Gujarat ROC Penalty order for violation of Section 137 read with Section 134 of CA 2013 in the matter of M/S. SVH FABRICS PRIVATE LIMITED

Facts: Company has failed to attach complete Director’s Report (only first page enclosed) in AOC-4, which is a violation attracted penal provisions of Section 137(1) of the CA, 2013 and the company and every officers in default have violated the aforesaid provisions ofthe Companies Act, 2013.

Penalty imposed on Company & all Directors & instructions for fresh filing of Form AOC 4 with additional fees

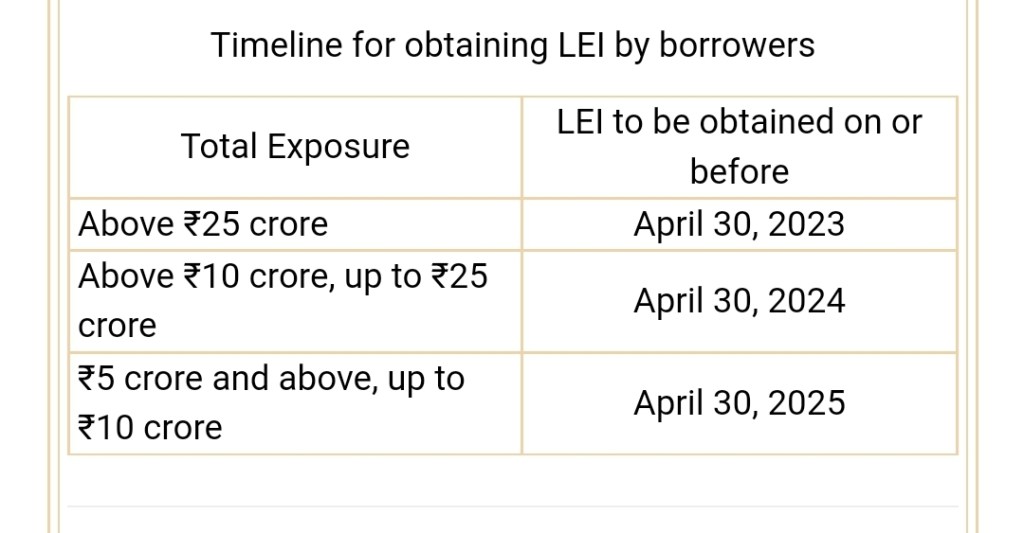

It has been decided that the guidelines on LEI stand extended to Primary (Urban) Co-operative Banks (UCBs) and Non-Banking Financial Companies (NBFCs).

It is further advised that non-individual borrowers enjoying aggregate exposure of ₹5 crore and above from banks and financial institutions (FIs) shall be required to obtain LEI codes as per the timeline given below:

“Exposure” for this purpose shall include all fund based and non-fund based (credit as well as investment) exposure of banks/FIs to the borrower. Aggregate sanctioned limit or or outstanding balance, whichever is higher, shall be reckoned for the purpose. Lenders may ascertain the position of aggregate exposure based on information available either with them, or CRILC database or declaration obtained from the borrower.

Borrowers who fail to obtain LEI codes from an authorized Local Operating Unit (LOU) shall not be sanctioned any new exposure nor shall they be granted renewal/enhancement of any existing exposure. However, Departments/Agencies of Central and State Governments (not Public Sector Undertakings registered under Companies Act or established as Corporation under the relevant statute) shall be exempted from this provision.

These directions are issued under sections 21, 35A and 56 of the Banking Regulation Act, 1949, sections 45JA and 45L of the Reserve Bank of India Act, 1934, section 30A of the National Housing Bank Act, 1987 and section 6 of the Factoring Regulation Act, 2011.

Reduce compliance costs for producers. Ease of formation, business management, taxation and Flexible regulatory compliances

Suggested changes in LLP Act 2008

Incorporation of Producer LLPs by an amendment to the Act

A model agreement be inserted under the LLP Act, 2008 for ready use by Producer LLPs. Model agreement will be helpful in guiding the decisions of the Producer LLP and ensuring smooth functioning.

A producer has been defined as any person engaged in any activity connected with or relatable to primary produce, such as farmers and persons engaged in handloom, handicraft or other cottage industries.

Producer organisations play a pivotal role in reducing transaction costs and provide a forum for members to share mutually beneficial information, coordinate activities and make collective decisions.

It has been further noted that such an institutional support mechanism makes small producer agriculture more viable and can increase producers’ income.

While producer institutions have traditionally been organised in the form of co-operative societies, the concept of Producer Companies was introduced in the Companies Act, 1956 through the Companies (Amendment) Act, 2002. The amendment above sought to include mutual assistance and co-operative principles within the regulatory framework of company law, with suitable modifications. Under Section 378C of the Companies Act, 2013, a producer company may be incorporated where the objects of such company include matters relating to production, harvesting, procurement of primary produce; processing and packaging of produce; manufacture, sale or supply of machinery or equipment to members; providing education on mutual assistance principles to members; and rendering technical consultancy services, training and development for the promotion of interests of its members.

In light of the benefits associated with producer institutions and the comparative

advantages of LLPs vis-à-vis companies, particularly concerning reduced compliance burden, The Company Law Committee (2022) headed by Corporate Affairs Secretary Rajesh Verna (Herein after referred as “ the committee” deliberated whether Producer LLP’s may be incorporated within the LLP Act, 2008.

The Committee noted that Producer LLPs would serve as a more desirable option for small producers since LLPs have been provided with a range of relaxations in the conduct of their affairs. For instance, an LLP is not required to get its accounts audited unless its turnover exceeds Rs. 40 lakhs or its capital contribution exceeds Rs. 25 lakhs. The Committee felt that Producer LLPs are expected to function on a threshold lower than this stipulated limit and agreed that incorporating Producer LLPs would significantly reduce compliance costs for producers. Similarly, the LLP model offers ease of formation, business management, taxation and flexible regulatory compliances, which may be particularly beneficial for producers.

