Dear Friends,

Please find below YouTube video link on How to start beauty parlour business

Regards,

Bipul Kumar

Simplifying your business ideas, structures, functionalities, relations & operations

Dear Friends,

Please find below YouTube video link on How to start beauty parlour business

Regards,

Bipul Kumar

What do you mean by registration of documents?

Registration is recording the matters of a document with an authorized or recognized officer (Registering officer) and preserving the copies of the original document. One needs to register the legal documents so as to prevent any property dispute, fraud, conserve the evidence, be assured of the title and publicizing the information.

Benefits of registration

1. In case registered document is lost or damaged, the registration records prove the authenticity of the document.

2. Title, right of property, case status or an existing liability

3. It prevents forgeries or fraud in transactions specifically in tax, stamp duty etc.

4. Authentic documents/producible as proof in court

Mandatory registration & optional registration of documents

There are two kinds of registration according to The Registration Act, 1908 namely “Mandatory Registration” and “Optional Registration”

Mandatory registration

Section 17 of the Indian Registration Act, 1908 provides for mandatory registration of certain documents. Those are as follows:-

a. purporting to creation, assignment, declaration, extinguishing of any interest in any immovable property worth Rs. 100 and above;

b. which acknowledge receipt or payment of any consideration for creation, assignment, declaration or limitation of any right, title or interest;

Failing to do so will result in transfer being invalid.

Optional registration

Section 18 provides for optional registration of some documents such as:-

Time period of registration of documents:

Place of registration

In case of documents regarding immovable property, it shall be presented for registration in the office of Sub-Registrar within whose district the property or part of it is located (Section 28 of The Registration Act, 1908).

In case of all other documents, they shall be presented:-

The Officer authorized to register a document may on a special cause being shown also go to the individual’s private residence who desires to present a document for registration or deposit a will (Section 31 of The Registration Act, 1908).

Who can apply for registration?

Fees

The prescribed fees for registration of documents shall be paid on presentation of documents (Section 80 of The Registration Act, 1908).

Refer You Tube Video on Registration of documents under the Registration Act, 1908

MOF in Press release today (16 June 2021) says that :

Net Direct Tax collections for the Financial Year 2021-22 have grown at over 100%

Advance Tax collections for F.Y. 2021-22 stand at Rs. 28,780 crore which shows a growth of approximately 146%

Net Direct Tax collections for the F.Y. 2021-22 have grown at a robust pace despite the disruption caused by the COVID-19 pandemic on the economy

Refunds amounting to Rs. 30,731 crore have been issued in the F.Y. 2021-22Posted Date:- Jun 16, 2021

The figures of Direct Tax collections for the Financial Year 2021-22, as on 15.06.2021 show that net collections are at Rs.1,85,871 crore compared to Rs. 92,762 crore over the corresponding period of the preceding year, representing an increase of 100.4% over the collections of the preceding year. The net Direct Tax collections include Corporation Tax (CIT) at Rs. 74,356 crore (net of refund) and Personal Income Tax(PIT) including Security Transaction Tax(STT) at Rs. 1,11,043 crore (net of refund).

The Gross collection of Direct Taxes(before adjusting for refunds) for the F.Y. 2021-22 stands at Rs. 2,16,602 crore compared to Rs. 1,37,825 crore in the corresponding period of the preceding year. This includes Corporation Tax(CIT) at Rs. 96,923 crore and Personal Income Tax (PIT) including Security Transaction Tax(STT) at Rs. 1,19,197 crore. Minor head wise collection comprises Advance Tax of Rs. 28,780 crore, Tax Deducted at Source of Rs.1,56,824 crore, Self-Assessment Tax of Rs. 15,343 crore; Regular Assessment Tax of Rs. 14,079 crore; Dividend Distribution Tax of Rs.1086 crore and Tax under other minor heads of Rs. 491 crore.

