It may be noted that 6% tax rate has been added in the item details section of all the tables of form GSTR-1, except HSN table 12. In case your outward supplies attracts 6% tax rate, you are required to upload the details against 6% tax rate in the item details section.

Shri Kiren Rijiju recommends young talent to apply for Internship Programme introduced for Law students

Department of Legal Affairs introduces opportunity for internship for law students, under it’s offices in Delhi Mumbai, Bengaluru, Kolkata and Chennai

Internship programme aims to acquaint young law students with workings of the Department of Legal Affairs by training them in various related fields

Selected interns to be given a token remuneration

On the 1st of June, 2022, the Department of Legal Affairs has opened its forms for the Internship Programme for Law students at the behest of the Minister of Law & Justice, Shri Kiren Rijiju, under the capable guidance of the Minister of State, Prof. S.P. Singh Baghel, the Law Secretary, Dr. Niten Chandra and, the Additional Secretary in the Department of Legal Affairs, Dr. Anju Rathi Rana. The intended purpose of the said Internship Programme is to acquaint young law students with the workings of the Department of Legal Affairs by training them in research and referencing work, tendering legal advice in various specialized fields of law such as constitutional and administrative law, finance law, infrastructure law, economic law, labour law, conveyancing, arbitration and contract law, etc.

Shri Kiren Rijiju, Minister of Law & Justice, has recommended the young talent of the country to apply for this internship programme.

Shri Kiren Rijiju tweeted:

“A great opportunity to work at the Department of Legal Affairs, as it introduces #internships for law students for offices in Delhi, Mumbai, Bengaluru, Kolkata and Chennai.

A great opportunity to work at the Department of Legal Affairs, as it introduces #internships for law students for offices in Delhi, Mumbai, Bengaluru, Kolkata and Chennai. I recommend young talent to apply for this internship at https://t.co/Gy4AQBUOwmpic.twitter.com/PuUOFpK8iK— Kiren Rijiju (@KirenRijiju) June 1, 2022

The eligibility criteria for this Internship Programme includes that the applicants must be Indian students who are pursuing their studies in the 2nd and 3rd year of the three-year degree course, and in their 3rd to 5th year of the five-year degree course, or students who have completed their LLB course from any recognized college/law school/university. The duration of this internship will ordinarily remain for a period of one month, which shall commence from the first working day of every month unless specified otherwise. The monthly internships shall tentatively start from June, 2022 until May, 2023.

In a given month, the maximum number of interns to be allowed will be 10-30. The students willing to undergo the Internship Programme under the Department of Legal Affairs may fill their application along with the relevant documents/ an NOC from their respective college/law school/university. The application form can be accessed on the website https://legalaffairs.gov.in/internship. All applicants are advised to fill the form online and upload all the documents prior to the last date, as mentioned on the website.

The selection of the interns for the Programme will be made on a first come, first served basis, subject to the availability of slots and approval of the competent authority. All further intimations regarding the same will be sent to the applicants via SMS and emails. The selected interns will be attached with an officer of appropriate level in the Department of Legal Affairs in the cities of New Delhi, Mumbai, Chennai, Bengaluru and Kolkata.

At the end of the Internship Programme, all interns will be required to submit a report on the work undertaken by them in the Department of Legal Affairs and upon a satisfactory completion of the internship, a Certificate of Internship shall be awarded, along with an honorarium of Rs. 5000/-. For a satisfactory completion of the internship, inter-alia 90% attendance is mandatory. The said Internship is a full-time internship, to be attended physically, where the interns are expected not to pursue any other course/work during the tenure of the internship.

All further information and clarifications can be attained by contacting the Section Officer, Admin.I (LA) admn1-la@nic.in (011-23387914)

As a significant step towards the Digital India vision of the Government, Government e-Marketplace (GeM) has developed an IT module for Ministry of Defence, for integration of competent financial authorities and Internal Financial Advisers (IFA) for online e-concurrence and approval of procurement proposals on GeM portal. The integration module was launched by Shri. Rajnish Kumar, Controller General of Defence Accounts (CGDA), in the presence of Shri Prashant Kumar Singh, Chief Executive Officer of Government e-Marketplace (GeM) at Defence Accounts Department Headquarters in New Delhi on June 01, 2022.