Therefore, to enable producer institutions to take advantage of the light touch regime under the LLP Act, 2008, the Committee recommended enabling the incorporation of Producer LLPs by an amendment to the Act. The Committee further underscored the importance of an LLP Agreement to guide the decisions of the Producer LLP and ensure its smooth functioning. Accordingly, it was recommended that a model agreement be inserted under the LLP Act, 2008 for ready use by Producer LLPs.

Central Government amends Nidhi Rules, 2014 to safeguard the interest of general public

Rules provide that Public Companies desirous to function as Nidhis must obtain prior declaration from the Central Government before accepting deposits

Under the Companies Act, 1956, a Nidhi or Mutual Benefit Society meant a company which the Central Government declared as Nidhi or Mutual Benefit Society by notification in the official gazette. Under the Companies Act, 2013, initially there was no need for a company to get declaration from Central Government to function as a Nidhi Company. Such companies were required to only incorporate as a Nidhi and meet requirements under sub-rule (1) of rule 5 of Nidhi Rules viz., minimum membership of 200, Net Owned Fund (NoF) of Rs. 10 lakh, NOF to deposit ratio of 1:20 and keeping 10% unencumbered deposits in schedule commercial banks or post offices within one year of commencement of Nidhi Rules, 2014.

A committee was constituted in the Ministry to make recommendations on the issues arising from the implementation of the Companies Act, 2013 etc. and it was, inter-alia, felt that the earlier provisions under the Companies Act, 1956 requiring the approval of the Central Government for declaration as Nidhi were appropriate since they provided a centralized and more restrictive frame work for regulation of such entities and accordingly section 406 of the Companies Act, 2013 was amended with effect from 15.08.2019 to bring back the requirement of declaration as a Nidhi by the Central Government.

After the amendment in the Companies Act, 2013 w.e.f. 15.08.2019 and resultant amendments in Nidhi Rules, 2014 w.e.f. 15.08.2019, companies incorporated as Nidhis were required to apply to the Central Government in Form NDH-4 for declaration within 14 months of incorporation, if they were incorporated after the commencement of the Nidhi (Amendment) Rules w.e.f 15.08.2019 and within 09 months of commencement of the Nidhi (Amendment) Rules w.e.f 15.08.2019, if they were incorporated as Nidhis after 2014 but prior to 15.08.2019.

Under the Companies Act, 1956, about 390 companies were declared as Nidhi companies only. During 2014-2019, more than ten thousand companies get incorporated. However, only about 2,300 companies have applied in form NDH-4 for declaration. It has been noticed from examination of form NDH-4 that companies have not been complying with the applicable provisions of the Act and the Nidhi Rules, 2014 (as amended). To safeguard the interest of general public, it has become imperative that before becoming its member, one must ensure declaration of a company as a Nidhi by the Central Government and towards this, few necessary/important amendments in the Rules have been carried out which are applicable to the Companies to be incorporated after Nidhi (amendment) Rule, 2022, as under:-

A Public Company incorporated as a Nidhi with a share capital of Rs. 10 lakhs; needs to first get itself declared as a Nidhi from the Central Government by applying in form NDH-4 with a minimum membership of 200 and NOF of Rs. 20 lac within 120 days of its incorporation.

The Promoters and Directors of the company have to meet the criteria of fit and proper person as laid down in the rules.

For timely disposal, it has also been provided in amended Rules that in case no decision is conveyed by the Central Government within 45 days of the receipt of applications filed by companies in form NDH-4, approval would be deemed as granted. This would apply for such companies which shall be incorporated after Nidhi (Amendment) Rules, 2022.

(i)Non-Audit Services (ii) Punishment under Section 143 (iii) Resignation by auditors (iv) Mandatory joint audit for certain companies (v) Auditor of holding company to comment on the true and fair view of each subsidiary company (iv) Forensic Audit (vii) Standardising Qualifications By Auditors

Auditing is an independent review of a company’s financial information by an ‘auditor’. It is essential in detecting and preventing errors and fraud. Chapter X of the Companies Act, 2013 i.e., Sections 139 to 148, and the Companies (Audit and Auditors) Rules, 2014, govern the manner in which companies are audited under CA-13. This includes provisions on auditors’ appointment, removal and resignation, and eligibility.

The Companies Act, 2013 also envisages penalties for non-compliance with the provisions relating to the discharge of the auditor’s duties. It provides for the power of NCLT to debar auditors if they act fraudulently or abet or collude in any fraud by, or relation to, the company or its directors or officers.

Given the importance of audits and their crucial role in corporate governance, the

Committee deliberated mechanisms to strengthen audits laid down in The Companies Act, 2013. In particular, it discussed the ability to specify varying prohibited non-audit services for different classes of companies. The Committee also discussed the need for suitable amendments to Section 147 concerning punishment for contravention of The Companies Act, 2013, provisions concerning resignations and joint audits.

Non-Audit Services

Section 144 of the Companies Act, 2013 lists certain services that an auditor is prohibited from rendering. This includes services related to accounting, bookkeeping and actuarial services. In addition to the list of prohibited services, it also empowers the Central Government to prescribe any additional service as a ‘prohibited non-audit service’. As per Section 147(2), if an auditor performs such services, she shall be punishable with a fine that is not less than twenty-five thousand rupees but may extend to five lakh rupees or four times the auditor’s remuneration, whichever is less.

In 2018, the Committee of Experts on Regulating Audit Firms and their Networks had considered whether auditors, firms and networks should be prohibited from providing any non-audit services to their auditee companies. It took particular note of international practices concerning such services and observed that:

“While section 144 of the Companies Act, 2013 provides an exhaustive list of prohibited non-audit services, it also authorises the government to prescribe anyother kind of services in this list. The COE has noted that there could be a caseof self-review risk if certain services are allowed to be provided by the auditor.Therefore, there is a need to revisit the list keeping in view the various kind ofservices rendered by auditors, which can possibly result in conflict of interest.”