Despite extremely challenging initial months of the new Fiscal , the Advance Tax collections for the first quarter of the F.Y. 2021-22 stand at Rs. 28,780 crore against Advance Tax collections of Rs. 11,714 crore for the corresponding period of the immediately preceding Financial Year, showing a growth of approximately 146%. This comprises Corporation Tax(CIT) at Rs. 18,358 crore and Personal Income Tax (PIT) at Rs. 10,422 crore. This amount is expected to increase as further information is received from Banks.

Refunds amounting to Rs. 30,731 crore have also been issued in the F.Y. 2021-22.

****

Ministry of Finance issued Press release on 15th June says that Finance Ministry to hold meeting on 22nd June, 2021 with Infosys on issues in new Income Tax Portal

Senior officials of the Ministry of Finance, Government of India, will hold an interactive meeting on the 22nd of June, 2021, between 11:00 AM to 01:00 PM with Infosys (the vendor and its team) on issues/glitches in the recently launched e-filing portal of the Income Tax Department. Other stakeholders including members from ICAI, auditors, consultants and taxpayers will also be a part of the interaction. The new portal has been fraught with several technical glitches/issues leading to taxpayer inconvenience. Written representations on the problems/difficulties faced in the portal have also been invited from the stakeholders. Representatives from Infosys team will be present to answer queries, clarify issues and receive inputs on the working of the portal, to remove glitches and sort out issues faced by the taxpayers.

Ministry of Consumer Affairs, Food & Public Distribution issued Press release on 15th June 2021, says that

Mandatory Hallmarking of Gold Jewellery comes into force from tomorrow – 16th June,

No penalties till August end in implementation of Gold HallmarkingNo penalties till August end in implementation of Gold Hallmarking

Mandatory Hallmark certification of Gold Jewellery is good for both customers & businesses – Shri Piyush Goyal

Extensive consultations with stakeholders held

Shri Piyush Goyal, Minister for Consumer Affairs, Food & Public Distribution, Railways and Commerce & Industry meets various stake holders involved in Hallmarking of Gold Jewellery in India

Mandatory Hallmarking of Gold Jewellery is going to come into force from tomorrow, 16th June, 2021.

Based on extensive consultations with stakeholders, following decisions were taken-

Old jewellery can be got hallmarked as it is, if feasible by the jeweller or after melting and making new jewellery.

A committee constituting of representatives of all stake holders, revenue officials and legal experts will.be formed to look into the issues that may possibly emerge during the implementation of the scheme.

Shri Goyal said that constructive suggestions are always welcome and implementation should be effective. It may be noted that Hallmarking of Gold Jewellery was earlier set to begin from 15th June 2021.

Under Hallmarking scheme of Bureau of Indian Standards, Jewellers are registered for selling hallmarked jewellery and recognise testing and Hallmarking centres. BIS (Hallmarking) Regulations, were implemented w.e.f. 14.06.2018. Hallmarking will enable Consumers/Jewellery buyers to make a right choice and save them from any unnecessary confusion while buying gold. At present, only 30% of Indian Gold Jewellery is hallmarked.

The Hallmarking of jewellery/artefacts is required to enhance the credibility of gold Jewellry and Customer satisfaction through third party assurance for the marked purity/fineness of gold , consumer protection. This step will also help to develop India as a leading gold market center in the World.

It is to be noted that there has been 25% increase in A&H centers in the last five years. The number of A&H centers have increased from 454 to 945 in the last five years. At present 940 Assaying and Hallmarking centers are operative. Out of this 84 AHCs have been setup under Govt. subsidy scheme in various Districts.

Presently A&H Centre’s can hallmark 1500 articles in a day, the estimated hallmarking capacity of A&H Centre’s per year are 14 crore articles (Assuming 500 articles per shift &300 working days.

According to World Gold Council, India has around 4 lakh jewellers, out of this only 35879 have been BIS certified.

Ministry of Labour and Employment, Government of India has notified the draft rules relating to Employee’s Compensation under the Code on Social Security, 2020 on 03.06.2021 for inviting objections and suggestions, if any, from the stakeholders. Such objections and suggestions are required to be submitted within a period of 45 days from the date of notification of the draft rules.

The Code on Social Security, 2020 amends and consolidates the laws relating to social security with the goal to extend social security to employees and workers in the organised as well as unorganised sectors.

