Finance Act, 2021 inserted two new sections 206AB and 206CCA in the Income-tax Act 1961 which takes effect from 1st day of July, 2021. These sections mandate tax deduction or tax collection at higher rate in case of certain non-filers (specified persons). Higher rate is twice the prescribed rate or 5%, whichever is higher.

To implement these two provisions, tax deductor/collector was required to do a due diligence of satisfying himself if the deductee/collectee is a specified person. This would have resulted in extra compliance burden on such tax deductor/collector. To ease this compliance burden the Central Board of Direct Taxes has issued a new functionality “Compliance Check for Sections 206AB & 206CCA”. This functionality is already functioning through reporting portal of the Income-tax Department (https://report.insight.gov.in).

The tax deductor/collector can feed the single PAN (PAN search) or multiple PANs (bulk search) of the deductee/ coIIectee and can get a response from the functionality if such deductee/collectee is a specified person. For PAN Search, response will be visible on the screen which can be downloaded in the PDF format. For Bulk Search, response would be in the form of downloadable file which can be kept for record.

The logic of the functionality has been explained through CBDT Circular No. 11 of 2021 dated 21st June, 2021 available at (https://www.incometaxindia.gov.in/communications/circular/circular_11_2021.pdf). The Circular has further eased the burden of the tax deductors/collectors by ensuring that the deductors/collectors need to check the PAN in the functionality at the beginning of the financial year without there being any need to check the PAN of the non-specified person again during that financial year.

With this new functionality, the Government has reiterated its commitment to ease the compliance burden of taxpayers.

MOF issued Press release today (22 June 2021) interacting with tax professionals, other stakeholders and Infosys on issues in new Income Tax Portal.

A meeting was held between senior officials of the Finance Ministry and Infosys on 22.06.2021 on issues in the new Income Tax Portal. The meeting was presided over by Union Minister for Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman. Union Minister of State for Finance & Corporate Affairs, Shri Anurag Singh Thakur, also participated in the meeting. The interaction was attended by Shri Tarun Bajaj, Secretary Revenue; Shri J. B. Mohapatra, Chairman, CBDT; Smt. Anu J. Singh, Member (L & Systems), CBDT, and other senior officers of CBDT. Infosys was represented by its MD & CEO, Shri Salil Parekh and COO, Shri Praveen Rao and other members of their team. The meeting was also attended by 10 tax professionals from across the country, including representatives of ICAI and All India Federation of Tax Practitioners (AIFTP).

The new e-filing portal 2.0 of Income Tax Department (incometax.gov.in) went live on 07.06.2021. Since its launch, there were numerous glitches in the functioning of the new portal. Taking note of the grievances voiced on social media by taxpayers, tax professionals and other stakeholders, the Finance Minister had also flagged the issues to the vendor M/s Infosys, calling upon them to address these concerns. However, since the portal continued to be plagued by technical glitches causing inconvenience to taxpayers, it was decided to hold a meeting between Finance Ministry and Infosys as also other stakeholders here today. Suggestions in respect of the glitches on the portal were invited online by 18.06.2021. More than 700 emails detailing over 2,000 issues including 90 unique issues/problems in the portal were received in response to the same.

During the meeting, Smt. Sitharaman emphasised that enhanced taxpayer service is an important priority for the present Government and every effort should be made to amplify the same. While appreciating the role of ICAI and its president Shri Jambusaria and the ICAI’s positive contribution in giving shape to today’s meeting, the Finance Minister complimented them for providing specific nuanced inputs lying between the intersection of technology and taxation. Smt. Sitharaman also expressed her gratitude to the people who sent inputs through email and assured them that their suggestions would be taken up in all earnestness and would be addressed on priority.

The Finance Minister exhorted Infosys (service provider) to work on the tax portal to make it more humane and user-friendly and expressed her deep concern on the various problems being faced by the stakeholders in the new portal which was expected to provide a seamless experience to taxpayers.

