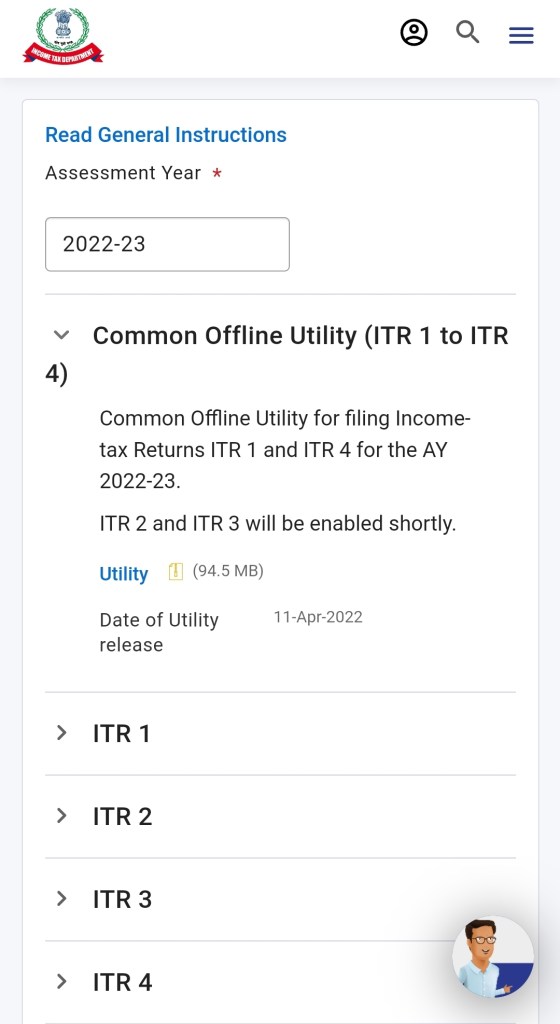

*Updates 12 April 2022* E-filing of ITR 1 and ITR 4 for AY 2022-23 enabled. Taxpayers can download ITR Offline Utility through “Downloads” Menu option, fill and file the ITR through the same. Online filing of these ITRs shall be enabled shortly.

Simplifying your business ideas, structures, functionalities, relations & operations

Income tax Articles, Video updates, PPT

*Updates 12 April 2022* E-filing of ITR 1 and ITR 4 for AY 2022-23 enabled. Taxpayers can download ITR Offline Utility through “Downloads” Menu option, fill and file the ITR through the same. Online filing of these ITRs shall be enabled shortly.

The tax revenue in the Union Budget for 2021-22 was estimated at ₹22.17 lakh crore against the revised estimates of ₹19 lakh crore, with a growth of 17%. The Union Budget was presented on 1st February, 2021 when the 1st COVID wave had tapered off in India but the world was facing successive waves.

Against the Union Budget estimates of ₹22.17 lakh crore, the revenue collections as per the pre-actual figures is ₹27.07 lakh crore, almost ₹5 lakh crore above the budget estimates. This is a growth of 34% over last years revenue collection of ₹ 20.27 lakh crore, led by growth of 49% in direct taxes and supported by 20% growth in indirect taxes. This revenue growth has been propelled by rapid economic recovery after successive waves of COVID, supported by one of the largest immunization programme of the world run by the Government. It also signifies a robust recovery in the economy. These was also supplemented with better compliance efforts in taxation. Various efforts were taken by tax administration on direct as well indirect taxes to nudge higher compliance through use of technology and artificial intelligence.

2021-22 marks the highest tax-GDP ratio of 11.7%, with direct tax to GDP ratio at 6.1% and indirect tax to GDP ratio at 5.6%. The tax buoyancy (which is a measure of growth in tax revenues as compared to GDP growth) is at a very healthy figure of 1.9, with 2.8 for direct taxes and 1.1 for indirect taxes. The ratio of direct to indirect taxes recovered from 0.9 in 2020-21 back to 1.1 in 2021-22.

The gross corporate taxes during 2021-22 was ₹8.6 lakh crore against ₹6.5 lakh crore last year, which shows that the new simplified tax regime with low rates and no exemptions has lived upto its promise. During the year, Income tax department gave refunds of ₹2.24 lakh core. During last two years, the effort has been to clear backlog of refunds to infuse liquidity into the hands of businesses. During the year, 2.4 crore refunds were issued that included 2.01 crore related to the year 2021-22, for which the returns were filed till 31st March 2021.

This has been possible due to faster processing of returns. During 2021-22, 22.4% returns were processed on the same day and around 75% returns were processed in less than a month time. The average processing time for returns during 2021-22 was 26 days. During the year, 7.14 crore returns were filed as compared to 6.97 crore last year.

On the indirect taxes, GST has seen an exemplary growth during 2021-22 despite two waves of COVID-19 pandemic. CGST revenues increased from ₹4.6 lakh crore last year to ₹5.9 lakh crore in 2021-22. The average monthly gross GST revenue in 2021-22 was ₹1.23 lakh crore as compared to ₹94,734 in 2020-21 and ₹1.01 lakh crore in 2019-20.