Chapter VII (Employee’s Compensation) of the Social Security Code, 2020 envisages, inter-alia, provisions relating to employer’s liability for compensation in case of fatal accidents, serious bodily injuries or occupational diseases.

The draft Employee’s Compensation rules notified by the Central Government provide for the provisions relating to manner of application for claim or settlement, rate of interest for delayed payment of compensation, venue of proceedings and transfer of matters, notice and manner of transmitting money from one competent authority to another and arrangements with other countries for the transfer of money paid as compensation.

The draft rules under the Code on Social Security, 2020 relating to Employees’ Provident Fund, Employees’ State Insurance Corporation, Gratuity, Maternity Benefit, Social Security and Cess in respect of Building and Other Constructions Workers, Social Security for Unorganised Workers, Gig Workers and Platform Workers and Employment Information were notified on 13.11.2020.

The draft of the Code on social Security (Employee’s Compensation) (Central) Rules, 2021 (Hindi and English) can be accessed at https://labour.gov.in/whatsnew/draft-social-security-employees-compensationcentral-rules-2021-framed-inviting-objections.

*****

MJPS/MS/jkRelease Id :-1727195

Minister for Road Transport & Highways and Micro, Small and Medium Enterprises, Shri Nitin Gadkari announced simplification of process for registration of Micro, Small and Medium Enterprises. Addressing a webinar of SMEStreet GameChangers Forum this evening, Shri Gadkari said that now only PAN and Aadhaar will be required for registration of MSMEs.

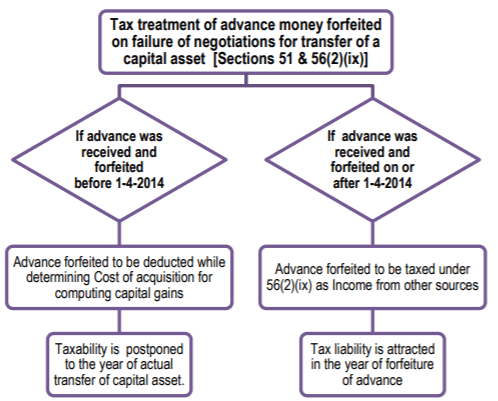

As per section 51 of Income tax Act,1961,Where any capital asset was on any previous occasion the subject of negotiations for its transfer, any advance or other money received and retained by the assessee in respect of such negotiations shall be deducted from the cost for which the asset was acquired or the written down value or the fair market value, as the case may be, in computing the cost of acquisition.

Proviso of Section 51 says that where any sum of money, received as an advance or otherwise in the course of negotiations for transfer of a capital asset, has been included in the total income of the assessee for any previous year in accordance with the provisions of clause (ix) of sub-section (2) of section 56, then, such sum shall not be deducted from the cost for which the asset was acquired or the written down value or the fair market value, as the case may be, in computing the cost of acquisition.

As per section 56(2)(ix) any sum of money received as an advance or otherwise in the course of negotiations for transfer of a capital asset, if,— (a) such sum is forfeited; and (b) the negotiations do not result in transfer of such capital asset shall be chargeable to income-tax under the head “Income from other sources”.

As per interpretation of section 51 & 56(2)(ix) , tax treatment of Advance money/earnest money forfeited as under :

Refer PPT & YouTube link on Tax treatment of Advance money/earnest money forfeited

Thank You !

Bipul Kumar

Business Consultant

RSBK Business Services Private Limited

(A team of CA,CS & Lawyers)