Smt. Sitharaman asked Infosys to address all issues without further loss of time, improve their services, redress grievances on priority as it was impacting taxpayers adversely. The Finance Minister concluded her remarks by appreciating the taxpayers who have kept up with the timelines of compliances despite the COVID-19 pandemic. Smt. Sitharaman also hoped that the positive engagement between taxpayers, tax professionals and the Government would continue in future. The Finance Minister assured them that the Government is responsive to their problems and is proactively committed to enhance taxpayer service and experience.

The team from Infosys, which was led by the CEO and COO of Infosys, took note of the issues highlighted by the stakeholders. They also noted the observations and suggestions received from various users and stakeholders through email. The Infosys team acknowledged the technical issues in the functioning of the portal and shared the status of the resolution w.r.t the issues highlighted by the stakeholders. They informed that Infosys has been working to fix the technical issues noticed in the functioning of the portal and that they have augmented the resources for execution of the project on the hardware as well as the application side and that some of the issues have already been identified and fixed. For the other remaining technical issues, they assured that their teams were working on these issues and gave the expected timelines within which the issues such as e-proceedings, Form 15CA/15CB, TDS statements, DSC, viewing of past ITRs etc. are expected to be resolved in about a week. It was also decided that the timelines mentioned by Infosys to redress the issues would also be placed in public domain in due course.

This interaction was followed by another detailed meeting between senior officers of the Department of Revenue and the Infosys team, covering technical issues in the new portal.

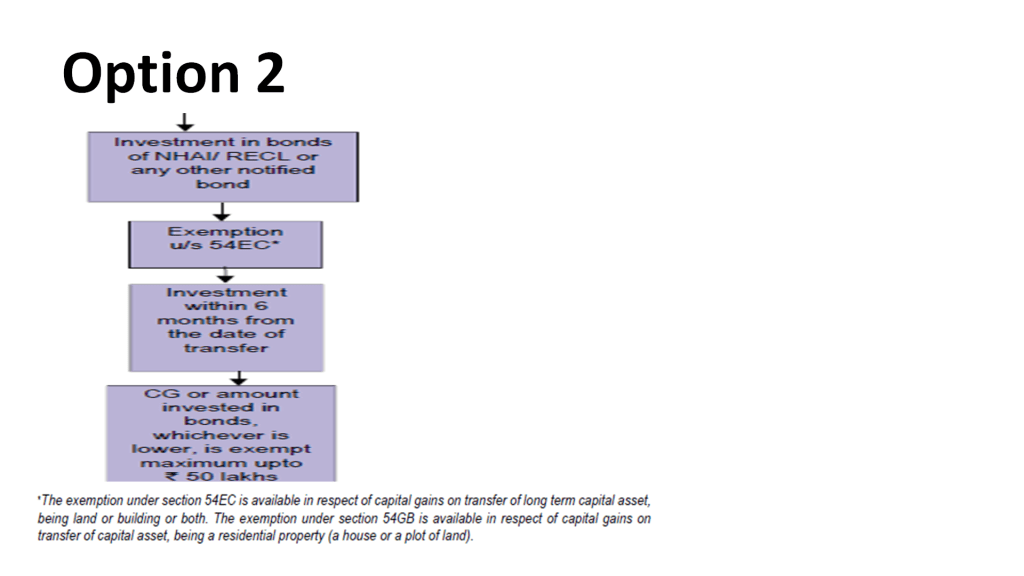

Holding residential house for 24 months or more is considered as Long term capital assets. Gain/profit arising from sale of residential house is considered as Short term capital gain or Long term capital gain as per period of holding of residential house. Here we are analysing available options to save taxes on long term capital gains on Sale of Residential house.

CBDT issued Circular No. 11 of 2021 dated 21.06.2021 on implementation of section 206AB & 206CCA with respect to higher tax deduction/collection for certain non-filers. New functionality issued for compliance checks for sec 206AB & 206CCA to ease compliance burden of tax deductors/collectors.

Ministry of Finance issued Press release today (19th June 2021) says that :

Certain reports have appeared in the media on 18.06.2021 stating that funds of Indians in Swiss Banks have risen to over Rs 20,700 crore (CHF 2.55 billion) at the end of 2020 from Rs 6,625 crore (CHF 899 million) at the end of 2019, reversing a 2 year declining trend. It has also been stated that this is also the highest figure of deposits in the last 13 years.