The module has been developed by GeM over the course of last one year, utilising Business Process Re-engineering (BPR)-based procedural inputs provided by the Ministry of Defence, Defence Accounts Department Headquarters and the Headquarters of the various defence services and other MoD organisations.

Procurement by Ministry of Defence (MoD) through Government e-Market (GeM) portal had reached an all-time high of Rs 15,047.98 crore for the Financial Year 2021-22, which is more than 250 percent over the last financial year.

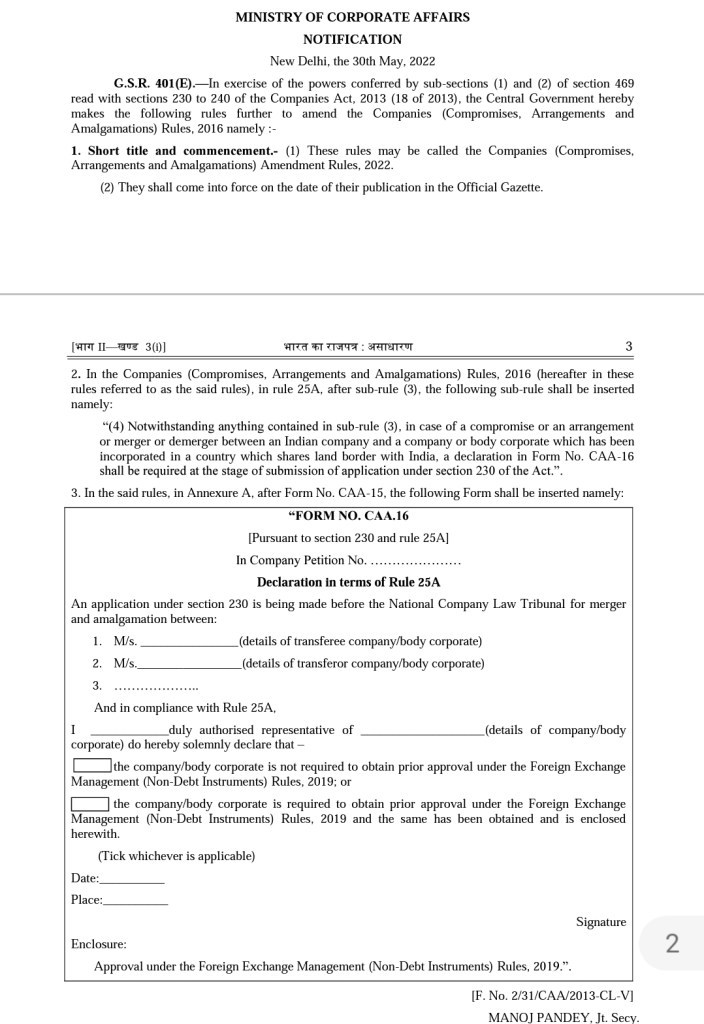

MCA has notified amendment in Companies (Compromises, Arrangements and Amalgamations) Rules, 2016, which requires in case of a compromise or an arrangement or merger or demerger between an Indian company and a company or body corporate which has been incorporated in a country which shares land border with India, a declaration in Form No. CAA-16 shall be required at the stage of submission of application under section 230 of the Companies Act, 2013.

The Union Cabinet, chaired by the Prime Minister Shri Narendra Modi has given its approval for expanding the mandate of GeM to allow procurement by Cooperatives as buyers on GeM.

The Government e Marketplace (GeM) was launched on August 9, 2016 by the Ministry of Commerce and Industry, Government of India to create an open and transparent procurement platform for Government buyers. A Special Purpose Vehicle (SPV) by the name of Government e- Marketplace (GeM SPV) was set up as the National Public Procurement Portal on 17th May, 2017 in pursuance of the approval, of the Union Cabinet accorded on 12th April, 2017. At present, the platform is open for procurement by all government buyers: central and state ministries, departments, public sector enterprises, autonomous institutions, local bodies, etc. As per existing mandate, GeM is not available for use by private sector buyers. Suppliers (sellers) can be from across all segments: government or private.