The Committee deliberated that while Section 144 allows the Central Government to prescribe non-audit services for one or more companies, there is a strong need to formulate different lists for different classes of companies. It felt that companies that do not have a public interest may avail some of the currently prohibited non-audit services from their auditors. In contrast, companies, where the public interest is inherent, must only avail auditrelated services from their auditors, and non-audit services of any kind, directly or indirectly, should be not be rendered by the statutory auditors to the company or its holding, subsidiary or associate company(ies).

In this regard, the Committee took note of the classes of companies for which NFRA has the jurisdiction under Section 132 of CA-13 read with NFRA Rules, 2018, which includes:

“(a) companies whose securities are listed on any stock exchange in India or

outside India;

(b) unlisted public companies having paid-up capital of not less than rupees five

hundred crores or having annual turnover of not less than rupees one thousand

crores or having, in aggregate, outstanding loans, debentures and deposits of not less than rupees five hundred crores as on the 31st March of immediately preceding financial year;

(c) insurance companies, banking companies, companies engaged in the generation or supply of electricity, companies governed by any special Act for

the time being in force or bodies corporate incorporated by an Act in accordance

with clauses (b), (c), (d), (e) and (f) of sub-section (4) of section 1 of the Act;”

In line with these deliberations, the Committee was of the opinion that differing classes of companies may be permitted to avail differing non-audit services from their auditors. Thus, it recommended that Section 144 of the Companies Act, 2013 may be amended to enable the Central Government to prescribe a differential list of prohibitions on availing non-audit services or total prohibition of the same for such class or classes of companies where public interest is inherent, as may be prescribed.

Extract of Section 144

144. Auditor not to render certain services. An auditor appointed under this Act shall provide to the company only such other services as are approved by the Board of Directors or the audit committee, as the case may be, but which shall not include any of the following services (whether such services are rendered directly or indirectly to the company), company or its holding company or subsidiary company, namely:- (a) accounting and book keeping services; (b) internal audit; (c) design and implementation of any financial information system; (d) actuarial services; (e) investment advisory services; (f) investment banking services; (g) rendering of outsourced financial services; (h) management services; and (i) any other kind of services as may be prescribed: Provided that an auditor or audit firm who or which has been performing any non-audit services on or before the commencement of this Act shall comply with the provisions of this section before the closure of the first financial year after the date of such commencement. Explanation.—For the purposes of this sub-section, the term “directly or indirectly” shall include rendering of services by the auditor,— (i) in case of auditor being an individual, either himself or through his relative or any other person connected or associated with such individual or through any other entity, whatsoever, in which such individual has significant influence or control, or whose name or trade mark or brand is used by such individual; (ii) in case of auditor being a firm, either itself or through any of its partners or through its parent, subsidiary or associate entity or through any other entity, whatsoever, in which the firm or any partner of the firm has significant influence or control, or whose name or trade mark or brand is used by the firm or any of its partners.

Punishment under Section 143

Section 143 of the Companies Act, 2013 provides the powers and duties of auditors and auditing standards, including rights of access to books of account and making a report to the company members.

In particular, under Section 143(12), if an auditor of a company has reason to believe that an offence involving fraud is being or has been committed against the company by officers or employees of the company, she needs to report the matter to the Central Government or committee constituted by the Board depending on the amount involved in the suspected fraud.

Section 143(15) provides the penalty if an auditor does not comply with the provisions of sub-section (12). Prior to the amendment of Section 143(15) in 2020, such a defaulting auditor was punishable with a fine, not less than one lakh rupees, but which may extend to twenty-five lakh rupees. However, upon the amendment in 2020, she shall be punishable with a penalty of five lakh rupees in the case of listed companies and one lakh rupees for any other company.

Section 143(15) only provides the penalty for non-compliance of sub-section (12). Noncompliance of other sub-sections was earlier covered by Section 147, which provided that if an auditor contravened any of the provisions of Section 139, 143, 144, or 145, she / it would be punishable with a fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees or four times the remuneration of the auditor, whichever is less.

However, Section 147 was amended in 2020 and inadvertently omitted the entire Section 143 from the purview of punishments.

The Committee noted that after the amendment to Section 147 through the

Companies (Amendment) Act, 2020 (“CAA–20”), auditors are not presently punishable for the contravention of Section 143, except for contravention of Section143(12), which is covered by Section 143(15). To rectify this anomaly, it recommendedthat a suitable amendment may be made to Section 147 to cover penal consequencesfor contravention of Section 143 regarding sub-sections other than sub-section (12).