Media reports allude to the fact that the figures reported are official figures reported by banks to Swiss National Bank (SNB) and do not indicate the quantum of much debated alleged black money held by Indians in Switzerland. Further, these statistics do not include the money that Indians, NRIs or others might have in Swiss banks in the names of third–country entities.

However, the customer deposits have actually fallen from the end of 2019. The funds held through fiduciaries has also more than halved from end of 2019. The biggest increase is in “Other amounts due from customers”. These are in form of bonds, securities and various other financial instruments.

It is pertinent to point out that India and Switzerland are signatories to the Multilateral Convention on Mutual Administrative Assistance in Tax Matters (MAAC) and both countries have also signed the Multilateral Competent Authority Agreement (MCAA) pursuant to which, the Automatic Exchange of Information (AEOI) is activated between the two countries for sharing of financial account information annually for calendar year 2018 onwards.

Exchanges of Financial Account information in respect of residents of each country have taken place between both countries in 2019 as well as 2020. In view of the existing legal arrangement for exchange of information of financial accounts (which has a significant deterrent effect on tax evasion through undisclosed assets abroad), there does not appear to be any significant possibility of the increase of deposits in the Swiss banks which is out of undeclared incomes of Indian residents.

Further, the following factors could potentially explain the increase in deposits:

Increase in the deposits held by Indian companies in Switzerland owing to increased business transactions

Increase in deposits owing to the business of Swiss Bank branches located in India

Increase in Inter- bank transactions between Swiss and Indian Banks

A capital increase for a subsidiary of a Swiss Company in India and

Increase in the liabilities connected with the outstanding derivative financial instruments

The Swiss Authorities have been requested to provide the relevant facts along with their view on possible reasons for increase/decrease in the light of the media reports highlighted above.

To enjoy tax-exempt status in respect of their income, the NPOs must comply with certain pre-requisites such as obtaining the registration with the tax authorities, and spending on charitable activities at least up to the prescribed thresholds.

Not-for-profit organizations (NPOs) are private entities that pursue activities to promote the interest of the poor, protect the environment, and undertake various social welfare services for the benefit of the public at large.

In India, an NPO can be constituted in the form of a trust, society, or a company. All three forms are widely prevalent in the country. To encourage charitable activities, Indian tax law grants tax exemption to these philanthropic organizations. However, to enjoy tax-exempt status in respect of their income, the NPOs must comply with certain pre-requisites such as obtaining the registration with the tax authorities, and spending on charitable activities at least up to the prescribed thresholds. The activities of these organizations are largely funded by voluntary contributions. The Indian tax law allows the donor to claim the donation made to such exempt entities as an eligible deduction from its income, up to specified limits, irrespective of the tax category of such donor. However, these institutions are required to obtain a separate approval to qualify as ‘eligible donee’ and enable the donor to claim the deduction.

In the past few years, the government has made several changes in the laws governing the NPOs. Recently, some amendments were done in Income-tax Act related to NPOs vide Finance Act 2021.

One of the key changes is to streamline the tax registration and approval process for the NPOs. In the past, different tax officers adopted different yardsticks while granting approval for tax-exempt status. Every application was treated differently because of which NPOs faced some practical challenges.

On the other hand, it was also becoming difficult for the tax authorities to keep a check on the nature of activities undertaken by such entities. Thus, to standardize this process, the government has introduced a new scheme of registration and approval for the NPOs. While these changes were brought in a year ago, due to the ongoing pandemic, the implementation was deferred till 1 April 2021. The new framework not only covers the registration process but also changes the way donors can claim the benefit of tax deduction, which is discussed below.

New scheme of registration and approval for the NPOs-Key Highlights

— All existing as well as new NPOs must obtain registration under the new scheme to be eligible to claim tax exemption going forward. Even approval for ‘eligible donee’ is required to be re-validated as per the new norms. Applications for revalidation by NPO already approved should be made by 30 June 2021.

