Income Tax Department carried out search and seizure operations on 16.06.2022 on a business group involved in retail and export sale of handicrafts, cash financing, purchase and sale of land and buildings, alongwith some bullion traders. The search operation covered more than 25 premises spread across Rajasthan and Mumbai.

During the course of the search operation, several incriminating documents have been found and seized. The perusal of seized evidences indicates that the group has indulged in unaccounted cash transactions in real estate business as well as obtaining bogus purchase bills. The modus operandi of the group has been to suppress profits of the handicrafts business by inflating the purchases in the books of account, through bogus bills of gold and silver arranged from bullion traders. During the search, it has also been seen that cash has been received back against the cheques issued to these bullion traders.

Cash was found to be utilised for investment in real estate as well as for obtaining cheques to be introduced as credits into the books of account. The seized evidence also revealed that the group recently acquired few shell companies through entry operators.

The search action has led to seizure of unaccounted cash exceeding Rs. 1.30 crore and unaccounted gold jewellery exceeding Rs. 7.90 crore. Prima facie, estimated unaccounted income in excess of Rs. 100 crore has been unearthed, so far.

Finance Act 2022 inserted a new section 194R in the Income-tax Act, 1961 (hereinafter referred to as “the Act”) w.e.f. 01st July 2022. The new section mandates a person, who is responsible for providing any benefit or perquisite to a resident, to deduct tax at source @10% of the value or aggregate of value of such benefit or perquisite, before providing such benefit or perquisite.

The benefit or perquisite may or may not be convertible into money but should arise either from carrying out of business, or from exercising a profession, by such resident.

This deduction is not required to be made, if the value or aggregate of value of the benefit or perquisite provided or likely to be provided to the resident during the financial year does not exceed twenty thousand rupees.

The responsibility of tax deduction also does not apply to a person, being an Individual/Hindu undivided family (HUF) deductor, whose total sales / gross receipts / gross turnover from business does not exceed one crore rupees, or from profession does not exceed fifty lakh rupees, during the financial year immediately preceding the financial year in which such benefit or perquisite is provided by him.

CBDT Circular No. 12 of 2022 dated 16th June 2022

Clarification 1:

Question 1. Is it necessary that the person providing benefit or perquisite needs to check if the amount is taxable under clause (iv) of section 28 of the Act, before deducting tax under section 194R of the Act?

Section 28 The following income shall be chargeable to income-tax under the head “Profits and gains of business or profession”, (iv) the value of any benefit or perquisite, whether convertible into money or not, arising from business or the exercise of a profession ;

Answer: No. The deductor is not required to check whether the amount of benefit or perquisite that he is providing would be taxable in the hands of the recipient under clause (iv) of section 28 of the Act.

The amount could be taxable under any other section like section 41(1) etc.

Section 194R of the Act casts an obligation on the person responsible for providing any benefit or perquisite to a resident, to deduct tax at source @10%.

There is no further requirement to check whether the amount is taxable in the hands of the recipient or under which section it is taxable.

In this regard it may be highlighted that in the context of section 195 of the Act it is a requirement to know whether the payment made by the deductor is income in the hands of the non-resident recipient as section 195 of the Act requires deduction on any other sum chargeable under the provisions of this Act at the rates in force. Thus there is requirement that deductor needs to verify if the “sum is chargeable under the Income-tax Act”. The term “rate in force” is defined in clause (37A) of section 2 of the Act and it allows benefit of agreement under section 90 or section 90A of the Act, if eligible, in determining the rate of tax at which the tax is to be deducted at source.

Hence, there is further requirement of checking if the amount is taxable under tax treaty and if yes, at what rate.

Such a requirement is not there in section 194R of the Act, in the absence of these two terms in this section.

Hence, there is no requirement for deductor to verify whether the amount is taxable in the hands of the recipient or section under which it is taxable.

It may also be highlighted that these two terms are also not there in section 194E (Section 194E TDS on Payments to Non-Resident Sportsmen or Sports Association ) of the Act and Hon’ble Supreme Court in the case of PILCOM vs. CIT West Bengal (Civil Appeal No. 5749 of 2012), held that tax is to be deducted under section 194E of the Act at a specific rate indicated there in and there is no need to see the taxability or the rate of taxability in the hands of the non-resident.

Clarification 2:

Question 2. Is it necessary that the benefit or perquisite must be in kind for section 194R of the Act to operate?

Answer: Tax under section 194R of the Act is required to be deducted whether the benefit or perquisite is in cash or in kind.

In this regard it is important to draw attention to the first proviso to sub-section (1) of section 194R of the Act, which reads as under:

“Provided that in a case where the benefit or perquisite, as the case may be, is wholly in kind or partly in cash and partly in kind but such part in cash is not sufficient to meet the liability of deduction of tax in respect of whole of such benefit or perquisite, the person responsible for providing such benefit or perquisite shall, before releasing the benefit or perquisite, ensure that tax required to be deducted has been paid in respect of the benefit or perquisite:”

This proviso clearly indicates the intent of legislature that there could also be situations where benefit or perquisite is in cash or the benefit or perquisite is in kind or partly in cash and partly in kind.

Thus, section 194R of the Act clearly brings in its scope the situation where the benefit or perquisite is in cash or in kind or partly in cash or partly in kind.

Clarification 3:

Question 3. Is there any requirement to deduct tax under section 194R of the Act, when the benefit or perquisite is in the form of capital asset?

Answer: As has been stated in response to question no 1, there is no requirement to check whether the perquisite or benefit is taxable in the hands of the recipient and the section under which it is taxable.

Further, courts have held many benefits or perquisites to be taxable even though one can argue that they are in the nature of capital asset.

The following judgments illustrate this point:

Assessee entered into an agreement with `.1′ for purchase of a plot of land and certain amount was paid as earnest money. However, possession of land was not given to assessee and seller entered into another agreement with a third party to develop the said plot. Assessee filed suit in which a consent decree was passed and in pursuance of same certain amount as paid to assessee. On appeal it was held that such sum received in pursuance of consent decree was liable to tax as business income under section 28(iv). Ramesh Babulal Shah v CIT (2015) 53 taxmann.com 277 (Born)

The amount representing principal loan waived by bank under one time settlement scheme would constitute income falling under section 28(iv) relating to value of any benefit or perquisite, arising from business or exercise of profession. CIT v Rainaniyam Homes (P) Ltd (2016) 68 taxmann.com 289 (Mad)

Value of rent free accommodation, furniture and fixtures given to director was held as taxable under section 28(iv). CIT v Subrata Roy (2016) 385ITR 547 (All)

