announcement by the Union Finance Minister in the Budget speech FY 2021-22, the following changes have been made in the Stand Up India Scheme:-

The extent of margin money to be brought by the borrower has been reduced from ‘upto 25%’ to ‘upto 15%’ of the project cost. However, the borrower will continue to contribute at least 10% of the project cost as own contribution;

Loans for enterprises in ‘Activities allied to agriculture’ e.g. pisciculture, beekeeping, poultry, livestock, rearing, grading, sorting, aggregation agro industries, dairy, fishery, agriclinic and agribusiness centers, food & agro-processing, etc. (excluding crop loans, land improvement such as canals, irrigation, wells) and services supporting these, shall be eligible for coverage under the Scheme.

To extend collateral free coverage, Government of India has set up the Credit Guarantee Fund for Stand Up India (CGFSI). Apart from providing credit facility, Stand Up India Scheme also envisages extending handholding support to the potential borrowers. It also provides for convergence with Central/State Government schemes. Applications under the scheme can also be made online at (www.standupmitra.in) portal.

The Government has taken several initiatives to support and protect the interest of women and other entrepreneurs through stimulus given under Aatma Nirbhar Bharat Packages to combat the impact of the COVID-19 pandemic in India. The packages comprise of schemes for various sectors of the economy and also schemes having impact across sectors. The specific initiatives taken to protect women entrepreneurs and MSMEs are as under:

Rs. 3 lakh crore Emergency Working Capital Facility for Businesses, including MSMEs

Rs. 20,000 crore Subordinate Debt for Stressed MSMEs

Rs. 50,000 crore equity infusion through MSME Fund of Funds

New Definition of MSME and other Measures for MSME

Rs. 10,000 crore scheme for formalisation of Micro Food Enterprises (MFE)

Relief of Rs. 1500 crore to MUDRA loanees

Emergency Credit Line Guarantee Scheme (ECLGS) for MSMEs, businesses, MUDRA borrowers and individuals

Rs. 5000 crore Credit facility for Street Vendors.

Under Pradhan Mantri Garib Kalyan Package, a total of 20.40 crores (approx) women account holders (Pradhan Mantri jan Dhan Yojana) were given an ex-gratia of Rs. 500 per month for three months.

For Self-Help groups (SHGs), limit of collateral free lending was increased from Rs.10 lakhs to Rs. 20 lakhs for women organized through 63 lakhs SHGs, who supported 6.85 crore households.

Under the ECLGS Scheme as on 28.02.2022, 81.18 lakhs women beneficiaries have been provided guarantees for loan. The State-wise details are at Annexure.

This information was given by the Union Minister of Women and Child Development, Smt. Smriti Zubin Irani, in a written reply in Lok Sabha today.

Ministry of Women and Child Development Press Release dated 01 April 2022

Cabinet approves setting up of National Land Monetization Corporation (NLMC)

NLMC to undertake monetization of surplus land and building assets of CPSEs and other Government agencies

The Union Cabinet on 9th March 2022 has approved setting up of National Land Monetization Corporation (NLMC) as a wholly owned Government of India company with an initial authorized share capital of Rs 5,000 crore and paid-up share capital of Rs 150 crore. This was stated by Union Minister of State for Finance Dr Bhagwat Kisanrao Karad in a written reply to a question in Rajya Sabha today.

The Minister stated that NLMC will undertake monetization of surplus land and building assets of Central Public Sector Enterprises (CPSEs) and other Government agencies. The proposal is in pursuance of the Budget Announcement for 2021-22, the Minister stated.

NLMC, the Minister listed out, has the following objectives:

To undertake professional and orderly monetization of land and other non- core assets referred to it.

To own, hold, manage and monetize land and building assets of CPSEs under closure and surplus land and buildings of 100% GoI owned CPSEs under strategic disinvestment.

To advise and support monetization of surplus land assets of (i)Demerged companies holding surplus land (ii) Other CPSEs

To advise and assist government departments, statutory bodies/ authorities, autonomous bodies, corporations, etc. on monetisation of surplus and under- utilized non-core assets.

To identify surplus land and building assets to create an inventory for monetization in consultation with CPSEs/other government agencies.

to build a capable organisation with skill and competencies to enable speedier and efficient monetisation which can generate maximum value from government assets.

To act as a repository of best practices in land monetization, assist and provide expert technical advice to DPE / DIPAM /Government of India in implementation of asset monetisation program.

The Minister further stated that NLMC would be administered by a Board of Directors. The proposed Board structure envisages a mix of senior government officials and eminent professionals in the field of real estate, banking, investment banking, construction, legal and related fields. The Board is expected to have necessary experience and expertise to steer the functioning of the NLMC in a professional manner. An eminent professional would be appointed as the Chairman of the Board, the Minister stated.

Incorporation of NLMC is underway which is being steered by Department of Public Enterprises, Ministry of Finance, the Minister stated.

Various steps have been taken by Reserve Bank of India (RBI) to expand the reach of UPI outside India. This was stated by Union Minister of State for Finance Dr Bhagwat Kisanrao Karad in a written reply to a question in Lok Sabha today. The steps are given below:-

NPCI International Payments Limited (NIPL), a wholly owned subsidiary of National Payments Corporation of India (NPCI) is devoted for internationalisation of UPI. NIPL has undertaken various initiatives across nations to enable cross-border acceptance of BHIM UPI QR at merchant establishment. These partnerships will facilitate Indian travellers to make payments using the BHIM UPI QR for all their retail purchases at international merchant establishments.

