The Government of India, in consultation withthe Reserve Bank of India, has decided to issue Sovereign Gold Bonds. The Sovereign Gold Bonds will be issuedin fourtranches fromOctober 2021 to March 2022 as per the calendar specified below:

Tranche :2021-22 Series VII

Date of Subscription: October 25 – 29, 2021

Date of Issuance: November 02, 2021

Issuance of calendar for Sovereign Gold Bond Scheme 2021-22

Sec 138 NI Act: Complaint comes to an end Once Accused & Complainant Enter into a Settlement Agreement: SC Gimpex Private Limited Vs Manoj Goel (Supreme Court of India)

Sec 138 NI Act- Complainant to prove the existence of a debt

V.P. Zacharia Vs State of Kerala (Kerala High Court)

Section 138 NI Act Directors responsible if they were in charge of & responsible for conduct of business of company: SC

Ashutosh Ashok Parasrampuriya Vs Gharrkul Industries Pvt. Ltd. (Supreme Court of India)

Sec 138 NI Act- Salutation Like Mr./M/s. while Drawing Cheque are Irrelevant N. Raveendran Vs Shajahan (Kerala High Court)

Preventive detention order unsustainable on stale or illusory grounds having no real nexus with past prejudicial activity

Naveen Kasera Alias Naveen Agrawal Vs. Union of India (Delhi High Court)

NI Act | Section 139 Presumption if signature on cheque is admitted

Triyambak S. Hegde Vs Sripad (Supreme Court of India)

Ministry of Power Press Release dated 11th Oct 2021

As an important step under the ongoing power sector reforms, Ministry of Power today mandated electricity distribution companies to undertake energy accounting on periodic basis. The regulation in this regard was issued by Bureau of Energy Efficiency (BEE) with the approval of Ministry of Power, under the provisions of Energy Conservation (EC) Act, 2001. The notification stipulates quarterly energy accounting by DISCOMs, through a certified Energy Manager, within 60 days. There will also be Annual energy audit by an independent Accredited Energy Auditor. Both these reports will be published in the public domain. Energy accounting reports will provide detailed information about electricity consumption by different categories of consumers & the transmission and distribution losses in various areas. It will identify areas of high loses and theft and enable corrective action. This measure will also enable fixation of responsibility on officers for losses and theft. The data will enable the DISCOMS to take appropriate measure for reducing their electricity losses. The DISCOMs will be able to plan for suitable infrastructure up-gradation as well as demand side management (DSM) efforts in an effective manner. This initiative will further contribute towards India’s climate actions in meeting our Paris Agreement Goals.

These regulations have been issued under the ambit of Energy Conservation Act, 2001, with an overall objective to reduce distribution sector in-efficiency and losses thereby moving towards economic viability of DISCOMs. BEE has certified a pool of National Accredited Energy Auditors and Energy Managers who possess expertise in preparing energy accounting and audit reports, duly providing recommendations for loss reduction and other technical measures. The aforesaid regulations were pre-published in April 2021 for seeking public comments and thereafter Ministry of Power held detailed discussions with various stakeholders before finally issuing these regulations.

In September 2020, through a separate notification, all the Electricity Distribution Companies were notified as Designated Consumers (DCs) under the EC Act. Owing to the potential benefits of energy auditing on the entire distribution system and retail supply business, it was imperative to develop a set of comprehensive guidelines and framework such that all Distribution utilities across India can adhere to and formulate actions.

Energy Accounting prescribes accounting of all energy inflows at various voltage levels in the distribution periphery of the network, including renewable energy generation and open access consumers, as well as energy consumption by the end consumers. Energy accounting on periodic basic and subsequent annual energy audit, would help to identify areas of high loss and pilferage, and thereafter focussed efforts to take corrective action. The Regulations issued today provides much awaited broad framework for Electricity Distribution Companies to carry out Annual Energy Audit and Quarterly Periodic Energy Accounting with necessary Pre-requisites and reporting requirements to be fulfilled.

Objectives to be achieved through periodic energy accounting are:

Development of a comprehensive energy accounting system to quantify and determine actual losses in the power distribution system, segregated across technical and commercial losses.

Identify areas of leakage, theft, wastage or inefficient use, thereby paving the way for tackling the present challenges of high Transmission and Distribution (T&D) losses.