Where a car was given to an assessee by his disciple, who had been benefited from his preaching, the value of car was held to be taxable in the hands of the assessee being a receipt from the exercise of the vocation carried on by him. CIT (Addl) v Rain Kripal Tripathi (1980) 125 ITR 408 (All)

The assessee was a director of a company. In terms of an agreement with the promoters, shares were allotted to the director. On these facts, it was held that the shares received by the director were benefit or perquisite received from a company by the director and it was a benefit assessable to tax. D. M. Neterwala v CIT (1986) 122 ITR 880 (Born)

Value of gift of land was held as a receipt by the assessee in carrying on of his vocation and was held as taxable. Amarendra Nath Chakraborty v CIT (1971) 79 ITR 342 (Cal)

Thus, it can be seen that the asset given as benefit or perquisite may be capital asset in general sense of the term like car, land etc but in the hands of the recipient it is benefit or perquisite and has accordingly been held to be taxable. In any case, as stated earlier, the deductor is not required to check if the benefit or perquisite is taxable in the hands of recipient. Thus, the deductor is required to deduct tax under section 194R of the Act in all cases where benefit or perquisite (of whatever nature) is provided.

Clarification 4:

Question 4: Whether sales discount, cash discount and rebates are benefit or perquisite?

Answer: Sales discounts, cash discount or rebates allowed to customers from the listed retail price represent lesser realization of the sale price itself. To that extent purchase price of customer is also reduced.

Logically these are also benefits though related to sales/purchase. Since TDS under section 194R of the Act is applicable on all forms of benefit/perquisite, tax is required to be deducted. However, it is seen that subjecting these to tax deduction would put seller to difficulty.

To remove such difficulty it is clarified that no tax is required to be deducted under section 194R of the Act on sales discount, cash discount and rebates allowed to customers.

Clarification 5:

Question 5. How is the valuation of benefit/perquisite required to be carried out?

Answer: The valuation would be based on fair market value of the benefit or perquisite except in following cases:-

The benefit/perquisite provider has purchased the benefit/perquisite before providing it to the recipient. In that case the purchase price shall be the value for such benefit/perquisite.

The benefit/perquisite provider manufactures such items given as benefit/perquisite, then the price that it charges to its customers for such items shall be the value for such benefit/perquisite. It is further clarified that GST will not be included for the purposes of valuation of benefit/perquisite for TDS under section 194R of the Act.

Clarification 6:

Question 6: Many a times, a social media influencer is given a product of a manufacturing company so that he can use that product and make audio/video to speak about that product in social media. Is this product given to such influencer a benefit or perquisite?

Answer: Whether this is benefit or perquisite will depend upon the facts of the case. In case of benefit or perquisite being a product like car, mobile, outfit, cosmetics etc and if the product is returned to the manufacturing company after using for the purpose of rendering service, then it will not be treated as a benefit/perquisite for the purposes of section 194R of the Act. However, if the product is retained then it will be in the nature of benefit/perquisite and tax is required to be deducted accordingly under section 194R of the Act.

Question 7: Whether reimbursement of out of pocket expense incurred by service provider in the course of rendering service is benefit/perquisite?

Answer: Any expenditure which is the liability of a person carrying out business or profession, if met by the other person is in effect benefit/perquisite provided by the second person to the first person in the course of business/profession.

Let us assume that a consultant is rendering service to a person “X” for which he is receiving consultancy fee. In the course of rendering that service, he has to travel to different city from the place where is regularly carrying on business or profession. For this purpose, he pays for boarding and lodging expense incurred exclusively for the purposes of rendering the service to “X”. Ordinarily, the expenditure incurred by the consultant is part of his business expenditure which is deductible from the fee that he receives from company “X”. In such a case, the fee received by the consultant is his income and the expenditure incurred on travel is his expenditure deductible from such income in computing his total income. Now if this travel expenditure is met by the company “X”, it is benefit or perquisite provided by “X” to the consultant.

However, sometimes the invoice is obtained in the name of “X” and accordingly, if paid by the consultant, is reimbursed by “X”. In this case, since the expense paid by the consultant (for which reimbursement is made) is incurred wholly and exclusively for the purposes of rendering services to “X” and the invoice is in the name of “X”, then the reimbursement made by “X” being the service recipient will not be considered as benefit/perquisite for the purposes of section 194R of the Act.

If the invoice is not in the name of “X” and the payment is made by “X” directly or reimbursed, it is the benefit/perquisite provided by “X” to the consultant for which deduction is required to be made under section 194R of the Act.

Question 8: If there is a dealer conference to educate the dealers about the products of the company – Is it benefit/perquisite?

Answer: The expenditure pertaining to deafer/business conference would not be considered as benefit/perquisite for the purposes of section 194R of the Act in a case where dealer/business conference is held with the prime object to educate dealers/customers about any of the following or similar aspects:

new product being launched

discussion as to how the product is better than others

obtaining orders from dealers/customers

teaching sales techniques to dealers/customers

addressing queries of the dealers/customers

reconciliation of accounts with dealers/customers

However, such conference must not be in the nature of incentives/benefits to select dealers/customers who have achieved particular targets.

Further, in the following cases the expenditure would be considered as benefit or perquisite for the purposes of section 194R of the Act:-

Expense attributable to leisure trip or leisure component, even if it is incidental to the dealer/business conference.

Expenditure incurred for family members accompanying the person attending dealer/business conference

Expenditure on participants of dealer/business conference for days which are on account of prior stay or overstay beyond the dates of such conference.

Question 9: Section 194R provides that if the benefit/perquisite is in kind or partly in kind (and cash is not sufficient to meet TDS) then the person responsible for providing such benefit or perquisite is required to ensure that tax required to be deducted has been paid in respect of the benefit or perquisite, before releasing the benefit or perquisite. How can such person be satisfied that tax has been deposited?

Answer: The requirement of law is that if a person is providing benefit in kind to a recipient and tax is required to be deducted under section 194R of the Act, the person is required to ensure that tax required to be deducted has been paid by the recipient. Such recipient would pay tax in the form of advance tax. The tax deductor may rely on a declaration along with a copy of the advance tax payment challan provided by the recipient confirming that the tax required to be deducted on the benefit/perquisite has been deposited. This would be then required to be reported in TDS return along with challan number. This year Form 26Q has included provisions for reporting such transactions.

In the alternative, as an option to remove difficulty if any, the benefit provider may deduct the tax under section 194R of the Act and pay to the Government. The tax should be deducted after taking into account the fact the tax paid by him as TDS is also a benefit under section 194R of the Act. In the Form 26Q he will need to show it as tax deducted on benefit provided.