No. of beneficiaries:

More than 8.54 lakh registered cooperatives and their 27 Crore members would be benefitted with this initiative. GeM portal is open for all the buyers and sellers across the country.

Details:

1. GeM is already adequately developed as a one stop portal to facilitate online procurement of common use Goods and Services. It is transparent, efficient, has economy of scale and is speedy in procurement. Cooperative Societies will now be allowed to procure goods and services from GeM.

2. Allowing Cooperative Societies to register on GeM as Buyers would help Cooperatives in getting competitive prices through an. open and, transparent process,

3. The validated list of cooperatives to be onboarded on GeM – for pilot as well as subsequent scale up – will be decided by Ministry of Cooperation in consultation with GeM SPV. This will ensure that technical capacity and logistics requirement of the GeM system are taken into account while deciding the pace of on boarding of Cooperative as buyers on GeM.

4. GeM will provide a dedicated onboarding process for cooperatives, provide the technical infrastructure to support additional users on existing portal, as well as provide assistance to cooperatives for onboarding and transaction journeys, via available contact centers, in-field training and other support services.

5. Ministry of Cooperation would issue necessary advisories to encourage the Cooperative Societies to make use of the GeM platform for procurement of goods and services in order to benefit from increased transparency, efficiency and competitive prices.

6. To protect interests of the broader seller community on GeM and ensure timely payments, the modalities of payment systems shall be decided by GeM in consultation with the Ministry of Cooperation.

Implementation strategy and targets:

GeM will initiate suitable actions, which would inter alia include creation of necessary features and functionalities on GeM portal, upgradation of infrastructure, strengthening of the helpdesk and training ecosystem, and onboarding of cooperatives. The overall pace and mechanism of roll-out would be decided by Ministry of Cooperation. The milestones and target dates will be aligned mutually between Ministry of Cooperation and GeM (Ministry of Commerce and Industry).

Impact including employment generation potential:

The Ministry of Cooperation wanted the Cooperative Societies to be allowed to procure goods and services from GeM as it is already adequately developed as a one stop portal to facilitate online procurement of common use Goods and Services. It is transparent, efficient, has economy of scale and is speedy in procurement. In the above context, allowing Cooperative Societies to register on GeM as Buyers of Goods & Services required by them would help Cooperatives in getting competitive prices through an open and transparent process. Moreover, since the societies have more than 27 Crore members, procurement through GeM would not only economically benefit the common man, but it would also enhance the credibility of the cooperatives.

GeM has also developed a rich understanding of running an advanced procurement portal including the functional needs, managing the technical infrastructure, and dealing with multiple stakeholders involved. It is felt that the rich experience gained in creating the procurement ecosystem in the country can be significantly utilized to produce efficiencies and transparency in procurement processes for cooperatives also. This is also expected to enhance overall “Ease of Doing Business” for cooperatives, while providing a larger Buyer base to the GeM registered sellers also.

Expenditure involved:

While the GeM SPV will continue to leverage the existing platform and organization for supporting the proposed expanded mandate, it may need some investments in additional technology infrastructure, and additional training and support resources. To cover for these incremental costs, GeM may charge an appropriate transaction fee from cooperatives, to be decided in mutual consultation with the Ministry of Cooperation. Such charges shall not be more than the charges which GeM would charge to other Government buyers. This will be planned to ensure self-sustainability of operations for GeM, and hence no major financial implication is expected for government.

