Simplifying your business ideas, structures, functionalities, relations & operations

GST Articles, Video, PPT, Discussion, Expert Analysis

CBIC has waived the interest rate on account of the non-filing of GSTR-8 by certain ecommerce operators under section 52 of the Central Goods and Services Tax Act, 2017(the Act). Electronic Commerce Operators having the prescribed Goods and Services Tax Identification Numbers who could not file the statement under sub-section (4) of section 52 of the said Act, for the month of December 2020, by the due date, due to technical glitch on the portal but had deposited the tax collected under sub-section (1) of section 52 for the said month in the electronic cash ledger, interest will not be charged from the date of depositing the tax collected under subsection (1) of section 52 of the said Act in the electronic cash ledger till the date of filing of the statement under subsection (4) of section 52.

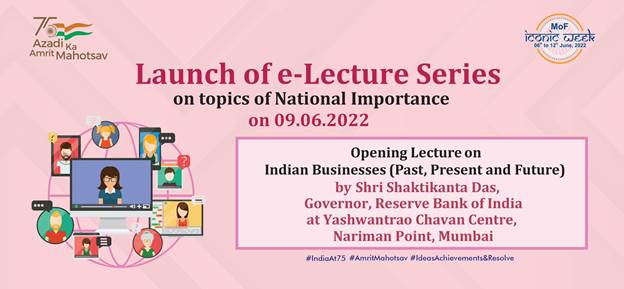

CBIC to launch “E-Lecture Series by Eminent Personalities on topics of national interest and indirect taxation” tomorrow

RBI Governor Shri Shaktikanta Das to give Opening Lecture on “Indian Businesses (Past, Present and Future)”

As part of celebrations of “ICONIC Week”, Central Board of Indirect Taxes & Customs (CBIC) is launching “E-Lecture Series by Eminent Personalities” tomorrow. The Ministry of Finance is celebrating the “ICONIC Week” from June 6th to 12th as part of the ‘Azadi Ka Amrit Mahotsav’ (AKAM) celebrations to mark the 75th year of India’s Independence. These celebrations were kick started by the Prime Minister, Shri Narendra Modi in New Delhi on 06th June, 2022.

Shri Shaktikanta Das, Governor, RBI, will be delivering the Opening Lecture on “Indian Businesses (Past, Present and Future)” at Yashwantrao Chavan Centre, Nariman Point, Mumbai on 9th June, 2022. The lecture will be attended by Shri Tarun Bajaj, Secretary, Revenue, Ministry of Finance, Government of India; Shri Vivek Johri, Chairman, CBIC, besides other members of CBIC.

Weblink of e-Lecture series: https://youtu.be/Mqxaoe_dJRI

The event is being hosted by the CBIC Chairman and organised by Mumbai Customs Zone-I. The event is also being attended by leading personalities of trade, industry and senior officials of Centre and State Govt. The event will be live steamed via the Internet on the CBIC YouTube Channel and the CBIC Facebook Page.

Sources: Ministry of Finance Press Release

Release Id :-1832193

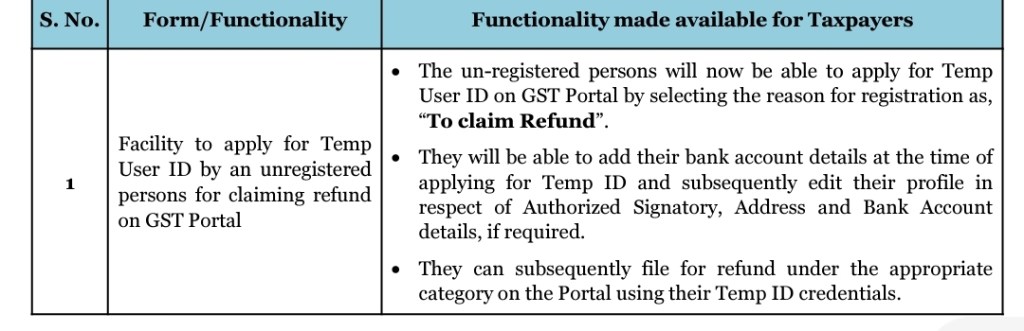

Form/Functionality : Bank Account Validation of Taxpayers

• To establish correctness of the bank account and to verify whether it matches with the PAN of the business, validation of the bank account details provided at the time of GST Registration/ Creation of Temp ID by the taxpayers is being done with CBDT database.