Question 10. Section 194R would come into effect from the 1St July 2022. Second proviso to subsection (1) of section 194R of the Act provides that the provision of this section does not apply where the value or aggregate of value of the benefit or perquisite provided or likely to be provided to a resident during the financial year does not exceed twenty thousand rupees. It is not clear how this limit of twenty thousand is to be computed for the Financial Year 2022-23?

Answer: It is hereby clarified that,-

Since the threshold of twenty thousand rupees is with respect to the financial year, calculation of value or aggregate of value of the benefit or perquisite triggering deduction under section 194R of the Act shall be counted from 1st April, 2022. Hence, if the value or aggregate value of the benefit or perquisite provided or likely to be provided to a resident exceeds twenty thousand rupees during the financial year 2022-23 (including the period up to 30th June 2022), the provision of section 194R shall apply on any benefit or perquisite provided on or after July 2022.

The benefit or perquisite which has been provided on or before 30th June 2022, would not be subjected to tax deduction under section 194R of the Act.

Is all type of benefits or perquisites taxable now? I Newly inserted Section 194R of Income Tax Act, 1961 (W.e.f. 01st July 2022)

✒️ Section 194 R –An Introduction (w.e.f. 01st July 2022)

✒️ Whether deductor is required to be check taxability of Benefits/perquisites in the hands of recipient?

✒️ Is Section 194 R apply on Capital asset provided as Benefits/perquisites ?

✒️ Whether sales discount, cash discount and rebates are benefit or perquisite?

✒️ How is the valuation of benefit/perquisite required to be carried out?

✒️ Whether reimbursement of out of pocket expense incurred by service provider in the course of rendering service is benefit/perquisite?

✒️ Threshold limit for FY 2022-23-How to check for applicability

✒️ TDS deposit & compliances in case of benefits or perquisites provided in Kind

For some of the taxpayers, there was an issue in relation to duplicate entries in GSTR2B which has since been fixed and correct GSTR 2B has been generated. In this regard, taxpayers while filing GSTR3B are advised to check and ensure that the value of ITC they are availing is correct as per the law.

They may check the correct ITC value from download of Auto drafted ITC statement GSTR2B or pdf of System Generated GSTR3B or on the ITC observed on the mouse hover of Table 4 in GSTR3B, particularly in any such case where there is any difference observed between the correct figures available at places as stated above and the prefilled GSTR3B observed on screen.

Net Direct Tax collections for the Financial Year 2022-23 grown at over 45%

Net Direct Tax collections for the F.Y. 2022-23 continue to grow at a robust pace further fortifying the economic revival

Gross Tax collections for the Financial Year 2022-23 grown at about 40%

Advance Tax collections for F.Y. 2022-23 stand at Rs. 1,01,017 crore which shows a growth of more than 33%

Refunds amounting to Rs. 30,334 crore issued in the F.Y. 2022-23

The figures of Direct Tax collections for the Financial Year 2022-23, as on 16.06.2022 show that net collections are at Rs.3,39,225 crore compared to Rs. 2,33,651 crore over the corresponding period of the preceding year, representing an increase of 45% over the collections of the preceding year. The net collection (as on 16.06.2022) in F.Y. 2022-23 has registered a growth of 171% over the corresponding period of F.Y. 2020-21 when the net collection was Rs. 1,25,065 crore, and a growth of 103% over the corresponding period of F.Y. 2019-20 when the net collection was Rs. 1,67,432 crore.

The Net Direct Tax collection of Rs. 3,39,225 crore (as on 16.06.2022) include Corporation Tax (CIT) at Rs. 1,70,583 crore (net of refund) and Personal Income Tax (PIT) including Security Transaction Tax (STT) at Rs. 1,67,960 crore (net of refund).

The Gross collection of Direct Taxes (before adjusting for refunds) for the F.Y. 2022-23 stands at Rs. 3,69,559 crore compared to Rs. 2,64,382 crore in the corresponding period of the preceding year, representing an increase of almost 40% over the collections of the preceding year. This includes Corporation Tax (CIT) at Rs. 1,90,651 crore and Personal Income Tax (PIT) including Security Transaction Tax (STT) at Rs. 1,78,215 crore. Minor head wise collection comprises Advance Tax of Rs. 1,01,017 crore, Tax Deducted at Source of Rs.2,29,676 crore, Self-Assessment Tax of Rs. 21,849 crore, Regular Assessment Tax of Rs. 10,773 crore, Tax on Distributed Profits of Rs. 5,529 crore and Tax under other minor heads of Rs. 715 crore.

The Advance Tax collections for the first quarter of the F.Y. 2022-23 stand at Rs. 1,01,017 crore against Advance Tax collections of Rs. 75,783 crore for the corresponding period of the immediately preceding Financial Year, showing a growth of more than 33%. This comprises Corporation Tax (CIT) at Rs. 78,842 crore and Personal Income Tax (PIT) at Rs. 22,175 crore. This amount is expected to increase as further information is received from Banks.

The TDS collections for F.Y. 2022-23 (as on 16.06.2022) stand at Rs. 2,29,676 crore against TDS collections of Rs. 1,57,434 crore for the corresponding period of the immediately preceding Financial Year, showing a growth of nearly 46%.

The Self-Assessment Tax collections for F.Y. 2022-23 (as on 16.06.2022) stand at Rs. 21,849 crore against self-assessment tax collections of Rs. 15,483 crore for the corresponding period of the immediately preceding Financial Year, showing a growth of more than 41%.

Refunds amounting to Rs. 30,334 crore have also been issued in the F.Y. 2022-23.

Disruptions & Opportunities in the Financial Sector (Address by Shri Shaktikanta Das, Governor, Reserve Bank of India – June 17, 2022 – Delivered at the Financial Express Modern BFSI Summit in Mumbai)

It is my pleasure to be here amongst such a distinguished gathering to deliver the inaugural address at the Financial Express Modern BFSI Summit. The theme of my address “Disruptions & Opportunities in the Financial Sector’ will resonate in the current context of technological innovations and fast evolving business models in the financial sector.

2. The impact of Covid-19 pandemic, the recent geo-political crisis and the all-pervasive technological innovations sweeping across economies are challenging the traditional financial intermediation processes. In my address today, I would like to focus more on the banking and the financial services space. I propose to share my thoughts on possible implications of technology on the financial services industry.

The Changing Paradigm of Banking

3. The edifice of growth and development in modern economies is built on the foundation of a vibrant, resilient and well-functioning financial sector. The core functions of the financial sector in an economy, viz. intermediation, asset price discovery, risk transfer and payments are globally undergoing a process of transformation. This is primarily driven by technological advancements. The Indian financial sector has also been a part of this churning and is adopting and propelling these transformations.