Currently, BHIM UPI QR has gained acceptance in Singapore (March, 2020), Bhutan (July, 2021) and recently with partners in UAE and Nepal (February, 2022). However, travel restrictions owing to the pandemic over the last two years have impacted overseas use of this facility.

In this regard, RBI has been facilitating engagements for the expansion of UPI in countries which have potential for collaboration. Various models of engagements being explored are as follows:

Central Bank to Central Bank cooperation through an agreement or MoU;

Central Bank facilitated discussion and agreement between the network and the Central Bank / Government Agency; and

Network to network arrangement.

Further, the performance of UPI123Pay launched in March 2022 is as follows:

The following major steps have been taken for promotion of Digital Payments by Ministry of Electronics & IT (MeitY):

The incentive scheme for promotion of RuPay Debit cards and low-value BHIM-UPI transactions (P2M) has been initiated by MeitY to give a further boost to digital transactions in the country. This scheme facilitates Banks in building robust digital payment ecosystem, promoting RuPay Debit card and BHIM-UPI digital transactions, across all sectors and segments of the population and further deepening of digital payments in the country.

Various other Incentive/cashback schemes were launched by MeitY for changing the customer/merchant behaviour for faster adoption of digital payments. Some of them were BHIM Cashback schemes for Individuals & Merchants, BHIM Aadhaar Merchant Incentive Scheme, BHIM-UPI Merchant On-boarding Scheme Merchant Discount Rate (MDR) Reimbursement scheme.

MeitY issued advisories to Central Ministries/Departments and States/UTs to improve payments acceptance infrastructure and thereby enable the citizens to pay by a variety of modes such as Internet banking, mobile banking, and mobile applications etc.

MeitY launched the scheme titled “Pradhan MantriGramin Digital SakshartaAbhiyan (PMGDISHA)” to usher in digital literacy in rural India.

MeitY advised all Banks and Payment Service Providers to undertake awareness campaigns for promotion of secure payment practices and generate information security awareness. Materials are disseminated through portals- “www.infosecawareness.in”, www.cyberswachhtakendra.gov.in .

Awareness campaigns were organized in the Capital Cities of North East to promote digital payments including BHIM app. MeitY also ran Newspaper campaigns, Digital Theatre Campaigns, FM Radio campaigns and hoarding campaigns to promote digital payments.

Various promotion and awareness campaigns, through traditional means of publicity as well as emergent means such as social media platforms, have been initiated to encourage citizens to use digital payments.

As part of the week-long ‘AzadiKa Digital Mahotsav’, MeitY celebrated, India’s Digital Payment Journey through a marquee ‘Digital Payment Utsav’. The day celebrated the journey and rise of digital payments in India and brought together leaders from the Government, Banking sector, Fintech companies, and Startups. Top Banks were awarded & recognized in various categories for achievements in FY 2019-20 and FY 2020-21 towards the promotion of Digital Payments.

MeitY has integrated Digital Payment Grievances along with Ministry of Consumer Affairs (MoCA) for utilizing it with National Consumer Helpline (NCH) platform of Department of Consumer Affairs (DoCA). All the major banks and financial service institutions have been on-boarded on NCH Platform. The platform is live and receiving Digital Payment related grievances.

In order to ensure safety and security of digital payments, various steps have been taken by the Government and Reserve Bank of India(RBI)

Promotion of digital payments ecosystem is an essential aspect of Digital India programme and is aimed at digitizing the financial sector and economy with consequent benefits of efficiency, transparency and quality. Over the years, digital payment transactions have grown multifold from 2071 crore in FY 2017-18 to 5,554 crore in FY 2020-21. During current financial year ie FY 2021-22, the total number of 8193 crore digital payment transactions have been reported till 20th March, 2022*. Bharat Interface for

Money-Unified Payments Interface (BHIM-UPI) has emerged as the preferred payment mode of the citizens and has achieved a record of 452.75 crore digital payment transactions with the value of Rs 8.27 lakh crore till 28th February 2022. The total number of digital payments undertaken during the last three years and current year is as under:

The Governor, Reserve Bank of India (RBI), Shri Shaktikanta Das inaugurated the Reserve Bank Innovation Hub (RBIH) today (March 24, 2022) in Bengaluru. The RBI has set up the RBIH as a Section 8 company under Companies Act, 2013, with an initial capital contribution of ₹100 crore to encourage and nurture financial innovation in a sustainable manner through an institutional set-up.

The Hub has an independent Board with Shri Senapathy (Kris) Gopalakrishnan as the Chairman and other eminent persons from industry and academia as members. RBIH aims to create an ecosystem that focuses on promoting access to financial services and products for the low-income population in the country. This is in line with the objective behind establishment of RBIH i.e., to bring world class innovation to financial sector in India, coupled with the underlying theme of financial inclusion.

The Hub would bring convergence among various stakeholders (BFSI Sector, Start-up ecosystem, Regulators & Academia) in the financial innovation space.

Details regarding the functions of RBIH are available at https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=50666.

The text of the inaugural address by the Governor, RBI is also available at https://rbi.org.in/Scripts/BS_SpeechesView.aspx?Id=1202.