The Financial Intelligence Unit-India (FIU-IND), in furtherance of the powers conferred upon the Director FIU-IND under Section 13(2)(d) of the Prevention of Money Laundering Act (PMLA), 2002, has imposed a monetary penalty of Rs. 5,49,00,000 (rupees five crore forty nine lakh) on Paytm Payments Bank Ltd with reference to the violations of its obligations under the PMLA read with the Prevention of Money Laundering (Maintenance of Records) Rules, 2005 (PML Rules) issued thereunder and applicable guidelines and advisories issued by the Director FIU-IND.

FIU-IND initiated a review of the Paytm Payments Bank Ltd on receipt of specific information from law enforcement agencies in respect of few entities and their network of businesses engaged in a number of illegal acts, including organising and facilitating online gambling. Further, the money generated from these illegal operations, i.e. proceeds of crime were routed and channelled through bank accounts maintained by these entities with the Paytm Payments Bank Ltd.

In furtherance of the above and upon scrutiny of the documents on record, FIU IND issued a compliance Show Cause Notice to the bank for its violations of (i) Rules 7(3) and 2(1)(g), PML Rules; (ii) violation of Rule 8(2) read with Rule 3(1)(D) and Rule 2(1)(g); (iii) violation of Rule 9(12), PML Rules; and (iv) violation of Rule 9(14) in terms of AML / CFT / KYC safeguards in respect of Payout services; and AML / CFT / KYC in respect of beneficiary accounts.

After considering the written and oral submissions of the Paytm Payments Bank Ltd, Director, FIU-IND, based on the voluminous material available on record, found that the charges against Paytm were substantiated. Consequently, vide order dated March 1st, 2024 in exercise of his powers under Section 13, PMLA, it was found to be appropriate to impose a penalty of Rs. 5,49,00,000.

FAQs : ₹2000 Denomination Banknotes – Withdrawal from Circulation; Will continue as Legal Tender

1. Why are ₹2000 denomination banknotes being withdrawn? The ₹2000 denomination banknote was introduced in November 2016 under Section 24(1) of RBI Act, 1934 primarily with the objective to meet the currency requirement of the economy in an expeditious manner after withdrawal of the legal tender status of all ₹500 and ₹1000 banknotes in circulation at that time. With fulfilment of that objective and availability of banknotes in other denominations in adequate quantities, printing of ₹2000 banknotes was stopped in 2018-19. A majority of the ₹2000 denomination notes were issued prior to March 2017 and are at the end of their estimated life-span of 4-5 years. It has also been observed that this denomination is not commonly used for transactions. Further, the stock of banknotes in other denominations continue to be adequate to meet the currency requirement of the public. In view of the above, and in pursuance of the “Clean Note Policy” of the Reserve Bank of India, it has been decided to withdraw the ₹2000 denomination banknotes from circulation.

2. What is Clean Note Policy? It is a policy adopted by RBI to ensure availability of good quality banknotes to the members of public.

3. Does the legal tender status of ₹2000 banknotes remain? Yes. The ₹2000 banknote will continue to maintain its legal tender status.

4. Can ₹2000 banknotes be used for normal transactions? Yes. Members of the public can continue to use ₹2000 banknotes for their transactions and also receive them in payment. However, they are encouraged to deposit and/or exchange these banknotes on or before September 30, 2023.

5. What should the public do with the ₹2000 denomination banknotes held by them? Members of the public may approach bank branches for deposit and/or exchange of ₹2000 banknotes held by them. The facility for deposit into accounts and exchange for ₹2000 banknotes will be available at all banks until September 30, 2023. The facility for exchange will be available also at the 19 Regional Offices (ROs) of RBI having Issue Departments1 until September 30, 2023.

6. Is there a limit on deposit of ₹2000 banknotes into a bank account? Deposit into bank accounts can be made without restrictions subject to compliance with extant Know Your Customer (KYC) norms and other applicable statutory / regulatory requirements.

7. Is there an operational limit on the amount of ₹2000 banknotes that can be exchanged? Members of the public can exchange ₹2000 banknotes upto to a limit of ₹20,000/- at a time.

8. Can ₹2000 banknotes be exchanged through Business Correspondents (BCs)? Yes, exchange of ₹2000 banknotes can be made through BCs upto a limit of ₹4000/- per day for an account holder.