Enable and ensure an independent 3rd party energy audit of the distribution system to arrive at a true and fair picture of T&D losses.

To enable the Distribution utilities to undertake targeted efficiency improvement activities to reduce T&D losses in priority areas / customer segments.

Providing a basis for prioritizing energy capital investments and help budget more accurately to achieve maximum results.

Identification of overloaded segments of the network for necessary capacity additions.

International Financial Services Centres Authority (IFSCA) and GIFT City launched I-Sprint’21, the global FinTech Hackathon Series of IFSCA on 7th October 2021 at 11.30 AM IST. The first Sprint of the series “Sprint01: BankTech” is focussed on FinTechs for the Banking sector.

The IFSCA is a unified authority for the development and regulation of financial products, financial services and financial institutions in the International Financial Services Centres (IFSCs) in India. IFSCA endeavours to encourage the promotion of financial technologies (‘FinTech’) initiatives across the spectrum of banking, insurance, securities and fund management in IFSC. In this context, a series of Hackathons cutting across these sectors have been planned under the banner of I-Sprint’21. This hackathon is first under the I-Sprint series focussing on the Banking Sector and is one of its kind being backed by a Regulator. It shall be conducted virtually and is open to eligible FinTechs from across the Globe.

Following the announcement by Hon’ble Finance Minister in Union Budget 2020-21 on supporting a “World Class FinTech Hub” at GIFT IFSC, IFSCA had introduced a framework for “Regulatory Sandbox” in October 2020 which allows the FinTech entities to have facilities and flexibilities to experiment with innovative FinTech solutions in a live environment with a limited set of real customers for a limited time frame. The finalists of this Hackathon shall be allowed direct entry into IFSCA Regulatory/Innovation Sandbox.

Sprint01: BankTech is hosted jointly by IFSCA and GIFT city in collaboration with NITI Aayog. The Partners to the Hackathon are ICICI Bank, HSBC Bank, iCreate, Zone Startups and Invest-India.

The aim of the Hackathon is:

(a) to connect IFSCA and GIFT IFSC with FinTech Ecosystem

(b) to solve Business Problems for the Banking Units at GIFT IFSC and

(c) to promote retail business for the Banking Units at GIFT IFSC.

Major rewards and recognition proposed under Sprint01: BankTech are:

FinTech finalists to be allowed direct entry into IFSCA Regulatory/Innovation Sandbox.

FinTechs will work directly with the Partner Banks on the problem statement who will provide the APIs, mentoring, guidance, etc.

Opportunity for the FinTechs to show-case during the Flagship FinTech Forum of IFSCA scheduled during Dec’2021

iCreate sponsored Price money of Rs 24 lakh

Business Support Solution Partner benefits of upto $25,000 per startup from Zone Startups India’s network.

The Cabinet Committee on Economic Affairs (CCEA) – empowered Air India Specific Alternative Mechanism (AISAM) comprising of Union Minister for Home Affairs and Cooperation Shri Amit Shah; Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman; Union Minister for Commerce and Industry Shri Piyush Goyal and Union Civil Aviation Minister Shri Jyotiraditya Scindia approved the highest price bid of M/s Talace Pvt Ltd, a wholly owned subsidiary of M/s Tata Sons Pvt. Ltd for sale of 100% equity shareholding of Government of India in Air India along with equity shareholding of Air India in AIXL and AISATS. The winning bid is for Rs 18,000 crore as Enterprise Value (EV) consideration for AI (100% shares of AI along with AI’s shareholding in AIXL and AISATS). The transaction does not include non-core assets including land and building, valued at Rs 14,718 crore, which are to be transferred to GoI’s Air India Asset Holding Limited (AIAHL).

The process for disinvestment of Air India and its subsidiaries commenced in June 2017 with the ‘in-principle’ approval of CCEA. The first round did not elicit any Expression of Interest. The process re-commenced on 27 January 2020 with issue of Preliminary Information Memorandum (PIM) and request for Expressions of Interest (EOI). The original construct as per the January 2020 PIM envisaged (i) pre-determined, fixed amount of debt to be retained in AI (with balance to be transferred to Air India Asset Holding Limited (AIAHL) and (ii) the sum of certain identified current and non-current liabilities (other than debt) to be retained in AI and AIXL would be equal to the sum of certain identified current and non-current assets of AI and AIXL (excess liabilities to be transferred to AIAHL).