• The status based on validation result is displayed to the registered taxpayers and Temp ID holders on their dashboard.

• Taxpayers and Temp ID holders can verify their Bank account status in their profile by clicking on the Bank Account Status link under Quick Links.

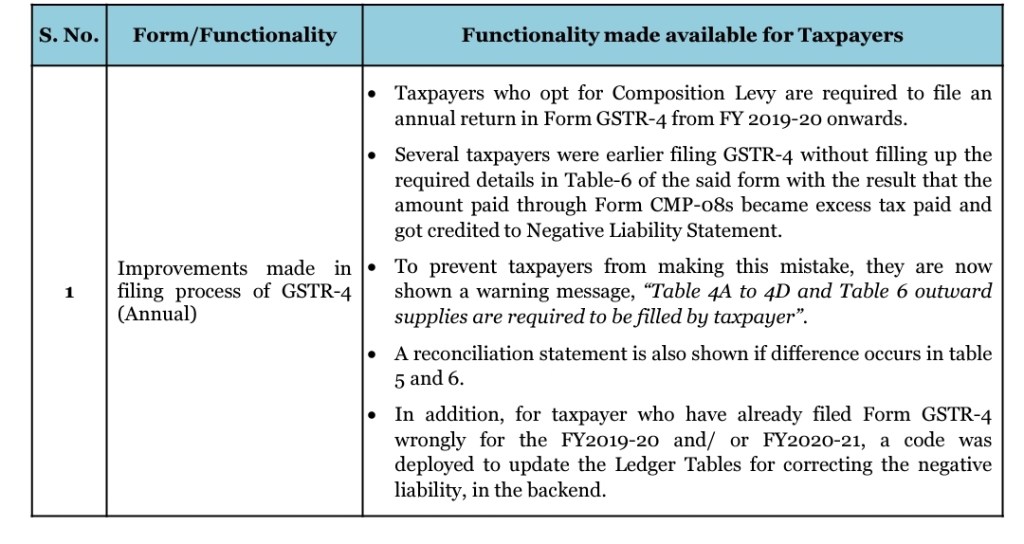

2. Returns

3. Refund

The option to add multiple Trade Names in GST has been activated in the GST Portal.

This option is available on the Business Details Tab.