This again signifies a robust rebound in the economy. This has been complemented due to various measures taken to improve compliance. The GSTR-3B filing (percentage of returns of previous month filed till end of the month) improved from 74% in September 2020 to 87% in February 2022. The GSTR-1 filing has significantly improved from

54% in September 2020 to 82% in February 2022. This also shows that the gap between GSTR-3B filing and GSTR-1 filing has completely narrowed down to the level of elimination. This shows that the GST ecosystem has appreciated the invoice-based discipline in GST, which not only benefits GST revenues but also contributes to overall formalization in the economy.

The level of economic recovery can also be seen from the value of e-way bills generated every month, which has improved from ₹16.9 lakh crore in January 2021 to ₹25.7 lakh crore in March 2022.

During 2021-22, Customs duty has witnessed a growth rate of 48%. During last two years, Government has undertaken comprehensive review and rationalization of the Customs tariff structure through extensive consultations and crowd sourcing and has rationalized various exemptions and simplified the tariff structure.

It is expected that the trend of recovery in the economy and tax revenues of the Government will continue to grow.

On consideration of difficulties in electronic filing of Form No.10AB as stipulated in Rule 2C or 11AA or 17A of the Income-tax Rules, 1962, the Central Board of Direct Taxes (CBDT), extends the last date for electronic filing of Form No.10AB.

The application for registration or approval under Section 10(23C), 12A or 80G of the Act in Form No.10AB, for which the last date for filing falls on or before 29th September, 2022, is extended to 30th September, 2022.

CBDT’s Circular No.08/2022 in F. No. 197/59/2022-ITA-I dated 31.03.2022 has also been issued.

The Income Tax Department conducted a search and seizure operation on a leading automobile manufacturer group along with a company operating chartered flights and a real estate group of Delhi-NCR covering more than 35 premises across Delhi-NCR, on 23.03.2022.

During the course of the search operation, various incriminating documents and digital evidence have been found and seized indicating that the expenses ostensibly shown to have been claimed towards business purposes are not fully supported by evidences. Expenditure aggregating to more than Rs. 800 crore has been booked in the guise of purchase of services from a specific event management entity. This entity has siphoned-off the money by way of layering. Such claims towards non-business purposes are inadmissible expenditure under the provisions of the Income-tax Act, 1961.

In the search, it was also found that 10 acres of farm land at Delhi was purchased through few paper companies. In such transactions, unaccounted cash component of over Rs. 60 crore was purportedly involved. The ultimate/ real beneficiary of the land deal is a prominent person of the automobile manufacturer group. The intermediary who facilitated the said deal has admitted in his statement that major part of the sale consideration was paid in cash.

Apart from this, several incriminating documents have been unearthed from the premises of persons involved in the real estate business. These contain records of on-money transactions where cash was being received in lieu of sale of units in their various real estate projects across Delhi.

In the case of the company operating chartered flights, evidence related to booking of bogus expenses and non-recognition of income totalling to over Rs. 50 crore, rotation of funds and suspicious loans through a dubious NBFC floated by a key person, layering and re-routing of funds through paper companies and claiming bogus interest expenses, etc. have also been unearthed.

Undisclosed cash exceeding Rs. 1.35 crore has been seized and jewellery over Rs. 3 crore has been kept provisionally under restraint.

Further investigations are in progress.

The Central Board of Direct Taxes (CBDT) has entered into 62 Advance Pricing Agreements (APA) in FY 2021-22 with Indian taxpayers. This includes 13 Bilateral APAs (consequent to Mutual Agreement between India and its treaty partners) and 49 Unilateral APAs. With this, the total number of APAs since inception of the APA program has gone up to 421.

Despite severe economic and social disruption caused by the CoVID-19 pandemic in first part of the financial year, the number of APAs signed compares very well with the APAs signed in the preceding two years (31 APAs in FY 2020-21 and 57 APAs in FY 2019-20).

The APA Scheme endeavours to provide certainty to taxpayers in the domain of transfer pricing by specifying the methods of pricing and determining the arm’s length price of international transactions in advance for the maximum of five future years. Further, the taxpayer has the option to rollback the APA for four preceding years, as a result of which, total nine years of tax certainty is provided.

The progress of the APA scheme strengthens the Government’s resolve of fostering a non-adversarial tax regime and increasing the ease of doing business in India. CBDT appreciates the cooperative and transparent attitude of taxpayers in this regard.

Section 206C (1G) of the Income-tax Act, 1961 (“the Act”) provides for collection of tax by a seller of an overseas tour programme package from a buyer, being a person purchasing such package, at the rate of 5% of the amount of the package.

Representations were received from domestic tour operators who were facing difficulties in collection of tax from non-resident individuals visiting India who were booking overseas tour package from such domestic tour operators. Since such persons may not have a PAN, tax is required to be collected at higher rates. Further, such non-residents may find it difficult to furnish their ITR and claim refunds.

