HSN search facility on the basis of Trade/Technical description/HSN – GST advisory 06th Jan 2022

Author: Business So Simple

Hi, I am business consultant working with a team of Chartered Accountants, Company Secretaries, Lawyers & MBAs.

Sovereign Gold Bond Scheme 2021-22 (Series IX) – Issue Price (Press release dated 07th Jan 2022)

In terms of Government of India Notification No.4(5)-B(W&M)/2021 dated October 21, 2021, Sovereign Gold Bonds 2021-22 (Series IX) will be opened for subscription during the period January 10-14, 2022 with Settlement date January 18, 2022. The issue price of the Bond during the subscription period shall be Rs 4,786 (Rupees Four thousand Seven hundred eighty six only) – per gram, as also published by RBI in their Press Release dated January 07, 2022.

The Government of India in consultation with the Reserve Bank of India has decided to allow discount of Rs 50 (Rupees Fifty only) per gram from the issue price to those investors who apply online and the payment is made through digital mode. For such investors the issue price of Gold Bond will be Rs 4,736 (Rupees Four thousand seven hundred thirty six only) per gram of gold.

New Functionalities made available for Taxpayers on GST Portal-05th Jan 2022

New Functionalities made available for Taxpayers on GST Portal-05th Jan 2022

Returns 1. Changes made in Form GSTR-1/IFF

2.Creation of My Masters facility (Product Master/Supplier/Recipient Master) in Form GSTR-1/IFF

3.Allowing entry of suspended GSTINs as recipients in Form GSTR 1/IFF (B2B Tables)

Appeals

- Integration of Appeal Module with Enforcement Module

- Integration of Appeal Module with Assessment Module

Evasion of Customs duty of Rs. 653 crore by M/s Xiaomi Technology India Private Limited (Press release dated 05th Jan 2022)

Based upon an intelligence that M/s Xiaomi Technology India Private Limited (Xiaomi India) was evading customs duty by way of undervaluation, an investigation was initiated by the Directorate of Revenue Intelligence (DRI) against Xiaomi India and its contract manufacturers. During the investigation, searches were conducted by the DRI at the premises of Xiaomi India, which led to the recovery of incriminating documents indicating that Xiaomi India was remitting royalty and licence fee to Qualcomm USA and to Beijing Xiaomi Mobile Software Co. Ltd., under contractual obligation. Statements of key persons of Xiaomi India and its contract manufactures were recorded, during which one of the directors of Xiaomi India confirmed the said payments.

During the investigations, it further emerged that the “royalty and licence fee” paid by Xiaomi India to Qualcomm USA and to Beijing Xiaomi Mobile Software Co. Ltd., China (related party of Xiaomi India) were not being added in the transaction value of the goods imported by Xiaomi India and its contract manufacturers.

The investigations conducted by the DRI further showed that Xiaomi India is engaged in the sale of MI brand mobile phones and these mobile phones are either imported by Xiaomi India or assembled in India by importing parts and components of mobile phones by contract manufacturers of Xiaomi India. The MI brand mobile phones manufactured by the contract manufacturers are sold exclusively to Xiaomi India, in terms of the contract agreement.

Evidence gathered during the investigations by the DRI indicated that neither Xiaomi India nor its contract manufactures were including the amount of royalty paid by Xiaomi India in the assessable value of the goods imported by Xiaomi India and its contract manufacturers, which is in violation of Section 14 of the Customs Act, 1962 and Customs valuation (determination of value of imported goods) Rules 2007. By not adding “royalty and licence fee” into the transaction value, Xiaomi India was evading Customs duty being the beneficial owner of such imported mobile phones, the parts and components thereof.

After completion of the investigation by the DRI, three show cause notices have been issued to M/s Xiaomi Technology India Private Limited for demand and recovery of duty amounting to Rs. 653 crore for the period 01.04.2017 to 30.06.2020, under the provisions of the Customs Act, 1962.

ROC Delhi Adjudication Order for non compliances of Section 203 of CA 2013 (Delay in appointment of Company Secretary) in the case of Yamuna International Airport Pvt. Ltd.

