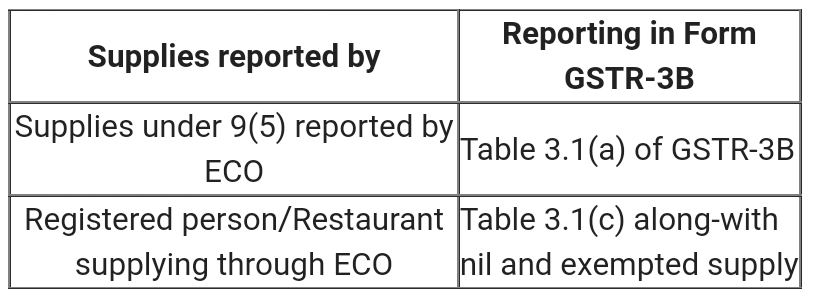

- As per the GST Council decision to notify “Restaurant Service” under section 9(5) of the CGST Act, 2017 along with other services notified earlier such as motor cabs, accommodation and housekeeping services wherein the tax on such supplies would be paid by electronic commerce operator if such supplies made through it, Notification No. 17/2021-Central Tax (Rate) and 17/2021-Integrated Tax (Rate) dated 18.11.2021 have been issued. Accordingly, the tax on supplies of restaurant service supplied through e-commerce operators, shall be paid by the e-commerce operator with effect from the 1st January, 2022.

- In light of the above, E-commerce operator and registered person would report taxable supplies notified under section 9(5) of CGST Act, 2017 and similar provisions in IGST/SGST/UTGST Act in the following manner.

- 3. For more details, please refer to CBIC Circular No. 167/23/2021 dated 17.12.2021.

Thanking you,

Team GSTN