4. Over the past few years, the business of banking has witnessed a shift from traditional branch banking to digital banking. This paradigm shift has been possible due to innovations in information technology (IT), growth in mobile and internet connectivity, market-based financial intermediation, and the advent of Fintech. Financial service providers are now devising new products and services and are adopting new business models for reaching out to the target customers.

5. Improvements in technology have also enhanced the cause of financial inclusion and tech-enabled public goods delivery. Direct Benefit Transfer (DBT) through the digital mode is among the best examples of tech-enabled public goods delivery. Digital-mobile-anywhere-anytime banking is becoming the order of the day. The indigenously developed Unified Payments Interface (UPI) and Aadhaar Enabled Payment Service (AePS) have become the backbone of our retail payments system.

6. Alongside these advancements, the Reserve Bank’s regulatory approach has been realigned to support and foster such innovations. The regulatory guidelines for account aggregators and peer-to-peer lending operators are indicative of a proactive regulatory approach. An enabling framework for Regulatory Sandbox has been in place for last three years. The Reserve Bank Innovation Hub (RBIH) has also been set up by the RBI to catalyse innovations in the Fintech sector. We are now moving towards the introduction of a central bank digital currency (CBDC).

Technology as a Disruptor – Opportunities and challenges

7. With the advent of new technologies, we are witnessing a new era of disruption. Given the growing role of technology, data and network effects, there is a feeling among the banks that having an ethos of a technology company, while offering banking services, is the need of the hour. This is an area of opportunity for the banks; but there are associated challenges which need to be mitigated. Greater attention needs to be given to building customers’ trust by (i) offering products and services appropriate and fit for customer’s needs and circumstances; (ii) ensuring robust security controls, reliable and efficient delivery of services, transparency of terms and conditions to customers; and (iii) by handling customer grievances satisfactorily and building necessary awareness among customers. All of these aspects need to be factored in when financial institutions introduce or enhance technology driven products and services.

8. Talking about opportunities, it would be relevant to note that what we have seen until now could be just the tip of the iceberg. The use of artificial intelligence (AI) and machine learning (ML) to determine the creditworthiness of clients for small ticket loans by analyzing data from a wide range of traditional and non-traditional data sources, has the potential to enhance access to credit for marginalized customers. Here also it would be necessary to understand the associated risks and mitigate them suitably through various safeguards and precautions. Risks relating to cyber security, software development, limitations in transaction capacity, privacy of customer data, and data security need to be factored in. The methodology of algorithms underpinning digital financial services has to be clear, transparent, explainable and free from exclusionary biases. The credit scoring models using innovative techniques can be useful but they should be subject to a robust model governance framework. Comprehensive assessment of risks has also to be undertaken while planning to move to cloud with customer sensitive data.

9. In all these digital initiatives, the plan should also factor in those sets of customers who may not be digitally savvy and who may want to engage physically with the bank. It is, therefore, crucial that while driving various tech-enabled initiatives, the existing systems and processes do not see frequent disruptions and non-availability. We have already seen instances of the damage that disruptions in technology systems can bring and the reputation risk they carry for financial entities. A casual approach to handling technology issues even as basic as wrongful deletion of a single system file or inadequate care in patch updating often lead to financial and operational losses.

10. The IT systems and platforms are also exposed to obsolescence and require frequent upgradation. This calls for adequate investment in IT infrastructure by all financial sector entities. This is one of the important focus areas of RBI’s supervision of its regulated entities, especially the Banks and the NBFCs.

11. It has also to be recognised that human resource can turn out to be the weakest link in technology enabled financial services. There is thus a vital need for ongoing training and skill building programmes.

12. At end of the day, the bottomline is how technology improves the financial system in terms of efficiency, effectiveness, resolving bottlenecks in economic functions and provide value addition to the customers.

Collaboration between Finance and Technology Firms

13. Large technology companies (BigTech) which have entered into provision of financial services could potentially be another source of disruption to the financial system. As you would be aware, such companies, whether from e-commerce, social media and search engine platforms, ride hailing and similar businesses have started to offer financial services in a big way on their own or on behalf of others. These companies have an enormous amount of customer data which has helped them to offer tailored financial services to entities and individuals lacking credit history or collateral. Even the banks and other lenders are sometimes utilising platforms provided by fintech companies in their internal processes for credit risk assessment. Such large scale use of new methodologies in credit risk assessment can create systemic concerns like over-leverage, inadequate credit assessment, etc. Authorities and regulators have to strike a fine balance between enabling innovation and preventing systemic risks.

14. The big techs also pose concerns related to competition, data protection, data sharing and operational resilience of critical services in situations where Banks and NBFCs utilise the services of big tech companies. These concerns can also materialise in sectors other than financial services. The provision of financial services through the digital channel, including lending through online platforms and mobile apps, have brought in issues relating to unfair practices, data privacy, documentation, transparency, conduct, breach of licensing conditions, etc. The Reserve Bank will soon issue suitable guidelines and measures to make the digital lending ecosystem safe and sound while enhancing customer protection and encouraging innovation.

What kind of Regulation and Supervision?

15. The need for FinTech regulation emanates from the challenges they pose to the financial system and the new risks they carry. These risks have a bearing on overall financial stability and market integrity.

16. The approach to regulation of FinTech could be by way of Activity Based Regulation wherein similar activities are treated similarly, regardless of the legal status or nature of the entity undertaking the activity. It could also be Entity Based Regulation which requires that regulations are applied to licensed entities or groups that engage in similar and specified activities, such as deposit taking, payment facilitation, lending, and securities underwriting, etc. The approach could also be an Outcome Based Regulation by setting out some basic, common and technology or business model-neutral outcomes that entities must ensure.

17. India has traditionally followed a hybrid form of regulation that combines Activity and Entity Based regulation. As a principle, the RBI has been applying comprehensive regulatory, supervisory and oversight requirements to various segments of financial sector in its domain to create an enabling ecosystem for such activities to grow in an orderly fashion. The underlying theme has always been to maintain financial stability. Going forward, the RBI will continue to finetune its regulatory and supervisory measures keeping in mind the evolving dynamics of the financial sector.

Does Regulation require collaboration with different Regulators?

18. When it comes to technology, it may transcend regulatory or national boundaries. The most relevant example in this case would be the blockchain technology. Different blockchain platforms cannot be limited to a regulator or a nation. Another example can be the case of De-centralised Finance (DeFi) in which financial applications are processed on a blockchain with limited or no involvement of centralised intermediaries. DeFi poses unique challenges to regulators as its anonymity, lack of a centralised governance body, and legal uncertainties can make the traditional approach to regulation ineffective. There is, therefore, a case for a globally coordinated regulatory approach and inter-regulatory co-ordination to enable comprehensive assessment of such activities and mitigation of their risks.