— Application for registration/ approval must be made online through the income-tax portal.

— Entities making an application for the first time may move an application even before the commencement of the activities. Provisional registration will be given in such cases. Subsequently, this should be converted into normal registration within the prescribed timelines.

— A Unique Registration Number will be allotted for each NPO upon granting of approval. This is in addition to Permanent Account Number (PAN) i.e. unique tax identification number required to be obtained under the domestic tax laws.

Undisposed applications

Applications made under the old scheme and pending for disposal as on 1 April 2021 shall be deemed to be applications made under the new scheme. Such applicants are not required to apply afresh under the new scheme. However, it is pertinent to note that detailed guidelines on how such pending applications will be considered under the new scheme by the tax administration while granting registration/ approval are awaited.

Introduction of validity period

Under the erstwhile provisions, approval once granted was perpetual unless specifically cancelled/surrendered. Now, all registration/approval shall be valid for a defined time.

Provisional registration shall be valid for a period of three years. Once activities are commenced, then such provisional registration needs to be converted into full-fledged approval within six months. In any case, normal registration should be applied at least six months before the expiry of provisional registration.

A normal registration shall be valid for a period of five years (including the period for which an NPO was provisionally registered). Thereafter, NPOs will have to get their registration renewed every five years to continue enjoying the tax benefits.

Disposal of application

Re-validation and provisional registration cases will be granted registration based on documents submitted at the time of making the application. No additional information is likely to be called upon by the tax authorities in such cases. However, all requests for renewals or conversion of provisional to normal registration etc. are likely to be subject to detailed scrutiny.

The department is obligated to dispose off the applications promptly. Further, an application can be rejected only after allowing the applicant to explain the case and recording reasons for such rejection, as applicable.

Incorrect or incomplete applications may lead to rejection of an application. This may happen even in the case of re-validation and provisional registration.

Also, if it is subsequently noticed by the tax authorities that the details submitted, or claims made by the organisations are incorrect, the department may cancel the registration. Such cancellation would be effective from the date of grant of registration/ approval. Hence, the NPOs should exercise caution while furnishing any information and/ or details along with the application and ensure that it is complete and accurate in all respects.

First-time applicant and renewals

At the stage of conversion of provisional into normal registration, tax authorities are likely to examine the nature of activities carried out by NPO in detail. Hence, necessary information/details should be kept ready to substantiate the information submitted in the application.

Also, NPOs are required to apply for renewal every five years. This would facilitate the tax authorities to re-examine the affairs of NPOs and satisfy themselves about the genuineness of the activities carried out by them.

NPOs should ensure their activities are always as per their charitable objectives. This should be supported by robust documentation. Further, adherence to compliances even under other governing laws is also important and may be examined at the time of renewal. The intention is to reduce roving inquiries made into the day-to-day affairs of tax-exempt entities, and instead focus on substantiating the key objectives for the which the NPO has been formed.

Filing a statement of donation

As discussed above, every NPO accepting donations will have to seek separate approval to be considered as ‘eligible donee’. Under the erstwhile mechanism, the NPOs were required to obtain such approval only once and did not have any further reporting obligations in respect of donations received. Going forward, all such entities will have to submit an Annual Statement in respect of donations received during the year with effect from the financial year 2021-22. It is intended to make the details of donations available in the centralized tax records of the taxpayer/donor basis this statement. The objective is to aid the donor in claiming the benefit at the time of filing his tax return. A deduction would be likely be available only for donations appearing in the tax records of donors. It seems that the process flow would be like one for withholding tax. This should help plug loopholes and help genuine donors in claiming the tax benefits. This will be possible through facilitation of one-on-one matching between donations received by exempt entities and donations claimed by the donor.

Key features of annual statement

— Reporting is required in respect of each receipt. Details of donors such as name, address, and the prescribed identification number are required to be reported. Furnishing incomplete details of donors may lead to denial of the tax benefit in the hands of the donor. On the other hand, this could have potential exposure of such donations being treated as “anonymous donation”, which would be taxable at a higher rate in the hands of donee.