ROC Delhi Adjudication Order for non compliances of Section 203 of CA 2013 (Delay in appointment of Company Secretary) in the case of Yamuna International Airport Pvt. Ltd.

Order passed on 29th Dec 2021 imposing penalty on Company & Director.

👉 Violation of Section 203(4) of CA 2013

(4) If the office of any whole-time key managerial personnel is vacated, the resulting vacancy shall be filled-up by the Board at a meeting of the Board within a period of six months from the date of such vacancy.

Penalty imposed as per Section 203(5) If any company makes any default in complying with the provisions of this section, such company shall be liable to a penalty of five lakh rupees and every director and key managerial personnel of the company who is in default shall be liable to a penalty of fifty thousand rupees and where the default is a continuing one, with a further penalty of one thousand rupees for each day after the first during which such default continues but not exceeding five lakh rupees.

Searches conducted by Income Tax Department largely in Uttar Pradesh and Maharashtra (Press release dated 05th Jan 2022)

The Income Tax Department carried out search and seizure operation on 31.12.2021 on two groups engaged in the business of perfume manufacturing and real estate. Over 40 premises in the states of Uttar Pradesh, Maharashtra, Delhi, Tamil Nadu and Gujarat have been covered during the search action.

In case of the first group primarily based in Mumbai & UP, the search action revealed that the group is involved in tax evasion by under-reporting sale of perfumes, stock manipulation, fudging books of account to shift profits from taxable unit to tax exempt unit, inflation of expenditure, etc. Evidences found in the sales office and main office have revealed that the group makes 35% to 40% of its retail sales in cash by ‘kucha’ bills and these cash receipts are not recorded in the regular books of account, running into crores of rupees. Evidences of booking purchases from bogus parties to the extent of about Rs. 5 crore have also been unearthed.

The analysis of incriminating evidence indicates that unaccounted income so generated is invested in various real estate projects in Mumbai, acquisition of properties both in India and The United Arab Emirates (UAE). It has also been detected that the group has evaded tax of Rs. 10 crore on conversion of the stock-in-trade to capital as corresponding income has not been declared. The group has also not declared income amounting to Rs. 45 crore on the benefits paid to retiring partners.

Evidences have also been found and seized substantiating that the promoters of the group have incorporated some offshore entities. However, such offshore entities have not been reported in their respective Income Tax Returns. The evidences recovered during the search reveal that the offshore entities are run and managed by the Indian promotors. Two of such offshore entities have also been found to own one villa each in the UAE.

It has also been unearthed that one of the offshore entities of the group from the UAE has purportedly introduced illicit share capital of over Rs. 16 crore in an Indian entity of the group, at exorbitant premium. This recipient group entity has also obtained further sum of Rs. 19 crore in the form of illicit share capital from certain Kolkata based shell entities. One of the shareholder directors of these shell entities admitted on oath that he was a dummy director and invested in share capital of the group company at the instance of the promoters of the group.

During the course of search action on another UP based group, incriminating evidences substantiating unrecorded cash transactions of about Rs. 10 crore have been found and seized. It is also gathered that the group is not maintaining any stock register for its inventory.

So far, unaccounted cash exceeding Rs. 9.40 crore and unexplained jewellery of more than Rs. 2 crore have been seized. Several bank lockers have been placed under restraint and are yet to be operated.

Further investigations are in progress.

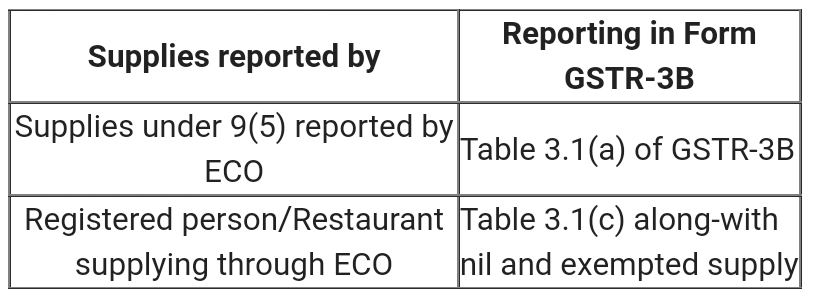

Reporting of supplies notified under section 9(5) / 5(5) by E-commerce Operator in GSTR-3B (GST Portal updates-04 Jan 2022)