Some recent initiatives of the RBI

19. I would now like to focus on certain supervisory steps taken by the RBI recently to deal with the emerging challenges from fintech. In the specific area of cyber security, the RBI has recently conducted Phishing Simulation exercises for select Supervised Entities (SEs) to assess their email security standards and cyber security preparedness. We have also initiated the process of conducting Cyber Reconnaissance exercises this year. This will provide pre-emptive information on the cybersecurity risk vectors of SEs. Besides, Cyber Drills which are conducted periodically are being further enhanced in terms of coverage and periodicity.

20. The increasing use of technology and digital services has led to more incidents of digital frauds and customer dissatisfaction. The recommendations of the RBI Working Group on digital lending in this area are under examination for issuance of guidelines.

21. In the context of customer service, another area which is engaging the attention of the RBI is the harsh recovery methods used by certain lenders, without having adequate checks and controls over their recovery agents. We have received complaints of customers being contacted by recovery agents at odd hours, even past midnight. There are also complaints of recovery agents using foul language. Such kind of actions by recovery agents are unacceptable and pose reputational risk for the financial entities themselves. We have taken serious note of such instances and will not hesitate to take stringent action in cases where regulated entities are involved. Such complaints against unregulated entities will have to be taken up with appropriate law enforcement agencies.

22. We have recently set up of a Committee for Review of Customer Service Standards in the RBI Regulated Entities (REs) which would inter alia review the emerging and evolving needs of the customer service landscape, especially in the context of evolving digital financial products and their distribution, and suggest measures for strengthening the overall consumer protection framework.

Governance and Risk Management

23. I have often spoken about the importance of good corporate governance in banks and financial institutions. A good governance structure will have to be supported by effective risk management and compliance functions. The cost of compliance to rules and regulations should be perceived as an investment, as inadequacy in this regard can prove to be highly costly. Compliance culture should ensure adherence to not only laws, rules and regulations, but also integrity, ethics and codes of conduct.

24. The Global Financial Crisis was preceded by a wave of financial innovations related to securitisation and other innovative financial instruments. These allowed the financial system to grow at a pace that was beyond its capacity to manage, especially from the point of view of the connected risks. Given such past experience, prudence demands that introduction of innovations in the financial system should be done responsibly and in a calibrated manner, taking into account the capacity of financial entities to manage potential risks. It goes without saying that innovations which provide opportunities through high risk taking need to be managed by sound corporate governance and risk management practices within the financial institutions. The senior management and internal control mechanisms in financial institutions should also ensure that their IT systems are robust and transparent, and not open to manipulation that may camouflage the true state of affairs in the organisation.

Conclusion

25. Let me conclude by saying that we are in the midst of a technological revolution in the sphere of financial services. Technology and Innovation per se are neither destructive nor constructive. It is the use cases that present the responsible or irresponsible sides of any particular innovation or technology. Reserve Bank shall continue with its approach where innovations which provide benefits to society are encouraged without compromising the stability of the financial system.

26. The trend of technology driven changes in the financial services sector will continue in the future. Participants and players in this sector will have to strive hard to remain relevant in the ever changing economic environment by continuously improving the quality of their governance; reworking their business strategies and business models; designing products and services with the customer in mind; ensuring operational resilience and risk management; and focussing on more efficient products and services by leveraging on technology. The possibilities are immense only if we are ready to embrace them while meeting the challenges!

The Chairman / Managing Director / Chief Executive Officer All Scheduled Commercial Banks, including Regional Rural Banks / Urban Co-operative Banks / State Co-operative Banks / District Central Co-operative Banks / Payments Banks / Small Finance Banks / Local Area Banks / Non-bank Prepaid Payment Instrument Issuers / Authorised Card Payment Networks / National Payments Corporation of India

Madam / Dear Sir,

Processing of e-mandates for recurring transactions

A reference is invited to our circulars DPSS.CO.PD.No.447/02.14.003/2019-20 dated August 21, 2019, DPSS.CO.PD No.1324/02.23.001/2019-20 dated January 10, 2020, DPSS.CO.PD No.754/02.14.003/2020-21 dated December 04, 2020 and CO.DPSS.POLC.No.S34/02-14-003/2020-2021 dated March 31, 2021 (collectively referred to as “e-mandate framework”). The e-mandate framework prescribed an Additional Factor of Authentication (AFA), inter alia, while processing the first transaction in case of e-mandates / standing instructions on cards, prepaid payment instruments and Unified Payments Interface. For subsequent transactions with transaction values up to ₹5,000/- (AFA limit), prescription of AFA was waived.

2. On a review of implementation of the e-mandate framework and the protection available to customers, it has been decided to increase the aforesaid AFA limit from ₹5,000/- to ₹15,000/- per transaction.

3. This circular is issued under Section 10 (2) read with Section 18 of the Payment and Settlement Systems Act, 2007 (Act 51 of 2007), and shall come into effect immediately.