Website: https://businesssosimple.com

Email: rsbkeducationalservices@gmail.com

Contact us: +91-6541-296060, 9304027546 Whatsup no. -9122050937

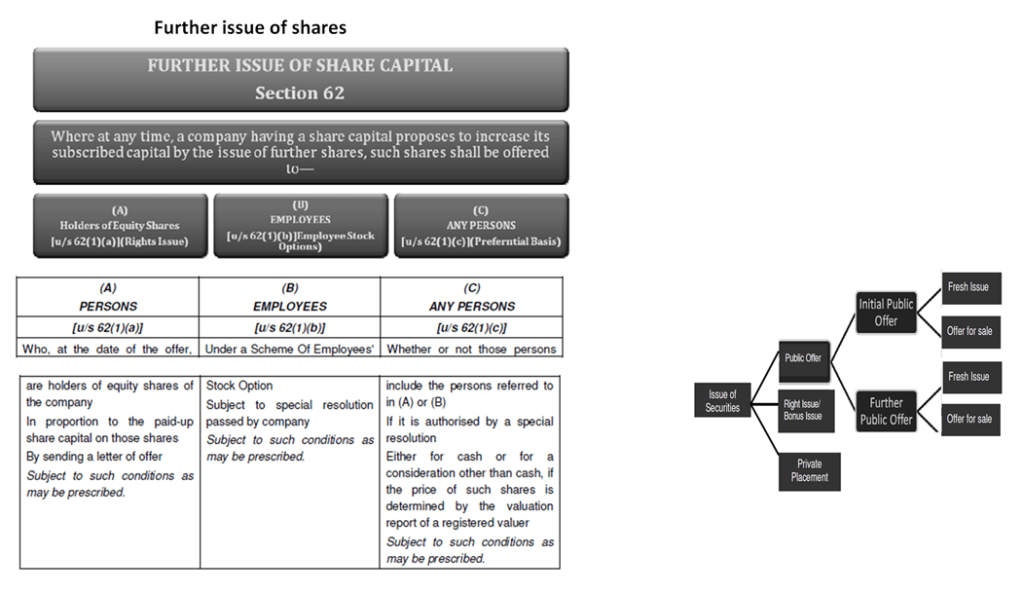

A company can raise funds through issue of securities. Issues of Securities can be classified as a 1. Public 2. Rights or 3. Preferential issues /private placements.

While public and rights issues involve a detailed procedure, private placements or preferential issues are relatively simpler. :

Public offer : “Public offer” includes initial public offer or further public offer of securities to the public by a company, or an offer for sale of securities to the public by an existing shareholder, through issue of a prospectus (Explanation to Section 23).

Private placement: Private placement as any offer or invitation to subscribe or issue of securities to a select group of persons by a company (other than by way of public offer) through private placement offer-cum-application, which satisfies the conditions specified in this section 42 (Explanation I to Section 42)

Offer for sale (OFS) :

Public Offer includes or an offer for sale (OFS) of securities to the public by an existing shareholder, through issue of a prospectus.

Offer for Sale (OFS) is when the promoters (owner) of a listed company sell their shares to the general public. It is a transparent process which takes place on the stock exchange. Only the top 200 companies as per market capitalisation can initiate an OFS.

Unlike IPOs or FPOs, the concept of OFS is fairly new for Indian investors. The Securities and Exchange Board of India (SEBI) introduced OFS in February 2012. This was following a guideline issued by SEBI that promoters cannot hold more than 75% stake in listed companies. Earlier only promoters could participate in an OFS. But now, any shareholder holding more than 10% shares can offer their shares for sale.

Further issue of Shares:

Refer PPT and YouTube Video Link on Issue of Securities-

Thank You !

Bipul Kumar

Business Consultant

RSBK Business Services Private Limited

(A team of CA,CS & Lawyers)

Website: https://businesssosimple.com

Email: rsbkeducationalservices@gmail.com

Contact us: +91-6541-296060, 9304027546 Whatsup no. -9122050937

Every business needs fund for plant/machinery/fixed assets, working capital, business expansion etc. In this video, I have listed some fund raising options available for Private Limited Company as under-

A. Further Issue of Capital–

Right Issue, Employee stock optional plan (“ESOP”), Private Placement/ Preferential Allotment B. Loan and Debenture– Loan, Unsecured Loan from Director and his Relatives, Debenture C. Deposit D. Inter-corporate Deposit E. Angle Investor F. Venture Capital G. Misc– Trade Payble/Creditors , Customer advance.

Please refer YouTube video link (PPT) for details

Regards,

Bipul Kumar