Extract of Section 143

143. Powers and duties of auditors and auditing standards. (1) Every auditor of a company shall have a right of access at all times to the books of account and vouchers of the company, whether kept at the registered office of the company or at any other place and shall be entitled to require from the officers of the company such information and explanation as he may consider necessary for the performance of his duties as auditor and amongst other matters inquire into the following matters, namely: — (a) whether loans and advances made by the company on the basis of security have been properly secured and whether the terms on which they have been made are prejudicial to the interests of the company or its members; (b) whether transactions of the company which are represented merely by book entries are prejudicial to the interests of the company; (c) where the company not being an investment company or a banking company, whether so much of the assets of the company as consist of shares, debentures and other securities have been sold at a price less than that at which they were purchased by the company; (d) whether loans and advances made by the company have been shown as deposits; (e) whether personal expenses have been charged to revenue account; (f) where it is stated in the books and documents of the company that any shares have been allotted for cash, whether cash has actually been received in respect of such allotment, and if no cash has actually been so received, whether the position as stated in the account books and the balance sheet is correct, regular and not misleading: Provided that the auditor of a company which is a holding company shall also have the right of access to the records of all 8[its subsidiaries and associate companies] in so far as it relates to the consolidation of its financial statements with that of 8[its subsidiaries and associate companies] (2) The auditor shall make a report to the members of the company on the accounts examined by him and on every financial statements which are required by or under this Act to be laid before the company in general meeting and the report shall after taking into account the provisions of this Act, the accounting and auditing standards and matters which are required to be included in the audit report under the provisions of this Act or any rules made thereunder or under any order made under sub-section (11) and to the best of his information and knowledge, the said accounts, financial statements give a true and fair view of the state of the company’s affairs as at the end of its financial year and profit or loss and cash flow for the year and such other matters as may be prescribed. (3) The auditor’s report shall also state— (a) whether he has sought and obtained all the information and explanations which to the best of his knowledge and belief were necessary for the purpose of his audit and if not, the details thereof and the effect of such information on the financial statements; (b) whether, in his opinion, proper books of account as required by law have been kept by the company so far as appears from his examination of those books and proper returns adequate for the purposes of his audit have been received from branches not visited by him; (c) whether the report on the accounts of any branch office of the company audited under sub-section (8) by a person other than the company’s auditor has been sent to him under the proviso to that sub-section and the manner in which he has dealt with it in preparing his report; (d) whether the company’s balance sheet and profit and loss account dealt with in the report are in agreement with the books of account and returns; (e) whether, in his opinion, the financial statements comply with the accounting standards; (f) the observations or comments of the auditors on financial transactions or matters which have any adverse effect on the functioning of the company; (g) whether any director is disqualified from being appointed as a director under sub-section (2) of section 164; (h) any qualification, reservation or adverse remark relating to the maintenance of accounts and other matters connected therewith; **4[(i) whether the company has adequate 6[internal financial controls with reference to financial statements] in place and the operating effectiveness of such controls;] (j) such other matters as may be prescribed. (4) Where any of the matters required to be included in the audit report under this section is answered in the negative or with a qualification, the report shall state the reasons therefor. (5) 1[“In the case of a Government company or any other company owned or controlled, directly or indirectly, by the Central Government, or by any State Government or Government, or partly by the Central Government and partly by one or more State Government, the Comptroller and Auditor-General of India shall appoint the auditor under sub-section (5) or sub-section (7) of section 139 and direct such auditor the manner in which the accounts of the company are required to be audited and”] thereupon the auditor so appointed shall submit a copy of the audit report to the Comptroller and Auditor-General of India which, among other things, include the directions, if any, issued by the Comptroller and Auditor-General of India, the action taken thereon and its impact on the accounts and financial statement of the company. (6) The Comptroller and Auditor-General of India shall within sixty days from the date of receipt of the audit report under sub-section (5) have a right to,— (a) conduct a supplementary audit of the financial statement of the company by such person or persons as he may authorise in this behalf; and for the purposes of such audit, require information or additional information to be furnished to any person or persons, so authorised, on such matters, by such person or persons, and in such form, as the Comptroller and Auditor-General of India may direct; and (b) comment upon or supplement such audit report: Provided that any comments given by the Comptroller and Auditor-General of India upon, or supplement to, the audit report shall be sent by the company to every person entitled to copies of audited financial statements under sub section (1) of section 136 and also be placed before the annual general meeting of the company at the same time and in the same manner as the audit report. (7) Without prejudice to the provisions of this Chapter, the Comptroller and Auditor-General of India may, in case of any company covered under sub-section (5) or sub-section (7) of section 139, if he considers necessary, by an order, cause test audit to be conducted of the accounts of such company and the provisions of section 19A of the Comptroller and Auditor-General’s (Duties, Powers and Conditions of Service) Act, 1971, shall apply to the report of such test audit. (8) Where a company has a branch office, the accounts of that office shall be audited either by the auditor appointed for the company (herein referred to as the company’s auditor) under this Act or by any other person qualified for appointment as an auditor of the company under this Act and appointed as such under section 139, or where the branch office is situated in a country outside India, the accounts of the branch office shall be audited either by the company’s auditor or by an accountant or by any other person duly qualified to act as an auditor of the accounts of the branch office in accordance with the laws of that country and the duties and powers of the company’s auditor with reference to the audit of the branch and the branch auditor, if any, shall be such as may be prescribed: Provided that the branch auditor shall prepare a report on the accounts of the branch examined by him and send it to the auditor of the company who shall deal with it in his report in such manner as he considers necessary. (9) Every auditor shall comply with the auditing standards. (10) The Central Government may prescribe the standards of auditing or any addendum thereto, as recommended by the Institute of Chartered Accountants of India, constituted under section 3 of the Chartered Accountants Act, 1949, in consultation with and after examination of the recommendations made by the National Financial Reporting Authority: Provided that until any auditing standards are notified, any standard or standards of auditing specified by the Institute of Chartered Accountants of India shall be deemed to be the auditing standards. (11) The Central Government may, in consultation with the National Financial Reporting Authority, by general or special order, direct, in respect of such class or description of companies, as may be specified in the order, that the auditor’s report shall also include a statement on such matters as may be specified therein. 3[“Provided that until the National Financial Reporting Authority is constituted under section 132, the Central Government may hold consultation required under this sub- section with the Committee chaired by an officer of the rank of Joint Secretary or equivalent in the Ministry of corporate Affairs and the committee shall have the representatives from the Institute of Chartered Accountants of India and Industry Chambers and also special invitees from the National Advisory Committee on Accounting Standards and the office of the Comptroller and Auditor-General”.] 2[(12) Notwithstanding anything contained in this section, if an auditor of a company in the course of the performance of his duties as auditor, has reason to believe that an offence of fraud involving such amount or amounts as may be prescribed, is being or has been committed in the company by its officers or employees, the auditor shall report the matter to the Central Government within such time and in such manner as may be prescribed: Provided that in case of a fraud involving lesser than the specified amount, the auditor shall report the matter to the audit committee constituted under section 177 or to the Board in other cases within such time and in such manner as may be prescribed: Provided further that the companies, whose auditors have reported frauds under this sub-section to the audit committee or the Board but not reported to the Central Government, shall disclose the details about such frauds in the Board’s report in such manner as may be prescribed.” (13) No duty to which an auditor of a company may be subject to shall be regarded as having been contravened by reason of his reporting the matter referred to in sub-section (12) if it is done in good faith. (14) The provisions of this section shall mutatis mutandis apply to— (a)7 [the cost accountant]conducting cost audit under section 148; or (b) the company secretary in practice conducting secretarial audit under section 204. 8(15) If any auditor, cost accountant or company secretary in practice do not comply with the provisions of sub-section (12),— (a) in case of a listed company, be liable to a penalty of five lakh rupees; and (b) in case of any other company, be liable to a penalty of one lakh rupees.]

