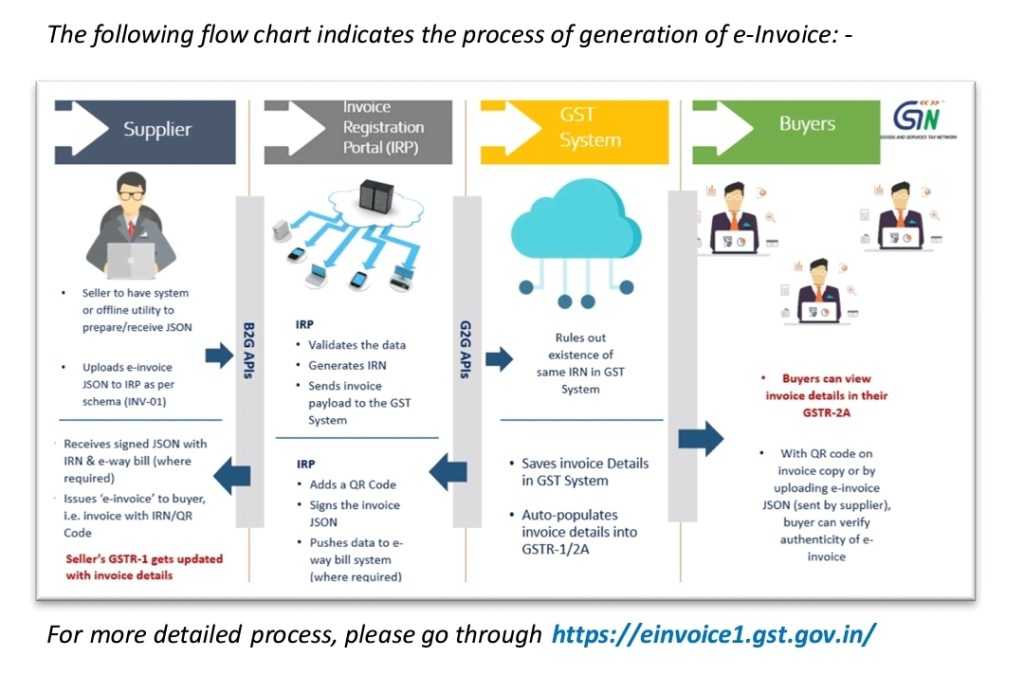

Flowchart :

What is ‘e-invoicing’?

As per Rule 48(4) of CGST Rules, notified class of registered persons shall prepare an invoice by incorporating the Invoice Reference Number (IRN) and the QR-Code generated by uploading specified particulars in FORM: GST INV-01 on Invoice Registration Portal (IRP).

Such invoice containing, inter alia, the QR Code embedded with IRN (mentioning IRN separately, is optional), issued by the notified supplier to buyer is commonly referred to as ‘e-invoice’ in GST.

Please note that ‘e-invoice’ doesn’t mean generation of invoice on a Government portal or issue of invoice in pdf form.

How is ‘e -invoicing’ different from present system (normal invoice)?

There is no much difference between the e-invoice and a normal invoice. In the e-invoice system, the notified registered persons will continue to create their GST invoices on their own Accounting/Billing/ERP Systems, but it shall bear the QR Code embedded with IRN (mentioning IRN separately, is optional), pre-generated on IRP. In other words, the specified contents of the invoices will have to be first posted in FORM: GST INV-01 on IRP, to generate the said unique IRN with a QR Code. e-Invoice is nothing but an invoice issued to the receiver of goods/services by the supplier along with the QR Code .

A GST invoice issued by the notified supplier will be valid only with a valid IRN/QR-code.

For which businesses, e-invoicing is mandatory?

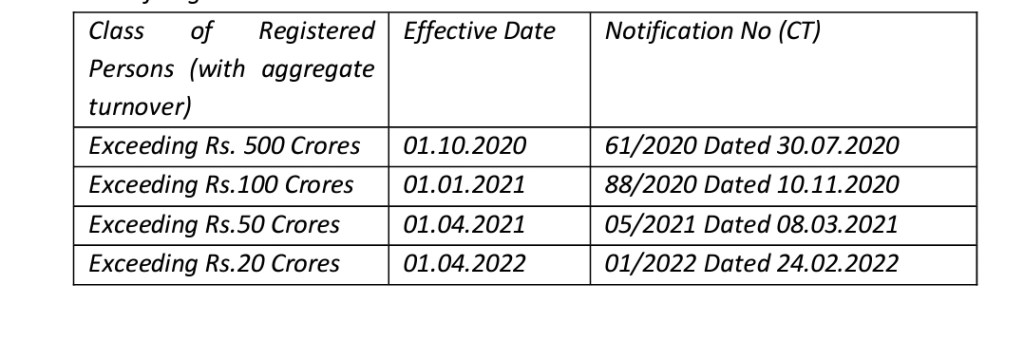

e-invoicing is mandatory for the class of Registered Persons whose aggregate turnover (based on PAN) is more than the prescribed limit (as per relevant notification) in any preceding financial year from 2017-18 onwards. of The effective date from which the e-Invoice was notified as mandatory for different class of Registered Persons is indicated hereunder:

What are the advantages of e-invoice for businesses?

e-invoice has many advantages for businesses such as:

Ø Smooth ITC reconciliation by Auto-reporting of invoices into GST return;

Ø Simultaneous generation of EWB

Ø Utmost reliability (no need to doubt the genuineness- eliminates fake invoices);

Ø Reconciliation problems are eliminated;

Ø Standardisation & eliminates data entry errors;

Ø Documents become tax compliant on real time basis;

Ø Reduction of processing costs; Ø improve payment cycles;

Ø thereby greatly improving overall business efficiency and ensure Ease of doing business.