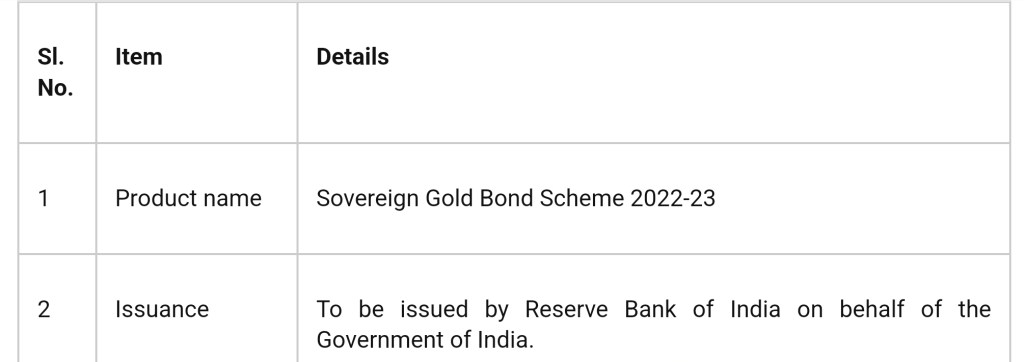

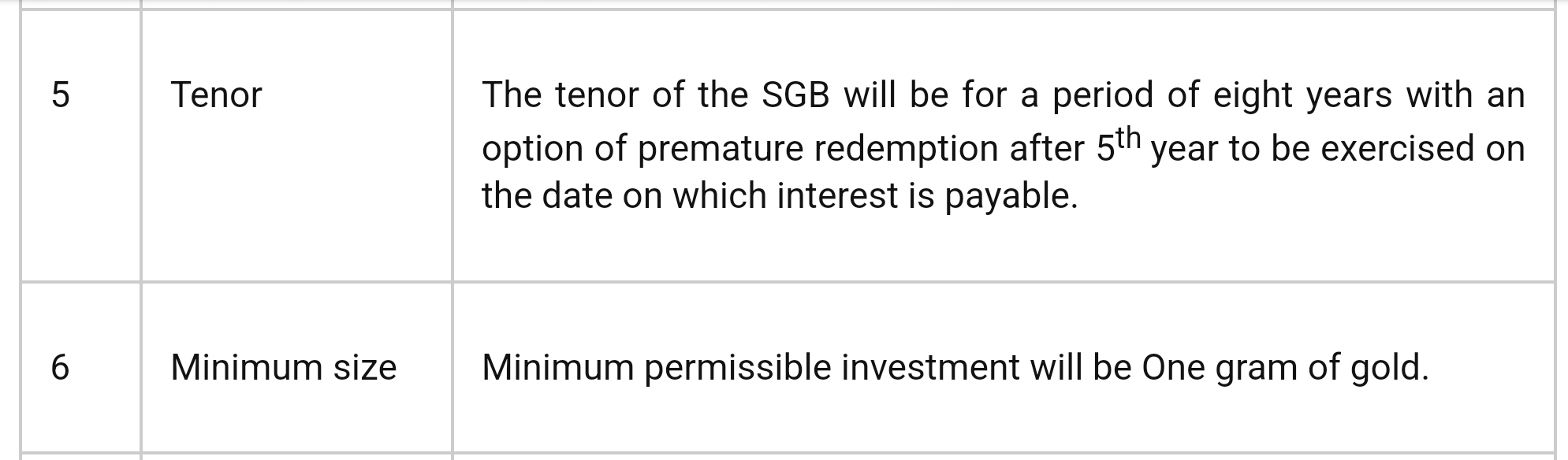

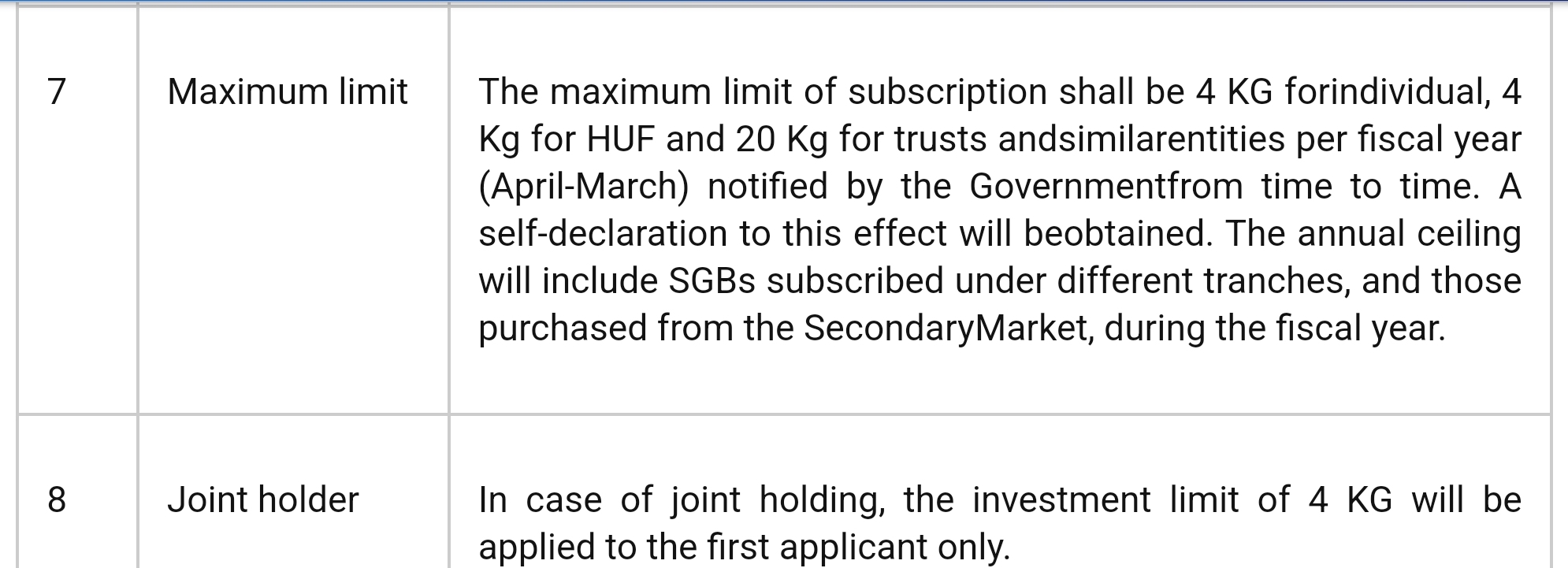

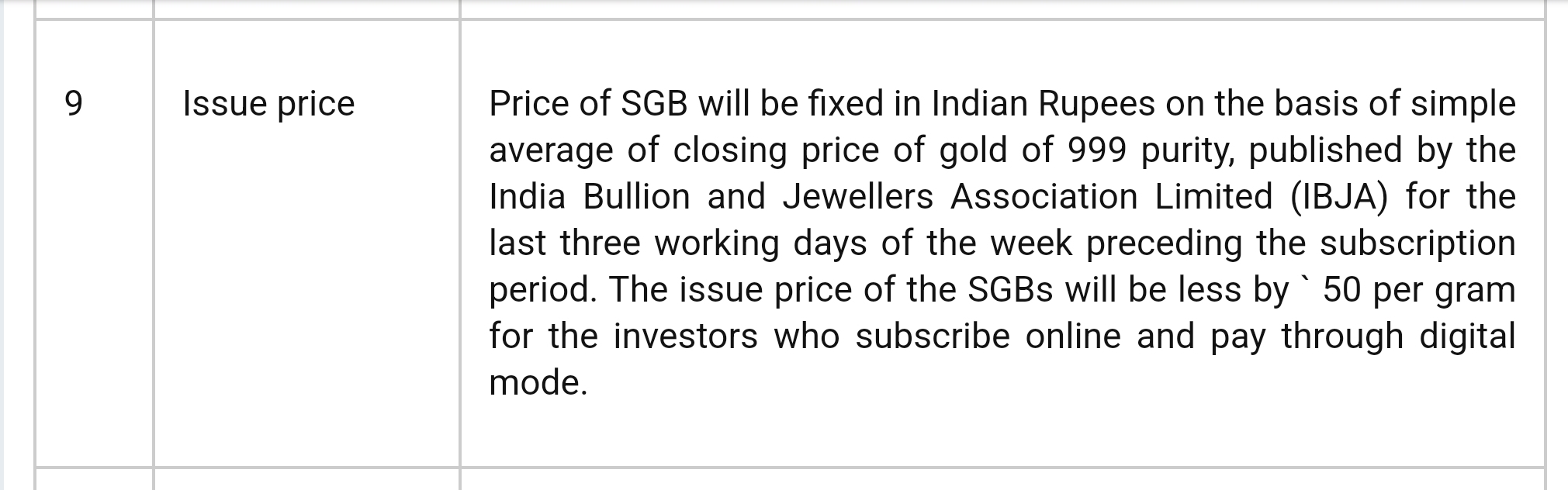

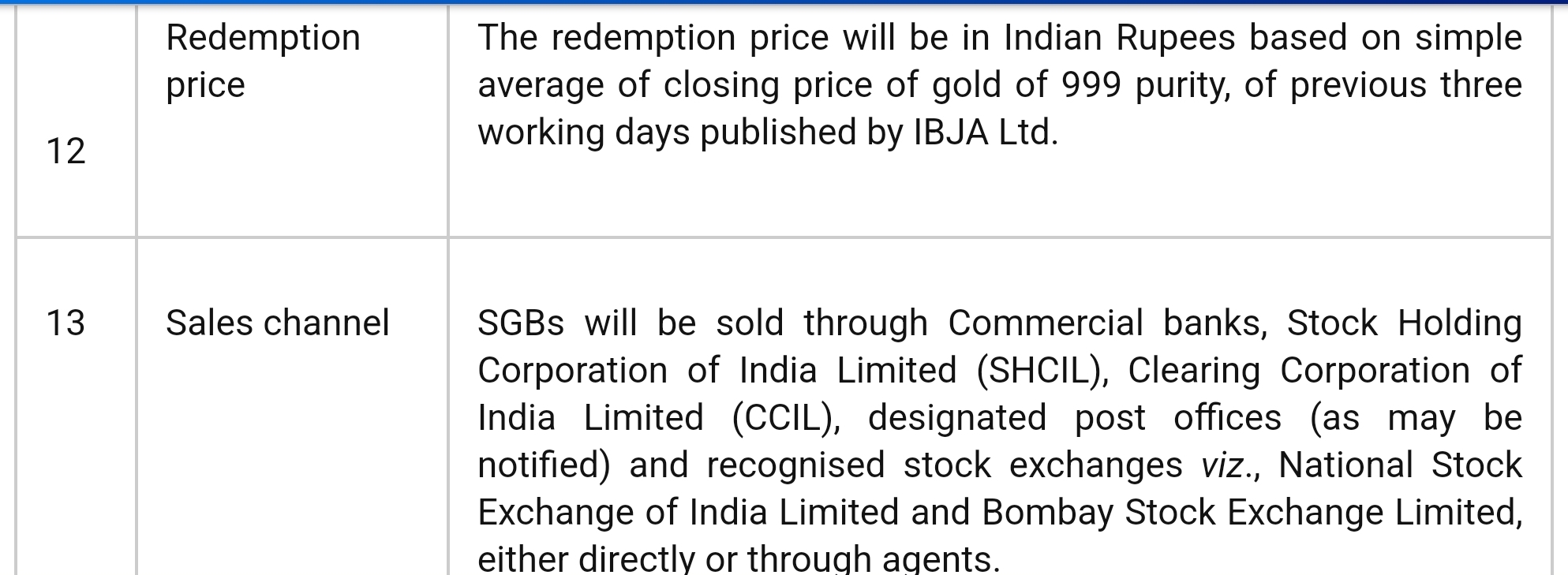

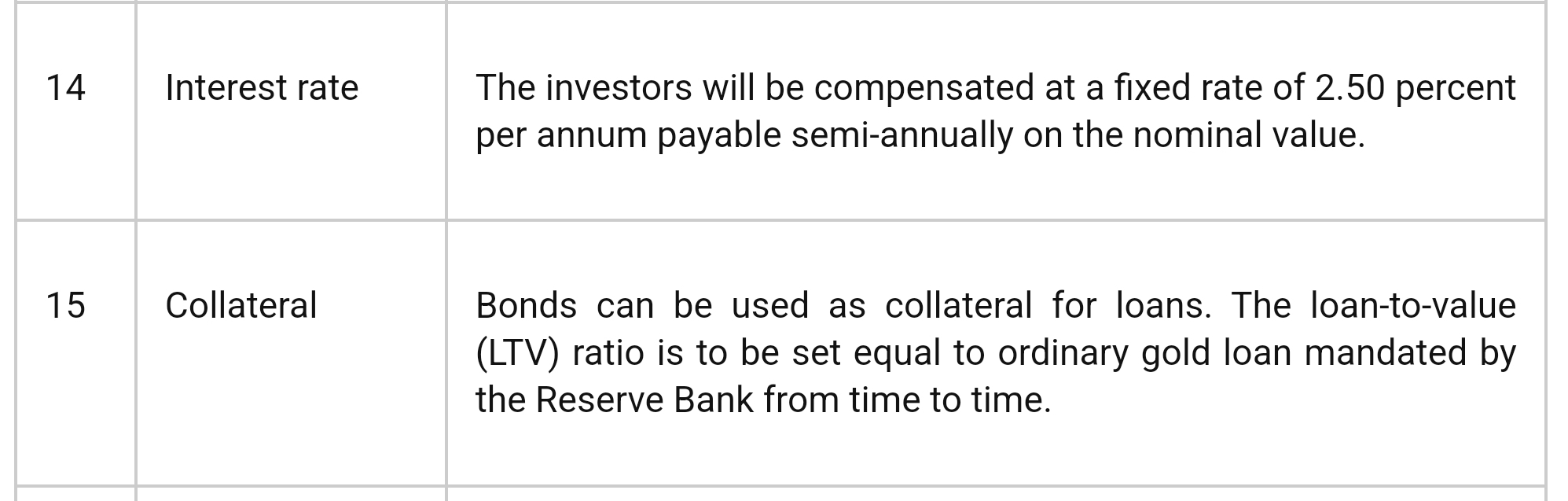

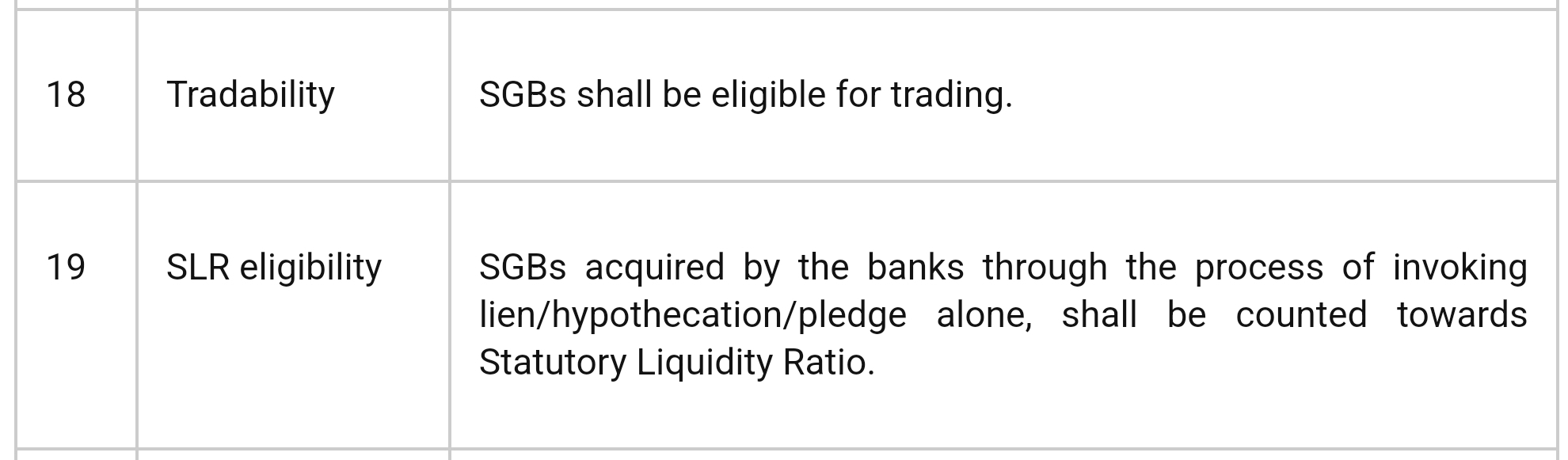

The Government of India, in consultation with the Reserve Bank of India, has decided to issue Sovereign Gold Bonds in tranches as per the calendar specified below:

The Sovereign Gold Bonds (SGBs) will be sold through Scheduled Commercial banks(except Small Finance Banks and Payment Banks), Stock Holding Corporation of India Limited (SHCIL),Clearing Corporation of India Limited (CCIL), designated post offices, and recognised stock exchanges viz., National Stock Exchange of India Limited and Bombay Stock Exchange Limited.The features of the Bond are as under:

Revised Instruction for constitution and functioning of Local Committees to deal with taxpayers’ grievances due to high-pitched Scrutiny Assessment.

In line with CBDT’s policy and commitment towards providing enhanced taxpayers’ services and reduce taxpayers’ grievances, CBDT has issued revised Instruction for constitution and functioning of Local Committees to deal with taxpayers’ grievances arising out of high-pitched Scrutiny Assessment through F.No.225/101/2021-ITA-II, dated 23rd April, 2022.

This instruction also provides for initiation of suitable administrative action against the officer concerned, in cases where assessments are found by the Local Committee to be high-pitched or where there is non-observance of principles of natural justice, non-application of mind or gross negligence of Assessing Officer/ Assessment Unit.

The Insolvency and Bankruptcy Board of India (IBBI/Board) notified the Insolvency and Bankruptcy Board of India (Insolvency Resolution Process for Corporate Persons) (Second Amendment) Regulations, 2016 (CIRP Regulations) on 14th June, 2022.