Extract of Section 147

147. Punishment for contravention (1) If any of the provisions of sections 139 to 146 (both inclusive) is contravened, the company shall be punishable with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees and every officer of the company who is in default shall be punishable 5[Omitted] with fine which shall not be less than ten thousand rupees but which may extend to 6[one lakh rupees]. (2) If an auditor of a company contravenes any of the provisions of section 139, 7[Omitted], section 144 or section 145, the auditor shall be punishable with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees 1[or four times the remuneration of the auditor, whichever is less] Provided that if an auditor has contravened such provisions knowingly or wilfully with the intention to deceive the company or its shareholders or creditors or tax authorities, he shall be punishable with imprisonment for a term which may extend to one year and 2[with fine which shall not be less than fifty thousand rupees but which may extend to twenty-five lakh rupees or eight times the remuneration of the auditor, whichever is less] (3) Where an auditor has been convicted under sub-section (2), he shall be liable to— (i) refund the remuneration received by him to the company; and (ii) pay for damages to the company, statutory bodies or authorities 3[or to members or creditors of the company] for loss arising out of incorrect or misleading statements of particulars made in his audit report. (4) The Central Government shall, by notification, specify any statutory body or authority or an officer for ensuring prompt payment of damages to the company or the persons under clause (ii) of sub-section (3) and such body, authority or officer shall after payment of damages to such company or persons file a report with the Central Government in respect of making such damages in such manner as may be specified in the said notification. (5) Where, in case of audit of a company being conducted by an audit firm, it is proved that the partner or partners of the audit firm has or have acted in a fraudulent manner or abetted or colluded in any fraud by, or in relation to or by, the company or its Directors or officers, the liability, whether civil or criminal as provided in this Act or in any other law for the time being in force, for such act shall be of the partner or partners concerned of the audit firm and of the firm jointly and severally *4[“Provided that in case of criminal liability of an audit firm, in respect of liability other than fine, the concerned partner or partners, who acted in a fraudulent manner or abetted or, as the case may be, colluded in any fraud shall only be liable.”]

3. Resignation by auditors

The third proviso to Section 139(2) of the Companies Act, 2013 allows auditors to resign from their position. Moreover, Section 140(2) provides the procedure for such resignation. An auditor that resigns from a company shall file a statement within 30 days with the company and the RoC indicating the reasons and other facts as may be relevant about her resignation. Rule 8 of the Companies (Audit and Auditors) Rules, 2014 refers to the form of such a statement, which shall include the ‘reasons for resignation’ and ‘any other facts relevant to the resignation’.

CLC 2016 had deliberated on the provisions concerning the punishment if such a statement is not filed within the prescribed time. It observed:

“Section 140 (3) prescribes a minimum fine of Rupees fifty thousand in case the auditor does not file the statement with regard to his resignation. This fine was considered onerous for auditors of small companies. The Committee recommended that the minimum fine may be reduced to Rupees fifty thousand or the audit fees, whichever is lesser.”

Presently, if an auditor does not comply with the provisions of Section 140(2), Section 140(3) specifies that she shall be liable to a penalty of fifty thousand rupees or an amount equal to her remuneration, whichever is less, and in case of continuing failure, with a further penalty of five hundred rupees for each day after the first during which such failure continues, subject to a maximum of two lakh rupees.

The Committee received representations that there have been several instances of

resignation by auditors despite the concerned provisions. In 2018, the Committee of Experts on Regulating Audit Firms and their Networks had also observed that:

“The year 2018 also witnessed the resignation of several statutory auditors of listed entities over a short period of time. MCA has already ordered investigation to ascertain the reasons behind these resignations.”

In this regard, attention may be drawn to the provision in the UK Companies Act, 2006 concerning the resignation of auditors. An auditor may resign from office on submitting a statement to the company concerning the circumstances of the resignation. An auditor must expressly state the matters which she considers necessary to be brought to the attention of members or creditors of the company. Failure to file such a statement makes the auditor liable to a statutory fine.80 The company must either forward such a statement to the shareholders or approach the relevant adjudicatory body for appropriate directions for not sending such information. The Act also empowers the auditor to requisition a general meeting. She can give a notice to this effect to the company’s Board.

Thus, the Committee was of the opinion that there is a need to review the provisions concerning the resignation of auditors. Particularly, it was felt that there is a need for a resigning auditor to assure the shareholders and other stakeholders that, in her opinion, there is nothing in the company’s accounts which needs to be brought to their notice, and that her resignation is an independent decision. The auditor shall be under

an explicit obligation to make detailed disclosures before resignation and should specifically mention whether such resignation is due to non cooperation from the auditee company, fraud or severe non-compliance, or diversion of funds. Moreover, if such information comes to light after the resignation of an auditor but has not been disclosed in the resignation statement, suitable action may be taken against the resigning auditor. The Committee was of the clear view that similar obligations of a resigning auditor may be borrowed from the UK Companies Act, 2006.

