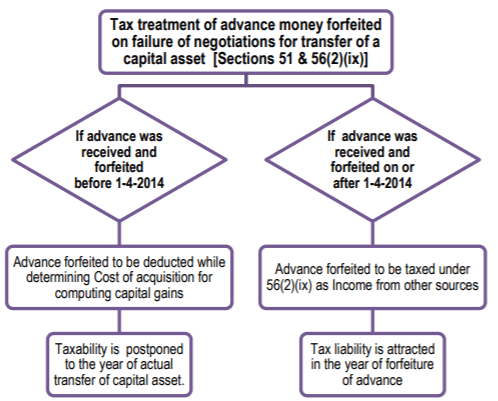

As per section 51 of Income tax Act,1961,Where any capital asset was on any previous occasion the subject of negotiations for its transfer, any advance or other money received and retained by the assessee in respect of such negotiations shall be deducted from the cost for which the asset was acquired or the written down value or the fair market value, as the case may be, in computing the cost of acquisition.

Proviso of Section 51 says that where any sum of money, received as an advance or otherwise in the course of negotiations for transfer of a capital asset, has been included in the total income of the assessee for any previous year in accordance with the provisions of clause (ix) of sub-section (2) of section 56, then, such sum shall not be deducted from the cost for which the asset was acquired or the written down value or the fair market value, as the case may be, in computing the cost of acquisition.

As per section 56(2)(ix) any sum of money received as an advance or otherwise in the course of negotiations for transfer of a capital asset, if,— (a) such sum is forfeited; and (b) the negotiations do not result in transfer of such capital asset shall be chargeable to income-tax under the head “Income from other sources”.

As per interpretation of section 51 & 56(2)(ix) , tax treatment of Advance money/earnest money forfeited as under :

Refer PPT & YouTube link on Tax treatment of Advance money/earnest money forfeited

Thank You !

Bipul Kumar

Business Consultant

RSBK Business Services Private Limited

(A team of CA,CS & Lawyers)

Website: https://businesssosimple.com

Email: rsbkeducationalservices@gmail.com

Contact us: +91-6541-296060, 9304027546 Whatsup no. -9122050937