The timelines had to be extended on account of the situation arising from the COVID-19 pandemic. In view of the excessive debt and other liabilities of Air India arising out of huge accumulated losses, the bidding construct was revised in October 2020 to Enterprise Value (EV) to allow prospective bidders an opportunity to resize the balance sheet and increase chances of receiving bids and competition. The EV construct allowed the bidders to bid on the total consideration for equity and debt instead of a pre-determined, fixed debt with minimum cash consideration of 15% for equity. As per both the original and revised construct, all non-core assets (land, buildings, etc.) are to be transferred to AIAHL and are therefore not a part of the transaction. It has been ensured that the interest of the employees and retired employees would be taken care of.

The transaction saw keen competition with seven EOIs being received in December, 2020. Five of the bidders, however, had to be disqualified as they could not meet the requirements set out in the PIM/EOI, even after allowing them an opportunity for clarification. The Request for Proposal (RFP) and draft Share Purchase Agreement (SPA) was issued on 30 March, 2021. Air India provided comprehensive information through the Virtual Data Room to the qualified bidders who were also provided access to inspect the assets and facilities being offered as a part of the transaction. A large number of queries from bidders were responded to. On request of bidders, the bid due date was extended to 15 September, 2021 so that they could complete their due diligence before submission of bid. The final SPA containing detailed terms and conditions and the respective responsibilities to meet the conditions precedent for closing the transaction including release of Government guarantees prior to closing was agreed upon prior to bid submission. Two sealed bids were received on the due date along with non-financial bid documents and bid security from the two qualified bidders.

In line with the approved procedure for strategic disinvestment, a reserve price was fixed after the receipt of sealed financial bids for the transaction, based on valuation using methodologies as per the established process. After the independent fixation of Reserve Price, the already received sealed financial bids were opened in the presence of the bidders, who were as follows:

M/s Talace Pvt Ltd, a wholly owned subsidiary of M/s Tata Sons Pvt Ltd for an EV of Rs 18,000 crore

Consortium led by Sh Ajay Singh for an EV of Rs 15,100 crore.

Both the bids were above the reserve price of Rs 12,906 crore.

The entire disinvestment process has been carried out in a transparent manner, with due regard to confidentiality of the bidders, through multi-layered decision making involving Inter-Ministerial Group (IMG), Core Group of Secretaries on Disinvestment (CGD) and the empowered Air India Specific Alternative Mechanism (AISAM) at the apex Ministerial level. Transaction Adviser, Legal Adviser, Asset Valuer, professionals in their respective fields, have supported the entire process.

The next step will be to issue the Letter of Intent (LoI) and then sign the Share Purchase Agreement following which, the conditions precedent would need to be satisfied by the successful bidder, the company and Government. It is expected that the transaction will be completed by December 2021.

Ministry of Finance Press Release dated 08 Oct 2021

International Financial Services Centres Authority (IFSCA) has been established as a unified regulator to develop and regulate financial products, financial services, and financial institutions in the International Financial Services Centres (IFSCs) in India.

India aspires to be a frontrunner in climate action, which is evident in its commitment towards its intended Nationally Determined Contributions under Paris Agreement. Raising financial resources for climate change adaptation and mitigation actions of this scale needs active participation of international investors. IFSCA envisions GIFT- IFSC as a global hub for sustainable finance thereby acting as a gateway for channelizing foreign capital into India.

IFSCA, in its endeavour to develop the required eco-system has constituted an Expert Committee to recommend approach towards development of Sustainable Finance Hub and provide road map for the same. The expert committee is being chaired by Shri C.K. Mishra, Former Secretary to Government of India, Ministry of Environment, Forest & Climate Change. The committee consists of leaders across the sustainable finance spectrum, including international agencies, standard setting bodies, funds, academia, and consultancies.