Background:

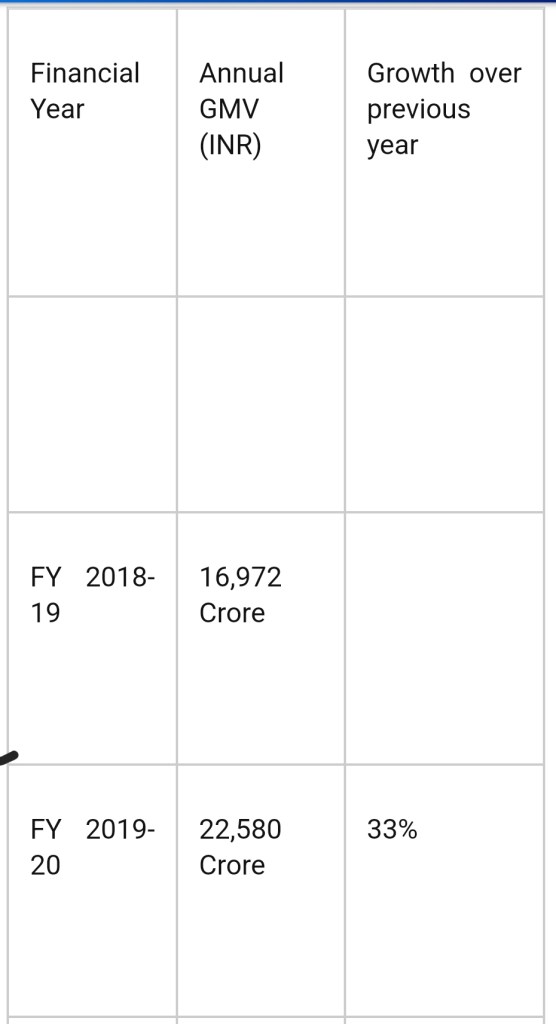

The GeM SPV has made significant strides since its inception. The Gross Merchandise Value (GMV) has grown with CAGR of over 84.5% from FY 2018-19 to FY 2021-22. The portal has delivered 178% growth in GMV in the FY 2021-22 and has crossed INR 1 lakh Crore in FY 2021-22 alone, which is higher than the cumulative GMV till FY 2020-21.

Each of the three pillars of GeM viz inclusion, transparency and efficiency have seen significant progress. The contribution by MSMEs to the cumulative transaction value is about 58%. Different independent studies, including those by the World Bank and National Economic Survey 2021, indicated substantial savings due to GeM’s ability to pool in more participation and provide cost effective options.

The cooperative movement in India has grown significantly, playing an important role in addressing the developmental needs of underprivileged classes in India, especially in agricultural, banking and housing sectors. There are currently 8.54 lakh registered cooperatives. These cooperatives collectively procure and sell in large quantities. Presently, the registration of cooperatives as “buyers” was not covered within the existing mandate of GeM.

Any complaint regarding malpractices in FCRA & MU wings of Foreigners Division, MHA may be sent to email fcra-complaints[at]mha[dot]gov[dot]in. This email will be accessed exclusively by Joint Secretary.

A complaint box has been placed near MHA reception in Major Dhyan Chand National Stadium (MDCNS), Near India Gate, New Delhi. Any person desirous of raising complaint of malpractice related to FCRA may drop a complaint in the box.

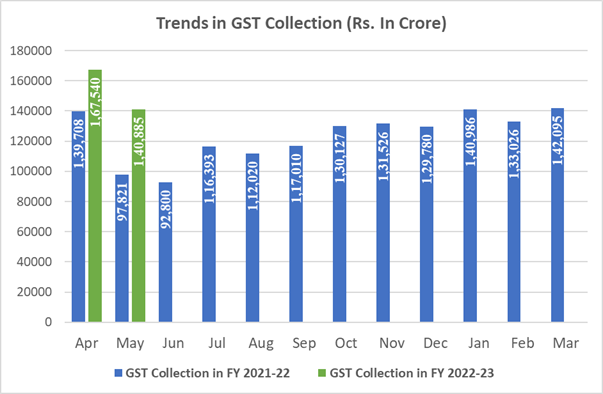

₹1,40,885 crore gross GST Revenue collection for May 2022; increase of 44% year-on-year

GST collection crosses ₹1.40 lakh crore mark 4th time since inception of GST; 3rd month at a stretch since March 2022

The gross GST revenue collected in the month of May 2022 is ₹1,40,885crore of which CGST is ₹25,036 crore, SGST is ₹32,001 crore, IGST is ₹73,345 crore (including ₹ 37469 crore collected on import of goods) and cess is ₹10,502 crore (including ₹931 crore collected on import of goods).