- As per the GST Council decision to notify “Restaurant Service” under section 9(5) of the CGST Act, 2017 along with other services notified earlier such as motor cabs, accommodation and housekeeping services wherein the tax on such supplies would be paid by electronic commerce operator if such supplies made through it, Notification No. 17/2021-Central Tax (Rate) and 17/2021-Integrated Tax (Rate) dated 18.11.2021 have been issued. Accordingly, the tax on supplies of restaurant service supplied through e-commerce operators, shall be paid by the e-commerce operator with effect from the 1st January, 2022.

- In light of the above, E-commerce operator and registered person would report taxable supplies notified under section 9(5) of CGST Act, 2017 and similar provisions in IGST/SGST/UTGST Act in the following manner.

- 3. For more details, please refer to CBIC Circular No. 167/23/2021 dated 17.12.2021.

Thanking you,

Team GSTN

ROC Bengaluru Adjudication Order imposing penalty of 1.5 Cr for violation of Section 42(8) of the Companies Act, 2013 in case of Valley Monks Private Limited.

ROC Bengaluru Adjudication Order imposing penalty of 1.5 Cr for violation of Section 42(8) of the Companies Act, 2013 in case of Valley Monks Private Limited.

Year End Review: Legislative Department (Press release 04th Jan 2022)

Various initiatives, Programmes, schemes and achievements of Legislative Department during 2021

Legislative Department acts mainly as a service provider in so far as the legislative business of the Union Government is concerned. It ensures timely processing of legislative proposals of various Ministries/Departments. In this context, Legislative Department plays an important role in assisting the Ministries/Departments of the Government to achieve the policy objectives through legislation. Legislative Department provides assistance to State Governments in translation of Central Laws into the languages mention in the Eighth Schedule to the Constitution.

Important Tasks Undertaken by the Department

During the period from 1st January, 2021 to 22nd December, 2021, this Department has examined 84 Notes for the Cabinet/new legislative proposals and after consulting the concerned Ministries/ Departments, drafted/prepared the draft Bills/Ordinances. After approval of the Cabinet, 50 Bills were forwarded to Parliament for introduction during this period. Bills which were already pending before Parliament and those introduced during the period from 1st January, 2021 to 22nd December, 2021, 46 Bills have been enacted into Acts including the Constitution (One Hundred and Twenty-seventh Amendment Bill, 2021 (As the Constitution 105th Amendment Act, 2021). Total 10 Ordinances have been promulgated by the President under article 123 of the Constitution during the aforesaid period. Further, 1977 statutory rules, regulations, orders and notifications were also scrutinized and vetted by this Department during this period.

Election Laws and Electoral Reforms

To amend the Representation of the People Act, 1950 and the Representation of the People Act, 1951, the Election Laws (Amendment) Bill, 2021 has been passed by Parliament on 21.12.2021. The said Bill envisages the following:

- Linking of Electoral Roll with Aadhaar System will curb the menace of multiple enrolment of the same person in different places; Multiple qualifying dates for enrolment in the electoral roll will expand the voter base and consequently greater participation of eligible voters in the electoral process;

- Making the statutes gender neutral in line with the avowed policy of gender equality and inclusiveness vis-à-vis conduct of our elections; and

- Streamlining the process of conduct of elections with reference to requisition of staff or premises, etc.

Institute of Legislative Drafting and Research (ILI)R)

Legislative drafting is a specialised job which involves drafting skills and expertise. Apart from in-depth knowledge of laws and their regular updation, continuous and sustainable efforts are required to enhance the skills of legislative drafting. The Officers of the Central Government, State Governments and Union territory Administrations dealing with legislative proposals and the students of law need training and orientation to develop the aptitude and the skills in legislative drafting.