The constitution of the committee can be accessed through the following weblink:

Union Finance and Corporate Affairs Minister Smt. Nirmala Sitharaman has said that India needs four or five more banks like SBI. She said that we need to scale up banking to meet the changing requirements in light of shifting recent realities of economy and industry. “The way in which the economy is shifting to a different plane altogether, the way in which industry is adapting, so many new challenges keep arising. To address these challenges, we need not just more, but bigger banks.” The Union Minister shared this point of view with the banking community, during her keynote address at the 74th Annual General Meeting of the Indian Banks’ Association (IBA) in Mumbai today.

FM asks IBA to improve access to financial services pan India through scientific digitized mapping

The Finance Minister exhorted the industry to imagine how Indian banking has to be in the immediate and long-term future. “If we look at post-COVID scenario, India’s banking contour will have to be very unique to India, where there has been an extremely successful adoption of digitization. While banks in many countries could not reach out to their clients during the pandemic, the level of digitization of Indian banks helped us to transfer money to small, medium and big account holders through DBT and digital mechanisms.”

The Union Minister underlined the importance of seamless and interconnected digital systems in creating a sustainable future for Indian banking industry. “Long-term future of Indian banking is going to be largely driven by digitized processes.”

The benefits of digitization notwithstanding, the Finance Minister observed that there are wide disparities as well in access to financial services. She said there are parts of our country where brick-and-mortar banks are necessary. The FM asked IBA to improve access of banking in every district through a rationalized approach and optimal utilization of digital technologies.

To achieve this, the Union Minister advised IBA to carry out digitized location-wise mapping of all bank branches for every district of the nation. “Almost two-thirds of nearly 7.5 lakh panchayats have optical fibre connection, IBA should consider this and conduct an exercise and decide where banks should have a physical presence and where we are able to serve customers even without physical branch. IBA should take the initiative and complement government’s efforts for financial inclusion and enhancing access to financial services, especially in unserved and under-served areas.”

“Be nimble, agile, adaptive, it is a must for attaining 1 trillion dollar export target for 2030”

The Finance Minister reminded bankers of the need to adapt in line with fast changes in technology. “What we think is latest today will be outdated in a year or so, we have to thus acquire resources to constantly update ourselves.”

Such nimbleness and agility are especially important in India’s being able to achieve the ambitious export targets we have set for ourselves, she said. “We have given ourselves an export target of $ 2 trillion by 2030, $ 1 trillion in merchandise exports and $ 1 trillion in service exports. In an age of rapid change post the pandemic, there are going to be a lot of challenges in how we look at customers. These challenges cannot be addressed unless banks are going to be nimble, with sound understanding of various businesses and sectors. Hence, the banking industry needs specialists to understand the unique business requirements of diverse sectors and the many businesses who are rapidly relocating to India.”

The Finance Minister also spoke of the benefits of the recently formed Account Aggregator Framework. “If the framework is put to good use, we would not need specialized credit outreach. Govt. together with RBI has been helping with protocols and frameworks, helping banks attain more through the digital systems in the industry.”

The Finance Minister also spoke of the high potential for banking outreach in the eastern region of the country. “The eastern region of this country has more than adequate CASA (Current Account Saving Account), but there are no takers for credit; you need to address this issue and see how you can lend in those regions, in states such as Bihar.”

“Strengthen UPI”

The Finance Minister said that UPI needs to be strengthened. “In the payment world today, Indian UPI has actually made a very big impression. A RuPay card which was not as glamorous as a foreign card is now accepted in so many different parts of the world, symbolic of India’s futuristic digital payment intentions.” FinTech understands that UPI is its backbone, you have to give it its flesh and blood, you have to strengthen UPI, the Minister advised bankers.

“You ensured that bank amalgamation happened without friction”

The Finance Minister appreciated banks for executing amalgamation of banks even during the COVID-19 pandemic, without causing disruption in services to customers. “I commend that you ensured that amalgamation did not inconvenience customers, you ensured that systems of different banks spoke to each other, you have kept yourselves available during the pandemic in serving customers, while also ensuring that banks’ amalgamation happened without friction, without aberrations”, the Minister said.

“NARCL is not a bad bank”

Smt. Sitharaman thanked IBA for having come together in establishing the National Asset Reconstruction Company Ltd. and India Debt Resolution Company Ltd. “Working together, NARCL and IDRCL would be able to restructure and sell the NPAs.”