The government has settled ₹27,924 crore to CGST and ₹23,123 crore to SGST from IGST. The total revenue of Centre and the States in the month of May 2022 after regular settlement is ₹52,960 crore for CGST and ₹55,124 crore for the SGST. In addition, Centre has also released GST compensation of ₹86912 crores to States and UTs on 31.05.2022.

The revenues for the month of May 2022 are 44% higher than the GST revenues in the same month last year of ₹97,821 crore. During the month, revenues from import of goods was 43% higher and the revenues from domestic transaction (including import of services) are 44% higher than the revenues from these sources during the same month last year.

This is only the fourth time the monthly GST collection crossed ₹1.40 lakh crore mark since inception of GST and third month at a stretch since March 2022. The collection in the month of May, which pertains to the returns for April, the first month of the financial year, has always been lesser than that in April, which pertains to the returns for March, the closing of the financial year. However, it is encouraging to see that even in the month of May 2022, the gross GST revenues have crossed the ₹1.40 lakh crore mark. Total number of e-way bills generated in the month of April 2022 was 7.4 crore, which is 4% lesser than 7.7 crore e-way bills generated in the month of March 2022.

The chart below shows trends in monthly gross GST revenues during the current year. The table shows the state-wise figures of GST collected in each State during the month of May 2022 as compared to May 2021.