2.In January, 1989, with a view to increase the availability of trained officers to deal with legislative proposals as also trained Legislative Counsel in the country, the Institute of Legislative Drafting and Research (ILDR) was established as a Wing of the Legislative Department, Ministry of Law and Justice.

3. The ILDR conducts one Basic Course and one Appreciation Course in Legislative Drafting every year which are as follows:

- The Basic Course is of three months’ duration and meant for the middle level officers of the State Governments/Union territories.

- The Appreciation Course is of fifteen days’ duration for middle level officers of Central Government Ministries/Departments/Attached/Subordinate Offices and Central Public Sector Undertakings.

- There is Voluntary Internship Scheme for students of law. This Scheme is intended to motivate students in creating interest in legislative drafting skills and secure knowledge about the nature and working of the Legislative Department. The Voluntary Internship Scheme has been

devised for Law students who are studying in Third Year of Three Year LLB Course or Fourth or Fifth year of Five year LLB course, with duration from four to six weeks. The said scheme has been started from the year 2013. Due to the Covid — 19 pandemic and social distancing norms the Voluntary Internship Scheme has been temporarily suspended.

devised for Law students who are studying in Third Year of Three Year LLB Course or Fourth or Fifth year of Five year LLB course, with duration from four to six weeks. The said scheme has been started from the year 2013. Due to the Covid — 19 pandemic and social distancing norms the Voluntary Internship Scheme has been temporarily suspended. - An online Capsule course on legislative drafting was organised for three days from 23rd June, 2021 to 25th June, 2021 for middle level officers of Central Government Ministries/Departments/Attached/Subordinate Offices and 29 participants attended the course.

- One month online training in legislative drafting was organised from 8th November, 2021 to 10th December, 2021 for all the officers of State Government/State Legislative Assemblies and 40 participants were benefitted by the training.

India Code Information System (ICIS)

Each year number of legislations (both principal Acts and Amending Acts) are passed by the legislature and it is difficult for judiciary, lawyers as well as citizens to refer relevant and up to date Acts when required. Keeping all these aspects in view, India Code Information System (ICIS), a one stop digital repository of all the Central and State Legislation including their respective subordinate legislations has been developed with the help of NIC under the guidance of Ministry of Law and Justice (Legislative Department). It is an important step in ensuing legal empowerment of all citizens as well as the object of ONE NATION — ONE PLATFORM. Till date, Central Acts from the

Each year number of legislations (both principal Acts and Amending Acts) are passed by the legislature and it is difficult for judiciary, lawyers as well as citizens to refer relevant and up to date Acts when required. Keeping all these aspects in view, India Code Information System (ICIS), a one stop digital repository of all the Central and State Legislation including their respective subordinate legislations has been developed with the help of NIC under the guidance of Ministry of Law and Justice (Legislative Department). It is an important step in ensuing legal empowerment of all citizens as well as the object of ONE NATION — ONE PLATFORM. Till date, Central Acts from the years 1838 to 2021 total 823 Central Acts have been updated and uploaded (in ICIS) for general public.

years 1838 to 2021 total 823 Central Acts have been updated and uploaded (in ICIS) for general public.

Official Language Wing has published the Constitution of India (5 th diglot pocket edition), which was released by Hon’ble Miniser of Law & Justice Shri Kiren Rijiju during the function held at Dr. B. R. Ambedkar Auditorium on 25/11/2021. In this edition, the text of the Constitution of India has been brought up-to-date by incorporating therein all the amendments up the Constitutional (One Hundred and Fifth Amendment) Act, 2021.

GST changes w.e.f. 01st Jan 2022 II 46th GST Council Meeting-31st Dec 2021 (Deferment of GST rate in Textiles ) II GST Portal update -03 Jan 2022 (Implementation of Rule-59(6))

GST changes w.e.f. 01st Jan 2022 II 46th GST Council Meeting-31st Dec 2021 (Deferment of GST rate in Textiles ) II GST Portal update -03 Jan 2022 (Implementation of Rule-59(6))