The Minister asserted that NARCL is not a bad bank. “It is a formulation which is intended to clean up banks’ assets and dispose of NPAs in a speedy manner. Banks are now able to raise money from the market, hence the burden on govt. to recapitalize banks will be less, this is how we want banks to function – a lot more professional, with a changed mindset.” The Finance Minister said that this is absolutely the right time to become professional. Bank valuations should be razor-sharp, enabling you to raise the right kinds of amount at the right cost, she said.

“Private sector DFIs needed to finance development needs”

The Minister underlined the importance and need for Development Finance Institutions, even in the private sector. ”Govt. is coming up with a Development Finance Institution, at the same time, we have made enough provisions for DFIs to come up in the private sector as well. We hope there is going to be good competition between public and private sector DFIs, so that money is available at competitive prices.”

The FM recalled that the Prime Minister has said that there needs to be a change and reset in our mindset and ways of living and hoped that IBA lives up to this invocation. “We are at a very critical stage of the Indian economy, you are the backbone for it, I wish IBA rises to this occasion and provides India the best of financial services.”

The Minister called for a reimagination and sprucing up of banks’ corporate communications, in line with changing realities of the new digital and connected age. Smt. Sitharaman, at the beginning of her address, paid homage to all members of the banking industry who lost their lives serving the nation through the COVID-19 pandemic.

MoS Bhagwat Karad commends banks for taking benefits of financial packages to people

Minister of State for Finance Dr. Bhagwat Kishanrao Karad commended banks for taking to the public the benefits of various financial stimulus packages including Aatma Nirbhar Bharat package, announced by the government in view of COVID-19 pandemic. The Minister said that all banks have to take special efforts in implementing EASE 3.0 and 4.0 Reforms and modernize banks. He also underlined the role of JAM Trinity, which is playing an important role in Direct Benefits Transfer, in taking govt. benefits directly to the people.

Earlier, Chairman of Indian Banks’ Association (IBA) Shri Rajkiran Rai G. welcomed the gathering, while Chief Executive, IBA, Shri Sunil Mehta gave a presentation on the 75-year journey of the Association. A detailed snapshot of this journey can be found in this IBA document here.

Secretary and Managing Committee Members of IBA; Managing Directors, CEOs and Executive Directors of the member banks of the Association too were present at the meeting. The programme can be watched here.

What isNational Asset Reconstruction Company Limited (NARCL)? Who has set it up?

NARCL has been incorporated under the Companies Act and has applied to Reserve Bank of India for license as an Asset Reconstruction Company (ARC). NARCL has been set up by banks to aggregate and consolidate stressed assets for their subsequent resolution. PSBs will maintain51% ownership inNARCL.

2. What is India Debt Resolution Company Ltd. (IDRCL)? Who has set it up?

IDRCL is a service company/operational entity which will manage the asset and engage market professionals and turnaround experts. Public Sector Banks (PSBs) and Public FIs will hold a maximum of 49% stake and the rest will be with private sector lenders.

3 Why is NARCL-IDRCL type structure needed when there are 28 existing ARCs?

Existing ARCs have been helpful in resolution of stressed assets especially for smaller value loans. Various available resolution mechanisms, including IBC have proved to be useful. However,considering the large stock of legacy NPAs, additional options/alternatives are needed and the NARCL-IRDCL structure announced in the Union Budget is this initiative.

4. Why is a Government Guarantee needed?

Resolution mechanisms of this nature which deal with a backlog of NPAs typically require a backstop from Government. This imparts credibility and provides for contingency buffers. Hence, GoI Guarantee of up to Rs 30,600 crore will back Security Receipts (SRs) issued by NARCL. The guarantee will be valid for 5 years. The condition precedent for invocation of guarantee would be resolution or liquidation. The guarantee shall cover the shortfall between the face value of the SR and the actual realisation. GoI’s guarantee will also enhance liquidity of SRs as such SRs are tradable.

5 How will NARCL and IDRCL work?

The NARCL will acquire assets by making an offer to the lead bank. Once NARCL’s offer is accepted, then, IDRCL will be engaged for management and value addition.

6 What benefit do banks get from this new structure?

It will incentivize quicker action on resolving stressed assets thereby helping in better value realization. This approach will also permit freeing up of personnel in banks to focus on increasing business and credit growth. As the holders of these stressed assets and SRs, banks will receive the gains. Further, it will bring about improvement in bank’s valuation and enhance their ability to raise market capital.