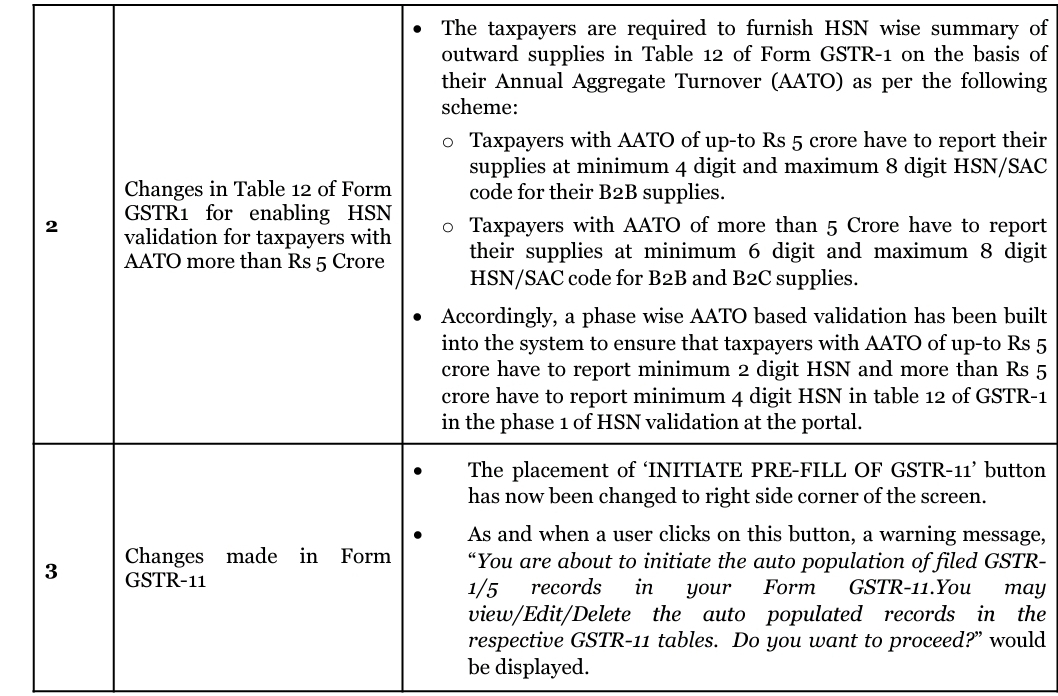

It may be noted that 6% tax rate has been added in the item details section of all the tables of form GSTR-1, except HSN table 12. In case your outward supplies attracts 6% tax rate, you are required to upload the details against 6% tax rate in the item details section.

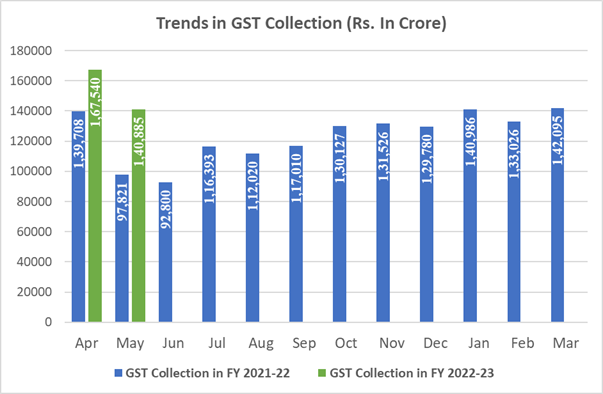

₹1,40,885 crore gross GST Revenue collection for May 2022; increase of 44% year-on-year

GST collection crosses ₹1.40 lakh crore mark 4th time since inception of GST; 3rd month at a stretch since March 2022

The gross GST revenue collected in the month of May 2022 is ₹1,40,885 crore of which CGST is ₹25,036 crore, SGST is ₹32,001 crore, IGST is ₹73,345 crore (including ₹ 37469 crore collected on import of goods) and cess is ₹10,502 crore (including ₹931 crore collected on import of goods).

The government has settled ₹27,924 crore to CGST and ₹23,123 crore to SGST from IGST. The total revenue of Centre and the States in the month of May 2022 after regular settlement is ₹52,960 crore for CGST and ₹55,124 crore for the SGST. In addition, Centre has also released GST compensation of ₹86912 crores to States and UTs on 31.05.2022.

The revenues for the month of May 2022 are 44% higher than the GST revenues in the same month last year of ₹97,821 crore. During the month, revenues from import of goods was 43% higher and the revenues from domestic transaction (including import of services) are 44% higher than the revenues from these sources during the same month last year.

This is only the fourth time the monthly GST collection crossed ₹1.40 lakh crore mark since inception of GST and third month at a stretch since March 2022. The collection in the month of May, which pertains to the returns for April, the first month of the financial year, has always been lesser than that in April, which pertains to the returns for March, the closing of the financial year. However, it is encouraging to see that even in the month of May 2022, the gross GST revenues have crossed the ₹1.40 lakh crore mark. Total number of e-way bills generated in the month of April 2022 was 7.4 crore, which is 4% lesser than 7.7 crore e-way bills generated in the month of March 2022.

The chart below shows trends in monthly gross GST revenues during the current year. The table shows the state-wise figures of GST collected in each State during the month of May 2022 as compared to May 2021.

State-wise growth of GST Revenues during May 2022

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1830039&RegID=3&LID=1

Reference:

EXCISE & TAXATION DEPARTMENT, HARYANA Memo No – 367/GST- 2 dated 24 May 2022

a) All applicants for registration are to be processed in accordance with provisions laid down in Section 25 and Rules framed there under.

b) The Act does not mandate physical appearance / personal statements of the applicants at the time of processing of registration. This practice shall be discouraged. However, in case of doubt/suspicion, physical verification of the business premises may be conducted under Rule 25 of the HGST Rules, 2017.

c) The list of documents to be uploaded with the application for registration are already provided in FORM GST REG-01. Ideally, no extraneous information/documents shall be sought by the Proper Officer while processing such applications. However, in case of doubt/suspicion, the proper officer may call for information as he may deem fit but information shall be relevant to the application and frivolous / extraneous information shall not be called for.