In order to remove such difficulties, the Central Government, in exercise of powers conferred under section 206C(1G) of the Act, has specified that the provisions of the said section shall not apply to a buyer being an individual who is not a resident in India in terms of clause (1) and clause (1A) of section 6 of the Act and who is visiting India. Hence, a domestic tour operator is not required to collect tax on sale of overseas tour package to non-resident individuals visiting India.

Notification No. 20 of 2022 dated 30.03.2022 has also been issued and is available on www.incometaxindia.gov.in under the Notification Section.

Under the provisions of the Income-tax Act, 1961 (“the Act”), every person who has been allotted a PAN as on 1st July, 2017 and is eligible to obtain Aadhaar Number, is required to intimate his Aadhaar to the prescribed authority on or before 31st March, 2022. On failure to do so, his PAN shall become inoperative and all procedures in which PAN is required shall be halted. The PAN can be made operative again upon intimation of Aadhaar to the prescribed authority after payment of a prescribed fee.

In order to mitigate the inconvenience to the taxpayers, as per Notification No.17/2022 dated 29th March, 2022, a window of opportunity has been provided to the taxpayers upto 31st of March, 2023 to intimate their Aadhaar to the prescribed authority for Aadhaar-PAN linking without facing repercussions. As a result, taxpayers will be required to pay a fee of Rs. 500 up to three months from 1st April, 2022 and a fee of Rs.1000 after that, while intimating their Aadhaar.

However, till 31st March, 2023 the PAN of the assessees who have not intimated their Aadhaar, will continue to be functional for the procedures under the Act, like furnishing of return of income, processing of refunds etc. A detailed Circular No.7/2022 dated 30.03.2022 has also been issued in this regard.

After 31st March, 2023, the PAN of taxpayers who fail to intimate their Aadhaar, as required, shall become inoperative and all the consequences under the Act for not furnishing, intimating or quoting the PAN shall apply to such taxpayers.

The Income Tax Department carried out a search and seizure operation on 14.03.2022 on a popular chain of educational institutes, running several schools and colleges at multiple locations in India and abroad. The search operation covered more than 25 premises spread over locations in Maharashtra, Karnataka and Tamil Nadu.

During the search, several incriminating evidences including hard copy documents and digital data have been found and seized, which reveal that substantial funds have been siphoned-off from the Trusts for the personal benefit of the group’s promoters and their family members, in violation of provisions relating to claim of exemption by the Trusts under the Income-tax Act, 1961.

The modus operandi of siphoning-off the funds from the Trusts includes debiting of bogus expenses in the guise of purchase of goods/services from various dummy companies and LLPs owned by the promoters, their family members, and some of their trusted employees. It was unearthed that no actual goods/services were delivered/rendered by these entities and the same have been corroborated by the employees in their deposition. The money so siphoned-off has been utilised for investment in acquiring benami properties and making unfair payments.

During the search, evidences of about two dozen immovable properties located in Maharashtra, Pondicherry and Tamil Nadu have also been gathered which are either benami properties or not disclosed in the respective returns of Income. These properties have been placed under provisional attachment.

The search also revealed evidences of borrowings on Hundi aggregating to Rs. 55 crore, and their repayment in cash in the form of discharged Promissory Notes/Bills of Exchange, which were found & seized.

The search action has resulted in the seizure of unaccounted cash of Rs. 27 lakh and jewellery worth Rs. 3.90 crore.

Further investigations are in progress.

Income Tax Department conducted a Search & Seizure operation on a Pune & Thane based unicorn start-up group, primarily engaged in the business of wholesale and retail of construction material, on 09.03.2022. The group has Pan-India presence having annual turnover exceeding Rs. 6,000 crore. A total of 23 premises were covered in Maharashtra, Karnataka, Andhra Pradesh, Uttar Pradesh and Madhya Pradesh, in the search operation.

A large number of incriminating evidences in the form of hard copy documents and digital data have been found & seized during the search operations. These evidences revealed that the group has booked bogus purchases, made huge unaccounted cash expenditure and obtained accommodation entries, aggregating to the tune of over Rs. 400 crore. These evidences were confronted to the Directors of the group, who admitted under oath this modus operandi, disclosed additional income of more than Rs. 224 crore in various assessment years, and consequently offered to pay their due tax liability.

The search action also revealed that the group had obtained huge foreign funding via the Mauritius route, by issuing shares at exorbitantly high premium.

During the search operation, a complex hawala network of some Mumbai and Thane based shell companies, was also unearthed. These shell companies exist on paper, and were created only for the purpose of providing accommodation entries. Preliminary analysis has revealed that the total quantum of accommodation entries provided by these shell entities exceeds Rs. 1,500 crore.

So far, unaccounted cash of Rs. 1 crore and jewellery of the value of Rs. 22 lakh have been seized.

Further investigations are under progress.