— Donations of all kinds i.e. whether received in cash, kind or through cheque/ electronic payments should be reported. It is worth noting that cash donations over `2,000/- and donations in kind are not considered as eligible deduction.

— The annual statement can be rectified to correct mistakes. However, a detailed process for making such rectification is yet to be announced.

— A certificate of donation shall be issued to each donor. This certificate is likely to get generated based on the annual statement filed by the donee. Detailed procedure in respect of a generation of such certificate is yet to be announced.

— Delay in submission of annual statement or issuance of certificate may attract late fee and penalty.

The introduction of new scheme, interlinking of the eligible donation benefit with the annual statement is a welcome move. The changes introduced by the government shall ensure transparency in the functioning of the NPOs and their philanthropic activities to ensure that the intent is met both in law and spirit.

MOF in Press release today (16 June 2021) says that :

Net Direct Tax collections for the Financial Year 2021-22 have grown at over 100%

Advance Tax collections for F.Y. 2021-22 stand at Rs. 28,780 crore which shows a growth of approximately 146%

Net Direct Tax collections for the F.Y. 2021-22 have grown at a robust pace despite the disruption caused by the COVID-19 pandemic on the economy

Refunds amounting to Rs. 30,731 crore have been issued in the F.Y. 2021-22Posted Date:- Jun 16, 2021

The figures of Direct Tax collections for the Financial Year 2021-22, as on 15.06.2021 show that net collections are at Rs.1,85,871 crore compared to Rs. 92,762 crore over the corresponding period of the preceding year, representing an increase of 100.4% over the collections of the preceding year. The net Direct Tax collections include Corporation Tax (CIT) at Rs. 74,356 crore (net of refund) and Personal Income Tax(PIT) including Security Transaction Tax(STT) at Rs. 1,11,043 crore (net of refund).

The Gross collection of Direct Taxes(before adjusting for refunds) for the F.Y. 2021-22 stands at Rs. 2,16,602 crore compared to Rs. 1,37,825 crore in the corresponding period of the preceding year. This includes Corporation Tax(CIT) at Rs. 96,923 crore and Personal Income Tax (PIT) including Security Transaction Tax(STT) at Rs. 1,19,197 crore. Minor head wise collection comprises Advance Tax of Rs. 28,780 crore, Tax Deducted at Source of Rs.1,56,824 crore, Self-Assessment Tax of Rs. 15,343 crore; Regular Assessment Tax of Rs. 14,079 crore; Dividend Distribution Tax of Rs.1086 crore and Tax under other minor heads of Rs. 491 crore.

Despite extremely challenging initial months of the new Fiscal , the Advance Tax collections for the first quarter of the F.Y. 2021-22 stand at Rs. 28,780 crore against Advance Tax collections of Rs. 11,714 crore for the corresponding period of the immediately preceding Financial Year, showing a growth of approximately 146%. This comprises Corporation Tax(CIT) at Rs. 18,358 crore and Personal Income Tax (PIT) at Rs. 10,422 crore. This amount is expected to increase as further information is received from Banks.

Refunds amounting to Rs. 30,731 crore have also been issued in the F.Y. 2021-22.

Ministry of Finance issued Press release on 15th June says that Finance Ministry to hold meeting on 22nd June, 2021 with Infosys on issues in new Income Tax Portal

Senior officials of the Ministry of Finance, Government of India, will hold an interactive meeting on the 22nd of June, 2021, between 11:00 AM to 01:00 PM with Infosys (the vendor and its team) on issues/glitches in the recently launched e-filing portal of the Income Tax Department. Other stakeholders including members from ICAI, auditors, consultants and taxpayers will also be a part of the interaction. The new portal has been fraught with several technical glitches/issues leading to taxpayer inconvenience. Written representations on the problems/difficulties faced in the portal have also been invited from the stakeholders. Representatives from Infosys team will be present to answer queries, clarify issues and receive inputs on the working of the portal, to remove glitches and sort out issues faced by the taxpayers.