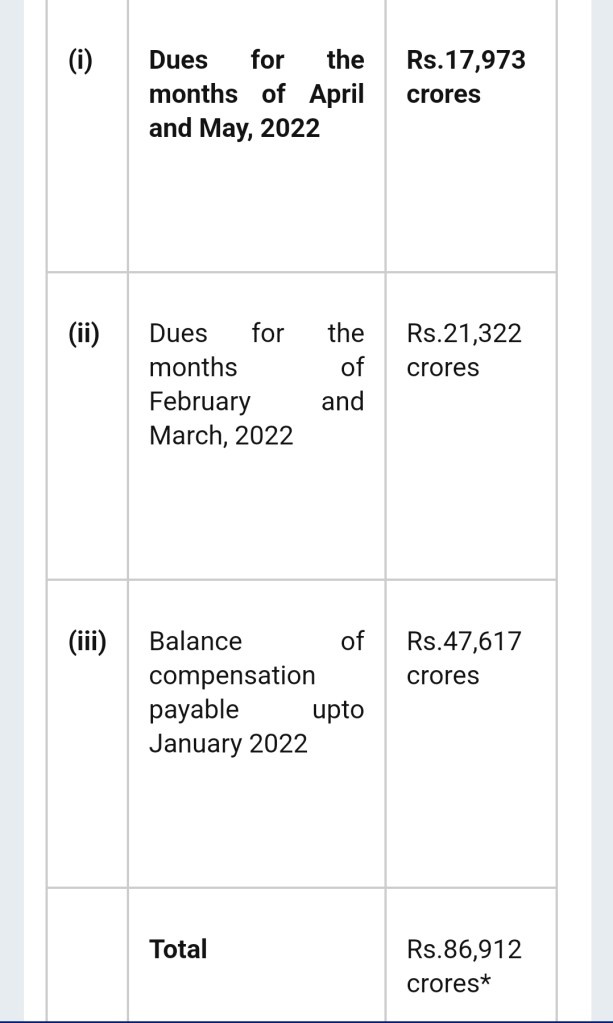

The Government of India has released the entire amount of GST compensation payable to States up to 31st May, 2022 by releasing an amount of Rs.86,912 crores. This decision was taken to assist the States in managing their resources and ensuring that their programmes especially the expenditure on capital is carried out successfully during the financial year. This decision has been taken despite the fact that only about Rs.25,000 crore is available in the GST Compensation Fund. The balance is being released by the Centre from its own resources pending collection of Cess.

Goods and Services Tax was introduced in the country w.e.f. 1st July, 2017 and States were assured for compensation for loss of any revenue arising on account of implementation of GST as per the provisions of the GST (Compensation to States) Act, 2017 for a period of five years. For providing compensation to States, Cess is being levied on certain goods and the amount of Cess collected is being credited to Compensation Fund. Compensation to States is being paid out of the Compensation Fund w.e.f. 1st July, 2017.

Bi-monthly GST compensation to States for the period 2017-18, 2018-19 was released on time out of the Compensation Fund. As the States’ protected revenue has been growing at 14% compounded growth whereas the Cess collection did not increase in the same proportion, COVID-19 further increased the gap between protected revenue and the actual revenue receipt including reduction in cess collection.

In order to meet the resource gap of the States due to short release of compensation, Centre has borrowed and released Rs.1.1 lakh crore in 2020-21 and Rs.1.59 lakh crore in 2021-22 as back-to-back loan to meet a part of the shortfall in cess collection. All the States have agreed to the above decision. In addition, Centre has also been releasing regular GST compensation from the Fund to meet the shortfall.

With the concerted efforts by Centre and States, gross monthly GST collection including Cess has been showing a remarkable progress. The details of GST compensation payable for the past financial years and for the period of April-May of the current financial year are given as per the table below: –

*State-wise break-up is given in a separate table.

With this release of Rs. 86,912 crore, the compensation to States till May 2022 gets fully paid and only compensation for June 2022 would remain.

Centre Clears Entire GST Compensation Due Till Date (31ST MAY, 2022)

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1829777&RegID=3&LID=1