Section 139(2) (2) No listed company or a company belonging to such class or classes of companies as may be prescribed, shall appoint or re-appoint— (a) an individual as auditor for more than one term of five consecutive years; and (b) an audit firm as auditor for more than two terms of five consecutive years: 2&4[Provided that— (i) an individual auditor who has completed his term under clause (a) shall not be eligible for re-appointment as auditor in the same company for five years from the completion of his term; (ii) an audit firm which has completed its term under clause (b), shall not be eligible for re-appointment as auditor in the same company for five years from the completion of such term: Provided further that as on the date of appointment no audit firm having a common partner or partners to the other audit firm, whose tenure has expired in a company immediately preceding the financial year, shall be appointed as auditor of the same company for a period of five years: 5[Provided also that every company, existing on or before the commencement of this Act which is required to comply with the provisions of this sub-section, shall comply with requirements of this sub-section within a period which shall not be later than the date of the first annual general meeting of the company held, within the period specified under sub-section (1) of Section 96, after three years from the date of commencement of this Act.] Provided also that, nothing contained in this sub-section shall prejudice the right of the company to remove an auditor or the right of the auditor to resign from such office of the company.]

140. Removal, resignation of auditor and giving of special notice.1&2 [(1) The auditor appointed under section 139 may be removed from his office before the expiry of his term only by a special resolution of the company, after obtaining the previous approval of the #Central Government in that behalf in the prescribed manner: Provided that before taking any action under this sub-section, the auditor concerned shall be given a reasonable opportunity of being heard.] (2) The auditor who has resigned from the company shall file within a period of thirty days from the date of resignation, a statement in the prescribed form with the company and the Registrar, and in case of companies referred to in sub-section (5) of section 139, the auditor shall also file such statement with the Comptroller and Auditor-General of India, indicating the reasons and other facts as may be relevant with regard to his resignation.

4. Mandatory joint audit for certain companies

Joint audit implies pooling together the resources and expertise of more than one audit firm to share responsibility and produce a single audit report. Section 139(3) of the Companies Act, 2013 allows joint audits. It provides:

“Subject to the provisions of this Act, members of a company may resolve to

provide that —

(a) *****

(b) the audit shall be conducted by more than one auditor. ”

Discussions on mandating joint audits for a class of companies have surfaced previously. In 2003, an ICAI study group had considered whether there should be a joint audit system involving firms of different sizes.83 The study recommended that a framework or a set of guidelines be issued to mandate that a single auditor would not audit companies beyond a particular size. However, noting the several implementation issues that may ensue, it suggested that such a mandate required further deliberation.

Similarly, in 2021, the RBI released new guidelines for statutory auditors of financial entities to enhance independence and address concentration issues. The guidelines require mandatory joint audits for entities having an asset size of Rs. 15,000 crore and above.

Currently, under CA-13, carrying out a joint audit is the prerogative of the company’s members.. The Committee deliberated the need for mandating joint audits for companies with a public interest. However, it was of the opinion that given the expenses associated with joint audits, the mandate should be restricted to a class or classes of companies as the Central Government may deem appropriate.

The Committee was of the opinion that if joint audits were to be made mandatory, this would also require an analysis of the liability of such joint auditors. In this regard, attention may be drawn to the ICAI Statement on Standard Auditing & Assurance Practices on the Responsibility of Joint Auditors. According to the statement, each joint auditor will be liable only for the work allotted to her pursuant to mutual discussions with other auditor/s part-taking in the joint audit.

Thus, given the growing corporate landscape of the country, the Committee was of the view that the Companies Act, 2013 be suitably amended to enable the Central Government to mandate joint audits for such class or class of companies as may be prescribed by the Central Government. In the case of a joint audit, the provisions concerning the extent of liability of individual auditors should also be accordingly provided in the Companies Act, 2013.

5. Auditor of holding company to comment on the true and fair view of each subsidiary company

Presently, proviso to Section 143(1) provides as under:

“Provided that the auditor of a company which is a holding company shall also have the right of access to the records of all its subsidiaries and associate companies in so far as it relates to the consolidation of its financial statements with that of its subsidiaries and associate companies.”

The Committee discussed the issue of large number of cases of diversion of funds through subsidiary companies that are presently taking place and expressed the need for regulatory changes on this matter. In the case of holding companies while the auditor of the holding company has been given the right of access to the records of subsidiary companies, there is currently no statutory obligation or liability on the auditor of the holding company (principal auditor) to formally verify and confirm on the truthfulness and fairness of accounts of subsidiary companies. It was however noticed that SA 600 provides for such requirements.

The Committee deliberated on this issue and viewed that since a holding company makes significant investment in its subsidiary companies, there should be proper oversight, especially on financial matters, of such subsidiary companies by the Board and the auditor of the holding company. The Committee was also informed about the existing auditing standards and practices. The Committee was of the view that suitable amendments may be required to ensure that the auditor of the holding company has been given assurance about the fairness of audit of each subsidiary company by the respective auditors. In addition, the auditor of the holding company may also be empowered to independently verify the accounts or part of accounts of

any subsidiary company. The Committee was however of the view that suitable amendments concerning these matters may be introduced after further examination and public consultation.

6. Forensic Audit

The Committee discussed the need to include the concept of ‘Forensic Audit’ in the Companies Act, 2013 for use in enforcement actions in case of serious non-compliances. It was noted that presently such audit is being conducted on the specific directions of regulators or on demand of creditors. A view was made that there should be clarity on the trigger event for ordering forensic audit and there should be uniformity on this across all regulators.

The Committee recommended that forensic audit may be ordered during investigations, of such nature as may be prescribed, under Chapter XIV (Inspection, Inquiry and Investigation) of the Companies Act, 2013. The Central Government should have the power to prescribe detailed Rules for this purpose through subordinate legislation.

7. Standardising Qualifications By Auditors

The purpose of an audit is to provide authentic information about a company’s state of finances to those who possess a proprietary interest in the company or are involved in its management and control. Accordingly, auditors are entrusted with the duty of preparing financial statements of the company, which depict a true and fair view of the company’s affairs to the best of their knowledge.