7 Why is it being set up now?

Insolvency and Bankruptcy Code (IBC), strengthening of Securitization and Reconstruction of Financial Assets and Enforcement of Securities Interest (SARFAESI Act) and Debt Recovery Tribunals, as well as setting up of dedicated Stressed Asset Management Verticals (SAMVs) in banks for large-value NPA accounts have brought sharper focus on recovery. In spite of these efforts, substantial amount of NPAs continue on balance sheets of banks primarily because the stock of bad loans as revealed by the Asset Quality Review is not only large but fragmented across various lenders. High levels of provisioning by banks against legacy NPAs has presented a unique opportunity for faster resolution.

8. Is the guarantee likely to be invoked?

Government guarantee will be invoked to cover the shortfall between the amount realised from the underlying assets and the face value of SRs issued for that asset, subject to overall ceiling of ₹30,600 crore, valid for 5 years. Since there shall be a pool of assets, it is reasonable to expect that realisation in many of them will be more than the acquisition cost.

9. How will Government ensure faster and timely resolution?

The GoI guarantee will be valid for five years and condition precedent for invocation of guarantee will be resolution or liquidation.Further, to disincentivize delay in resolution, NARCL has to pay a Guarantee fee which increase with passage of time.

10. What will be the capital structure of NARCL and how much will Government contribute?

Capitalization of NARCL would be through equity from banks and Non-Banking Financial Companies (NBFCs). it will also raise debt as required.The GoI guarantee will reduce upfront capitalization requirements.

11. What will be NARCL’s strategy for resolution of stressed assets?

NARCL is intended to resolve stressed loan assets above ₹500 crore each amounting to about ₹ 2 lakh crore. In phase I, fully provisioned assets of about Rs. 90,000 crores are expected to be transferred to NARCL, while the remaining assets with lower provisionswould be transferred in phase II.

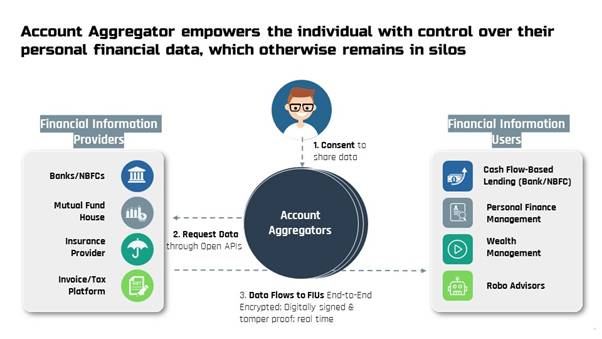

Last week India unveiled the Account Aggregator (AA) network, a financial data-sharing system that could revolutionize investing and credit, giving millions of consumers greater access and control over their financial records and expanding the potential pool of customers for lenders and fintech companies. Account Aggregator empowers the individual with control over their personal financial data, which otherwise remains in silos.

This is first step towards bringing open banking in India and empowering millions of customers to digitally access and share their financial data across institutions in a secure and efficient manner.

The Account Aggregator system in banking has been started off with eight of the India’s largest banks. The Account Aggregator system can make lending and wealth management a lot faster and cheaper.

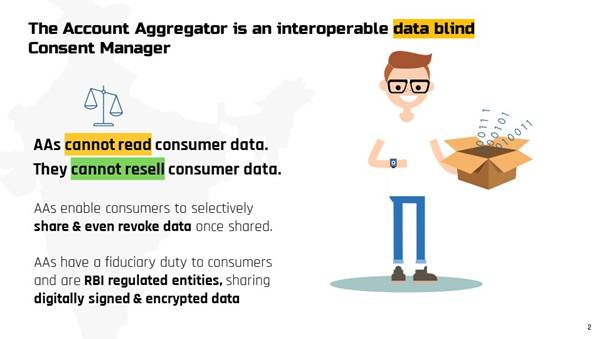

What is an Account Aggregator?

An Account Aggregator (AA) is a type of RBI regulated entity (with an NBFC-AA license) that helps an individual securely and digitally access and share information from one financial institution they have an account with to any other regulated financial institution in the AA network. Data cannot be shared without the consent of the individual.