The amendment provides the operational creditors to furnish extracts of Form GSTR-1, Form GSTR-3B and e-way bills, wherever applicable along with the application filed under section 9 of the Insolvency and bankruptcy Code, 2016. These additional set of documents, can be used as evidence of transaction with the corporate debtor, debt and default easing the process of admission. These documents will also to be submitted as part of the claims submitted to the resolution professional to help collation of claims. Further, creditors filing applications under section 7 or 9 of the Code are required to furnish details of their PAN and Email ID to ensure smooth correspondence.

In order to improve information availability, the amendment places a duty on corporate debtor, its promoters or any other person associated with the management of the corporate debtor to provide the information in such format and time as sought by the resolution professional.

The amendment places a duty on the creditors to share information regarding the assets and liabilities of the corporate debtor, the financial statements and other relevant financial information from their records and available reports to help the resolution professional in preparation of the information memorandum and relevant extracts from the transaction or forensic audit reports to aid the resolution professional in preparation of the avoidance application.

The Amendment also addresses the issue of treatment of avoidance applications filed with the Adjudicating Authority after closure of the corporate insolvency resolution process (CIRP). It provides that the resolution plan shall provide for manner in which such applications will be pursued after the approval of the resolution plan and the manner in which the proceeds, if any, from such proceedings shall be distributed.

The amendment includes a definition of significant difference in valuations during CIRP and enables the committee of creditors to make a request to the resolution professional regarding the appointment of a third valuer.

The amended regulations are effective from today. These are available at www.ibbi.gov.in.