Sections 143(3)(f) and 143(3)(h) of CA-13 obligate the auditor to provide observations and comments on financial statements of the company and to provide qualifications, reservations or any adverse remarks, as the case may be, concerning the maintenance of accounts in that company. As such, an auditor is required to express a qualified opinion or an adverse remark if the financial statements indicate certain material misstatements. In case of lack of sufficient evidence to demonstrate that the financial statements are entirely free from misstatements, the auditor is required to provide caution. To formulate such an

adverse opinion, the auditor must be convinced that such misstatement is of material importance.

Further, given that the directors of a company occupy a fiduciary relationship vis-à-vis its shareholders, Section 134(3)(f) of CA-13 requires directors of a company to provide information and explanations on every reservation, qualification, adverse remark or disclaimer contained in the auditor’s report and secretarial audit report on annual financial statements. Where the adverse remark is likely to affect the financial statements or functioning of the company, its potential impact and corrective measures proposed to be taken should also be disclosed in the Board’s report. The Committee noted that while auditors’ reports often highlight reservations or adverse remarks regarding a company’s financial statements, such remarks do not sufficiently elaborate on the corresponding negative effect on the economic health or functioning of the company.

Therefore, to ensure greater clarity, disclosure and standardisation, the Committee proposed that an enabling provision be inserted in CA-13 to allow the Central Government to introduce a format for auditors that would enable them to state the impact of every qualification or adverse remark on the financial statements of the company for circulation to the Board before the same is passed on to shareholders.

Summary:

Observations and Recommendations of the Committee:

CA-13 should enable the Central Government to prescribe a differential list of prohibitions on availing non-audit services for certain classes of companies.

Section 147 of CA-13 should be amended to cover penal consequences for contravention of sub-sections of Section 143 other than sub-section (12).

A resigning auditor should be under an explicit obligation to make detailed disclosures before resignation and should specifically mention whether such resignation is due to noncooperation from the client company, fraud or severe noncompliance, or diversion of funds. Moreover, if such information comes to light after the resignation of an auditor but has not been disclosed in the resignation statement, suitable action may be taken against the resigning auditor. Additionally, the auditor should be mandated to provide assurance about the company’s accounts and independence of her decision to resign.

CA-13 should enable the Central Government to mandate joint audits for such classes of companies as it may deem necessary.

CA-13 should enable the Central Government to order forensic audits in cases of investigation under Chapter XIV in such manner as may be prescribed.

Proposed amendments to the Companies Act 2013

Amendment to Section 139 to empower the Central Government to mandate joint audits for such companies as may be prescribed.

Amendment of Section 140 to provide that a resigning auditor make disclosures concerning non-cooperation from the client company, fraud or severe noncompliance, or diversion of funds, as well as her assurance on the company’s accounts and her decision to resign.

The amendment should also provide a penalty if she fails to make such disclosures.

Amendment to Section 144 to restrict certain companies from availing any non-audit services.

Amendment to Section 147 to cover penal consequences for contravention of sub-sections of Section 143 other than subsection (12). Amendment to Chapter XIV to recognise the concept of forensic audit in such cases, and subject to such Rules, as may be prescribed by the Central Government.

MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 19th April, 2022

G.S.R. 301(E).—In exercise of the powers conferred by sub-section (1) of section 406 read with sub-sections (1) and (2) of section 469 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules, further to amend the Nidhi Rules, 2014, namely:-

1. Short title and commencement.- (1) These rules may be called the Nidhi (Amendment) Rules, 2022. (2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Nidhi rules, 2014 (hereinafter referred to as the said rules), in rule 3, in sub-rule (1), after clause (a), the following clause shall be inserted, namely:- “(aa) „Branch‟ means a place other than the registered office of Nidhi”,

As per the Companies Act 2013 and the Rules framed thereunder, companies are mandated to maintain records in the form of registers that contain particulars relating to their dealings, including information about the company’s directors, shareholders, loans, etc.

Presently, there are about fifteen statutory registers under Companies Act 2013 that companies are obligated to maintain.

The Company Law Committee headed by Corporate Affairs Secretary Rajesh Verna took note of the compliance costs associated with the physical maintenance of statutory registers, particularly given that they require frequent updates. To ease this regulatory burden, the Committee deliberated creating an online platform for maintaining statutory registers under Companies Act 2013.

It was felt that creating such an electronic platform to maintain registers would make the process more secure and transparent, thereby avoiding duplication of effort for companies. It was further noted that a single consolidated platform would make sharing and viewing information stored in such registers easier for all stakeholders.

The Committee was apprised of emerging global regulatory practices that encourage maintaining statutory registers electronically through a platform operated and maintained by the Central Government.

For instance, in Singapore, the Accounting and Corporate Regulatory Authority47 provides an electronic platform and requires companies to maintain and update information in registers on such platform. Similarly, the Modernising Business Registers Program in Australia, implemented as a part of its Digital Business Plan between 2021-2024, proposes establishing Australian Business Registry Services, which aims to streamline how companies register, view, share and maintain business information.

In light of these globally accepted practices and benefits of maintaining registers electronically, the Committee recommended that certain class or classes of companies, as may be prescribed, should be required to compulsorily maintain their registers on an electronic platform in such form and manner as may be prescribed by the Central Government.

For this purpose, the Committee recommended that the Central Government may set up an electronic platform for such registers to be maintained, stored and periodically updated. Additionally, the requirement to include past records pertaining to statutory registers on the electronic platform should also be provided with adequate transitional period.

Observations and Recommendations of the Committee:

Certain companies should be required to mandatorily maintain their registers on an electronic platform in the manner laid down by the Central Government. For this purpose, the Central Government may set up an electronic facility.

The Central Government may direct the company to share the information held on such statutory registers pursuant to certain enforcement-related functions.

Proposed amendments to the Companies Act 2013

Amendment to Section 120 to mandate that prescribed class or classes of companies maintain registers on an electronic facility provided by the Central Government.

Central Government may be allowed to direct the company to share information held on the statutory registers in certain enforcement-related functions.

List of Statutory Registers maintained under the Companies Act 2013 and rules made thereunder:

S No.

Section under CA-13/ Corresponding Rule

Name of Register

1.