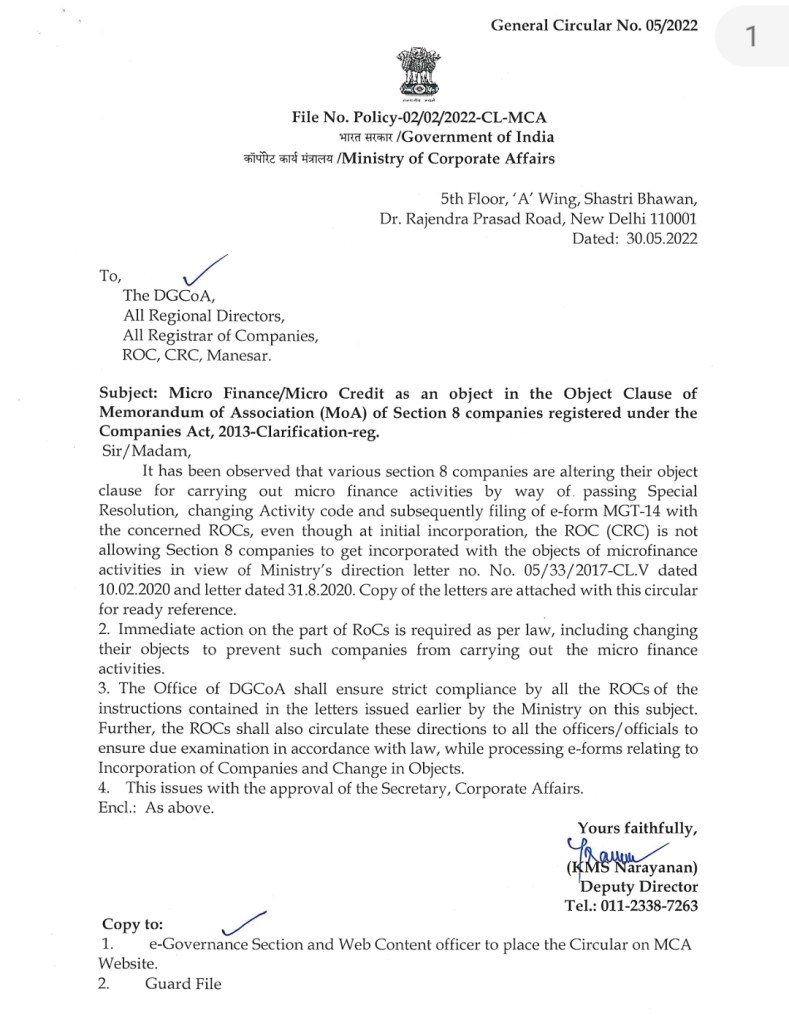

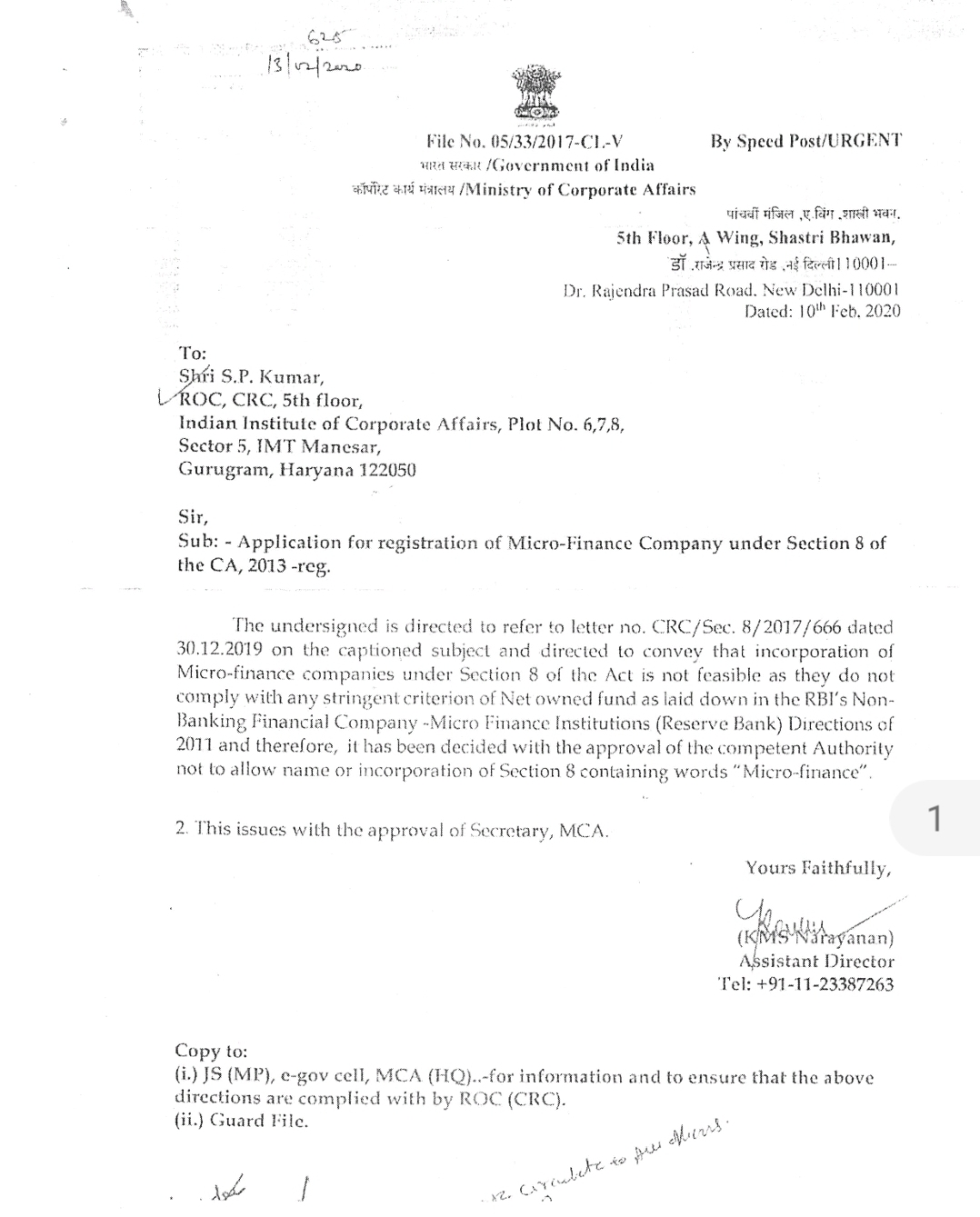

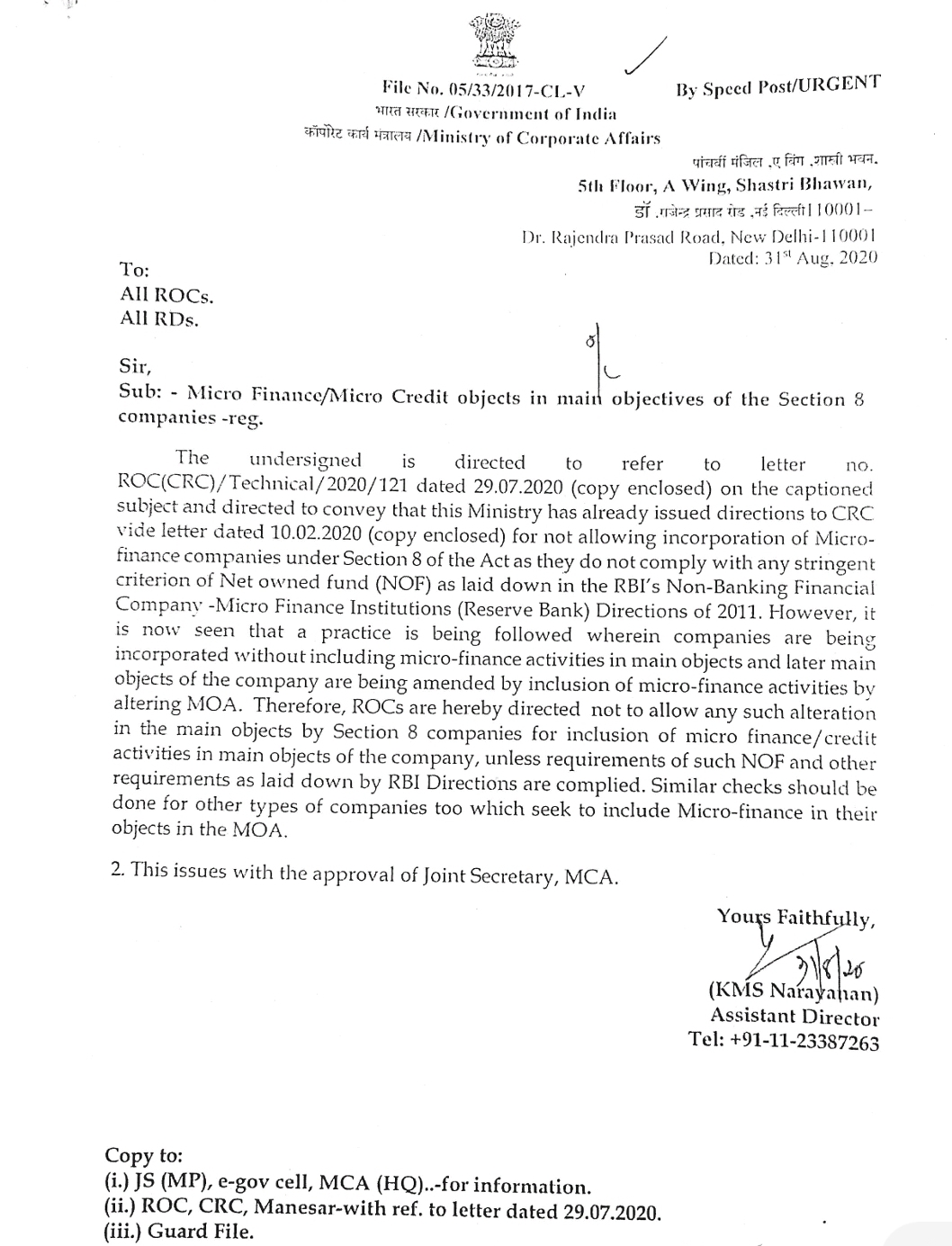

MCA issued General Circular on 30 May 2022 giving Clarification on Micro Finance/Micro Credit as an Object in the Object Clause of MOA of Section 8 companies registered under the CA 2013 :

During the course of search, inspection or investigation, sometimes the taxpayers opt for deposit of their partial or full GST liability arising out of the issue pointed out by the department during the course of such search, inspection or investigation by furnishing DRC-03. Instances have been noticed where some of the taxpayers after voluntarily depositing GST liability through DRC-03 have alleged use of force and coercion by the officers for making ‘recovery’ during the course of search or inspection or investigation. Some of the taxpayers have also approached Hon’ble High Courts in this regard.