There will be many Account Aggregators an individual can choose between.

Account Aggregator replaces the long terms and conditions form of ‘blank cheque’ acceptance with a granular, step by step permission and control for each use of your data.

2)How will the new Account Aggregator network improve an average person’s financial life?

India’s financial system involves many hassles for consumers today — sharing physical signed and scanned copies of bank statements, running around to notarise or stamp documents, or having to share your personal username and password to give your financial history to a third party. The Account Aggregator network would replace all these with a simple, mobile-based, simple, and safe digital data access & sharing process. This will create opportunities for new kinds of services — eg new types of loans.

The individual’s bank just needs to join the Account Aggregator network. Eight banks already have — four are already sharing data based on consent (Axis, ICICI, HDFC, and IndusInd Banks) and four are going to be able to shortly (State Bank of India, Kotak Mahindra Bank, IDFC First Bank, and Federal Bank).

3) How is Account Aggregator different to Aadhaar eKYC data sharing, credit bureau data sharing, and platforms like CKYC?

Aadhaar eKYC and CKYC only allow sharing of four ‘identity’ data fields for KYC purposes (eg name, address, gender, etc). Similarly, credit bureau data only shows loan history and/or a credit score. The Account Aggregator network allows sharing of transaction data or bank statements from savings/deposit/current accounts.

4) What kind of data can be shared?

Today, banking transaction data is available to be shared (for example, bank statements from a current or savings account) across the banks that have gone live on the network.

Gradually the AA framework will make all financial data available for sharing, including tax data, pensions data, securities data (mutual funds and brokerage), and insurance data will be available to consumers. It will also expand beyond the financial sector to allow healthcare and telecom data to be accessible to the individual via AA.

5) Can AAs view or ‘aggregate’ personal data? Is the data sharing secure?

Account Aggregators cannot see the data; they merely take it from one financial institution to another based on an individual’s direction and consent. Contrary to the name, they cannot ‘aggregate’ your data. AAs are not like technology companies which aggregate your data and create detailed profiles of you.

The data AAs share is encrypted by the sender and can be decrypted only by the recipient. The end to end encryption and use of technology like the ‘digital signature’ makes the process much more secure than sharing paper documents.

6) Can a consumer decide they don’t want to share data?

Yes. Registering with an AA is fully voluntary for consumers. If the bank the consumer is using has joined the network, a person can choose to register on an AA, choose which accounts they want to link, and share their data from one of their accounts for some specific purpose to a new lender or financial institution at the stage of giving ‘consent’ via one of the Account Aggregators. A customer can reject a consent to share request at any time. If a consumer has accepted to share data in a recurring manner over a period (eg during a loan period), it can also be revoked at any time later as well by the consumer.

7) If a consumer has shared my data once with an institution, for how long can they use it?

The exact time period for which the recipient institution will have access will be shown to the consumer at the time of consent for data sharing.

8) How can a customer get registered with an AA?

You can register with an AA through their app or website. AA will provide a handle (like username) which can be used during the consent process.

Today, four apps are available for download (Finvu, OneMoney, CAMS Finserv, and NADL) with operational licenses to be AAs. Three more have received in principle approval from RBI (PhonePe, Yodlee, and Perfios) and may be launching apps soon.

9) Does a customer need to register with every AA?

No, a customer can register with any AA to access data from any bank on the network.

10) Does a customer need to pay the AA for using this facility?

This will depend on the AA. Some AAs may be free because they are charging a service fee to financial institutions. Some may charge a small user fee.

11) What new services can a customer access if their bank has joined the AA network of data sharing?

The two key services that will be improved for an individual is access to loans and access to money management. If a customer wants to get a small business or personal loan today, there are many documents that need to be shared with the lender. This is a cumbersome and manual process today, which affects the time taken to procure the loan and access to a loan. Similarly, money management is difficult today because data is stored in many different locations and cannot be brought together easily for analysis.

Through Account Aggregator, a company can access tamper-proof secure data quickly and cheaply, and fast track the loan evaluation process so that a customer can get a loan. Also, a customer may be able to access a loan without physical collateral, by sharing trusted information on a future invoice or cash flow directly from a government system like GST or GeM.

/

/