9. From which date will the exchange facility be available? To give time to the banks to make preparatory arrangements, members of the public are requested to approach the bank branches or ROs of RBI from May 23, 2023 for availing exchange facility.

10. Is it necessary to be a customer of the bank to exchange ₹2000 banknotes from its branches? No. A non-account holder also can exchange ₹2000 banknotes up to a limit of ₹20,000/- at a time at any bank branch.

11. What if someone needs more than ₹20,000/- cash for business or other purposes? Deposit into accounts can be made without restrictions. The ₹2000 banknotes can be deposited into bank accounts and cash requirements can be drawn thereafter, against these deposits.

12. Is there any fee to be paid for the exchange facility? No. The exchange facility shall be provided free of cost.

13. Will there be special arrangements for senior citizens, persons with disabilities, etc. for exchange and deposit? Banks have been instructed to make arrangements to reduce inconvenience to the senior citizens, persons with disabilities, etc., seeking to exchange/deposit ₹2000 banknotes.

14. What will happen if one cannot deposit / exchange ₹2000 banknote immediately? To make the entire process smooth and convenient for the public, a period of over four months has been given for deposit and/or exchange of ₹2000 banknotes. Members of the public, are therefore, encouraged to avail this facility at their convenience within the allotted time.

15. What will happen if a bank refuses to exchange / accept deposit of ₹2000 banknote? For redress of grievance in case of deficiency of service, the complainant / aggrieved customer may first approach the concerned bank. If the bank does not respond within a period of 30 days after lodging of the complaint or if the complainant is not satisfied with the response/resolution given by the bank, the complainant can lodge the complaint under the Reserve Bank – Integrated Ombudsman Scheme (RB-IOS), 2021 at the Complaint Management System portal of RBI (cms.rbi.org.in).

RBI Press Release 19th May 2023

₹2000 Denomination Banknotes – Withdrawal from Circulation; Will continue as Legal Tender

The ₹2000 denomination banknote was introduced in November 2016 under Section 24(1) of RBI Act, 1934, primarily to meet the currency requirement of the economy in an expeditious manner after the withdrawal of legal tender status of all ₹500 and ₹1000 banknotes in circulation at that time. The objective of introducing ₹2000 banknotes was met once banknotes in other denominations became available in adequate quantities. Therefore, printing of ₹2000 banknotes was stopped in 2018-19.

2. About 89% of the ₹2000 denomination banknotes were issued prior to March 2017 and are at the end of their estimated life-span of 4-5 years. The total value of these banknotes in circulation has declined from ₹6.73 lakh crore at its peak as on March 31, 2018 (37.3% of Notes in Circulation) to ₹3.62 lakh crore constituting only 10.8% of Notes in Circulation on March 31, 2023. It has also been observed that this denomination is not commonly used for transactions. Further, the stock of banknotes in other denominations continues to be adequate to meet the currency requirement of the public.

3. In view of the above, and in pursuance of the “Clean Note Policy” of the Reserve Bank of India, it has been decided to withdraw the ₹2000 denomination banknotes from circulation.

4. The banknotes in ₹2000 denomination will continue to be legal tender.

5. It may be noted that RBI had undertaken a similar withdrawal of notes from circulation in 2013-2014.

6. Accordingly, members of the public may deposit ₹2000 banknotes into their bank accounts and/or exchange them into banknotes of other denominations at any bank branch. Deposit into bank accounts can be made in the usual manner, that is, without restrictions and subject to extant instructions and other applicable statutory provisions.

7. In order to ensure operational convenience and to avoid disruption of regular activities of bank branches, exchange of ₹2000 banknotes into banknotes of other denominations can be made upto a limit of ₹20,000/- at a time at any bank starting from May 23, 2023.

8. To complete the exercise in a time-bound manner and to provide adequate time to the members of public, all banks shall provide deposit and/or exchange facility for ₹2000 banknotes until September 30, 2023. Separate guidelines have been issued to the banks.

9. The facility for exchange of ₹2000 banknotes upto the limit of ₹20,000/- at a time shall also be provided at the 19 Regional Offices (ROs) of RBI having Issue Departments1 from May 23, 2023.

10. The Reserve Bank of India has advised banks to stop issuing ₹2000 denomination banknotes with immediate effect.11. Members of the public are encouraged to utilise the time up to September 30, 2023 to deposit and/or exchange the ₹2000 banknotes. A document on Frequently Asked Questions (FAQs) in the matter has been hosted on the RBI website for information and convenience of the public.