Section 42 of CA-13 r/w Rule 14(4) of Companies (Prospectus and Allotment of Securities) Rules, 2014

Record of private placement offers (PAS- 5)

2.

Section 46(3) r/w Rule 6(3)(a) of Companies (Share Capital and Debentures) Rules, 2014

Register of renewed & duplicate share certificates (Form SH-2)

3.

Section 54 r/w Rule 8(14)(a) of Companies (Share Capital and Debentures) Rules, 2014

Register of sweat equity shares (Form SH- 3)

4

Section 62 r/w Rule 12(10)(a) of Companies (Share Capital and Debentures) Rules, 2014

Register of employee stock options (Form SH-6)

5

Section 68(9) r/w Rule 17 (12) (a) of Companies (Share Capital and Debentures) Rules, 2014

Register of shares or securities bought back (Form SH-10)

1. I am new user of MCA system. How can I register?

2. If I am an existing user on Version-2. How do I register?

For the existing Users of MCA fresh/new registration is not required. To login for LLP related filings, you are required to use your existing User ID and Password. After login, the system will identify the user’s existing email ID which was used while user creation in V2 system and show all related history of filings in Application History section in the LLP Module.

If the user attempts to register with a new Email ID which was not associated with the Old V2 system, then User will be registered as a completely New User and in this case, the Application History of the User will not be visible to the user.

3. Who can upgrade to Business User?

4. I am a CA/CS/CMA in Professional Role; can I also have a director role with same user id?

5. What if the User is unable to see his SRNs in the application history?

6. What if a User has registered wrong DSC with his User ID?

7. Where can I see my resubmission comments?

This facility is available in the “My Application” tab. In the application history, Users will see “View Remarks” action button against the SRN marked under resubmission (RSUB). Users can click on “View Remarks” to see the comments by the MCA officers related to being asked for resubmission of the already filed SRN.

During the Financial Year 2021-22, Ministry of Corporate Affairs (MCA) registered more than 1.67 Lakh company incorporations as compared to 1.55 Lakh companies during FY 2020-21.

The increase is significant considering that number of companies incorporated during Financial Year 2020-21 were the highest in any of the previous years. The incorporations during FY 2021-22 are 8% more than the incorporations during FY 2020-21. While MCA had registered 1.24 lakh companies during FY 2018-19 and 1.22 lakh companies in 2019-20 respectively, it had registered 1.55 Lakh companies during FY 2020-21.

As part of Government of India’s drive for Ease of Doing Business (EoDB), the MCA has taken many initiatives thereby saving as many procedures, time and cost for starting a business in India.

The MCA launched SPICe+ form in February 2020 and also integrated 11 different services mentioned below, across 3 Central Government Ministries/Departments (Ministry of Corporate Affairs, Ministry of Labour & Department of Revenue in the Ministry of Finance), 3 State Governments (Maharashtra, Karnataka and West Bengal), and NCT of Delhi:

Name Reservation

Company Incorporation

Director Identification Number

EPFO Registration No.

ESIC Registration Number

PAN

TAN

Profession Tax Registration Number for the state of Maharashtra, Karnataka and West Bengal

Bank Account number and

GSTN Number (on Optional basis)

Shop and Establishment Registration No. for NCT of Delhi.

During FY 2021-22, the States having the highest number of registrations were Maharashtra (31,107 companies) followed by Uttar Pradesh (16,969 companies) Delhi (16,323 companies) Karnataka (13,403 companies) and Tamil Nadu (11,020 companies).

Sector wise, the maximum number of companies were incorporated in the Business Services (44,168 companies), followed by Manufacturing (34,640 Companies) Community, personal & Social Services (23,416 companies) and Agriculture & Allied Activities (13,387 companies).

The MCA is continuously striving to transform regulatory environment and has taken several measures in recent past towards EoDB like:-

Revision of Definition of Small Companies which has reduced compliance burden on about 2 lakh companies

Zero MCA fee for company incorporation up to Rs 15 lakh authorised capital

Incentivisation of incorporation of One Person Companies (OPCs)

De-criminalisation of technical & procedural violations under Companies & LLP Act.

As part of the ongoing ‘Azadi Ka Amrit Mahotsav’ celebrations, the Insolvency and Bankruptcy Board of India (IBBI) in collaboration with MyGov.in and BSE Investors’ Protection Fund is conducting the ‘3rd National Online Quiz on Insolvency and Bankruptcy Code, 2016’, to promote awareness and understanding of the Code among various stakeholders, across the country. The Quiz is open from 16th April, 2022 to 15th May, 2022.

The 3rd edition Quiz has been launched in continuation to the two quiz organized earlier, in the years 2020 and 2021, which evinced an overwhelming response, with over 1.9 lakh participants, in total, representing all the States and Union Territories of the country. The Quiz received interest from a wide range of stakeholders, including students, professionals and employees.

The Quiz shall be open on the MyGov portal https://quiz.mygov.in for all Indian citizens above 18 years of age, except for individuals working in IBBI, BSE Investors’ Protection Fund and service providers registered with IBBI, as also their immediate family members.

The best performer will be awarded a Gold Medal along with a cash prize of Rs. 1,00,000/- (One lakh rupees only). The second-best performer will be awarded a Silver Medal along with a cash prize of Rs. 50,000/- (Fifty thousand rupees only) and the third best performer will be receiving a Bronze Medal along with a cash prize of Rs. 25,000/- (Twenty five thousand rupees only). The next ten best performers will be awarded consolation prizes of Rs. 10,000/- (Ten thousand rupees only) each. Additionally, the top 10% performers shall be awarded ‘Certificates of Merit’ and all the participants will receive ‘Certificates of Participation’. The cash prizes and medals are sponsored by the BSE Investors’ Protection Fund, as part of its investor awareness initiatives.

The IBBI encourages everyone to participate in the Quiz and have a chance to win attractive prizes along with fostering a heightened awareness and knowledge about the Code.