With a view to put in place, a streamlined and swift complaint handling procedure, the Insolvency and Bankruptcy Board of India notified the Insolvency and Bankruptcy Board of India (Grievance and Complaint Handling Procedure) (Amendment) Regulations, 2022 and the Insolvency and Bankruptcy Board of India (Inspection and Investigation) (Amendment) Regulations, 2022 to amend the Insolvency and Bankruptcy Board of India (Grievance and Complaint Handling Procedure) Regulations, 2017 and the Insolvency and Bankruptcy Board of India (Inspection and Investigation) Regulations, 2017.

The Insolvency and Bankruptcy Code, 2016 (Code) read with Insolvency and Bankruptcy Board of India (Grievance and Complaint Handling Procedure) Regulations, 2017 provide mechanism for redressal of complaints and grievances filed against insolvency professionals, insolvency professional agencies and information utilities. Further the Code read with Insolvency and Bankruptcy Board of India (Inspection and Investigation) Regulations, 2017 provide mechanism for carrying out inspections and investigations on insolvency professional agencies, insolvency professionals and information utilities and passing orders by Disciplinary Committee.

The mechanism of complaint/ grievance redressal and subsequent enforcement action has been amended to have expeditious redressal and also to avoid placing undue burden on the service providers. To curtail such delays and to ensure expeditious and result oriented enforcement mechanism, the Amendment Regulations provides for following:

Revisions in various timelines related to enforcement process provided in the (Grievance and Complaint Handling Procedure) Regulations, 2017 and (Inspection and Investigation) Regulations, 2017 for addressing the issue of delay in present mechanism.

Effective participation of IPAs in regulating the IPs through examination of grievances received against IPs.

Intimation to Committee of Creditor (CoC)/ Adjudicating Authority (AA) about the outcome of Disciplinary Committee (DC) order.

The Amendment Regulations are effective from 14th June, 2022. These are available at www.ibbi.gov.in.