The matter has been examined. Board has felt the necessity to clarify the legal position of voluntary payment of taxes for ensuring correct application of law and to protect the interest of the taxpayers. It is observed that under CGST Act, 2017 a taxpayer has an option to deposit the tax voluntarily by way of submitting DRC-03 on GST portal. Such voluntary payments are initiated only by the taxpayer by logging into the GST portal using its login id and password. Voluntary payment of tax before issuance of show cause notice is permissible in terms of provisions of Section 73(5) and Section 74 (5) of the CGST Act, 2017. This helps the taxpayers in discharging their admitted liability, self-ascertained or as ascertained by the tax officer, without having to bear the burden of interest under Section 50 of CGST Act, 2017 for delayed payment of tax and may also save him from higher penalty imposable on him subsequent to issuance of show cause notice under Section 73 or Section 74, as the case may be.

It is further observed that recovery of taxes not paid or short paid, can be made under the provisions of Section 79 of CGST Act, 2017 only after following due legal process of issuance of notice and subsequent confirmation of demand by issuance of adjudication order. No recovery can be made unless the amount becomes payable in pursuance of an order passed by the adjudicating authority or otherwise becomes payable under the provisions of CGST Act and rules made therein. Therefore, there may not arise any situation where “recovery” of the tax dues has to be made by the tax officer from the taxpayer during the course of search, inspection or investigation, on account of any issue detected during such proceedings. However, the law does not bar the taxpayer from voluntarily making payment of any tax liability ascertained by him or the tax officer in respect of such issues, either during the course of such proceedings or subsequently.

Therefore, it is clarified that there may not be any circumstance necessitating `recovery’ of tax dues during the course of search or inspection or investigation proceedings. However, there is also no bar on the taxpayers for voluntarily making the payments on the basis of ascertainment of their liability on non-payment/ short payment of taxes before or at any stage of such proceedings. The tax officer should however, inform the taxpayers regarding the provisions of voluntary tax payments through DRC-03.

Pr. Chief Commissioners/ Chief Commissioners, CGST Zones and Pr. Director General, DGGI are advised that in case, any complaint is received from a taxpayer regarding use of force or coercion by any of their officers for getting the amount deposited during search or inspection or investigation, the same may be enquired at the earliest and in case of any wrongdoing on the part of any tax officer, strict disciplinary action as per law may be taken against the defaulting officers.

EXCISE & TAXATION DEPARTMENT, HARYANA Memo No – 367/GST- 2 dated 24 May 2022

It has come to the notice of the Head Office that few Proper Officers in the State are insisting on personal appearances or seeking extraneous information from the applicants seeking fresh registration under GST. The matter has been examined.

While there is an urgent need of weeding out bogus / fake firms set up for passing of fake input tax credit, there is also a need of facilitating bonafide taxpayers for GST registrations. The following instructions may please be noted:-

a) All applicants for registration are to be processed in accordance with provisions laid down in Section 25 and Rules framed there under.

b) The Act does not mandate physical appearance / personal statements of the applicants at the time of processing of registration. This practice shall be discouraged. However, in case of doubt/suspicion, physical verification of the business premises may be conducted under Rule 25 of the HGST Rules, 2017.

c) The list of documents to be uploaded with the application for registration are already provided in FORM GST REG-01. Ideally, no extraneous information/documents shall be sought by the Proper Officer while processing such applications. However, in case of doubt/suspicion, the proper officer may call for information as he may deem fit but information shall be relevant to the application and frivolous / extraneous information shall not be called for.

Difficulty, if any, in implementation of these instructions may be brought to the notice of the Department.

This issues with the approval of Excise and Taxation Commissioner. (Digitally signed. No signature required.) Addl. Excise and Taxation Commissioner (GST) Haryana, Panchkula