(Yogesh Dayal) Chief General ManagerPress Release: 2023-2024/257

RBI Notification dated 22 May 2023

₹2000 Denomination Banknotes – Withdrawal from Circulation; Will continue as Legal Tender

RBI/2023-24/33 DCM(Plg) No.S-239/10.27.00/2023-24

May 22, 2023

The Chairman / Managing Director/ Chief Executive Officer All Banks

Dear Sir /Madam,

₹2000 Denomination Banknotes – Withdrawal from Circulation; Will continue as Legal Tender

2. The facility of exchange of ₹2000 banknotes across the counter shall be provided to the public in the usual manner, that is, as was being provided earlier.

3. Banks are advised to provide appropriate infrastructure at the branches such as shaded waiting space, drinking water facilities, etc. considering the summer season.

4. Banks shall maintain daily data on deposit and exchange of ₹2000 banknotes in the format given below and submit the same as and when called for.

As per Section 2(5) of the Companies Act, 2013 “articles” means the articles of association of a company as originally framed or as altered from time to time or applied in pursuance of any previous company law or of this Act;

By-laws or rules and regulations which govern the management of its internal affairs and the conduct of its business.

Company can alter its AOA by way of addition, deletion, modification, substitution, or combination of them.

They are framed with the object of carrying out the aims and objects as set out in the Memorandum of Association.

Legal provisions:

Section 14 of the Companies Act, 2013

14. Alteration of Articles

(1) Subject to the provisions of this Act and the conditions contained in its memorandum, if any, a company may, by a special resolution, alter its articles including alterations having the effect of conversion of–(a) a private company into a public company; or(b) a public company into a private company:

Provided that where a company being a private company alters its articles in such a manner that they no longer include the restrictions and limitations which are required to be included in the articles of a private company under this Act, the company shall, as from the date of such alteration, cease to be a private company:

[Provided further that any alteration having the effect of conversion of a public company into a private company shall not be valid unless it is approved by an order of the Central Government on an application made in such form and manner as may be prescribed:Provided also that any application pending before the Tribunal, as on the date of commencement of the Companies (Amendment) Ordinance, [2019], shall be disposed of by the Tribunal in accordance with the provisions applicable to it before such commencement.]]]*

(2) Every alteration of the articles under this section and a copy of the order of the [Central Government]] Tribunal approving the alteration as per sub-section (1) shall be filed with the Registrar (INC -27), together with a printed copy of the altered articles, within a period of fifteen days in such manner as may be prescribed, who shall register the same.(3) Any alteration of the articles registered under sub-section (2) shall, subject to the provisions of this Act, be valid as if it were originally in the articles.

Procedure :

Notice of Board Meeting :

Issue notice in writing to every director

The notice must be a seven day notice.

The notice must contain time, date and venue for the meeting and detailed agenda of the business, Notes to agenda & draft resolution.

(As per section 173 and SS-1)

2. Hold Board Meeting

Consider and decide which of the articles are to be altered and pass a formal resolution in this respect (Refer Draft resolution).

Approve notice, agenda and explanatory statement to be annexed to the notice of the general meeting as per 102 of the Act (Refer Draft resolution & Explanatory statement).

Authorize the Company Secretary or any other competent officer of the company to issue notice of the general meeting as approved by the Board.

3. Notice of General Meeting:

Issue notice of the general meeting to all the members of the company, its directors and the auditors (Section 101).

.4.Hold the general meeting

Check the Quorum;

Check whether auditor is present, if not. Then Leave of absence is Granted or Not. (Section- 146) and

Pass the proposed special resolution.[Section-114(2)],

Approval of Alteration in AOA.

5. File with the ROC, Form MGT – 14 within 30 days

File with the ROC, Form MGT – 14 along with a certified copy of the special resolution and the explanatory statement annexed to the notice of the general meeting at which the resolution was passed and a copy of the Articles of Association, within 30 days of the passing of the resolution along with the prescribed filing fee.

6. File with the ROC, Form INC-27 within 15 days

Every alteration of the articles under this section and a copy of the order of the [Central Government]] Tribunal approving the alteration as per sub-section (1) shall be filed with the Registrar (INC -27), together with a printed copy of the altered articles, within a period of fifteen days in such manner as may be prescribed, who shall register the same.

7. Make necessary changes in all the copies of the articles of association of the company lying in the office of the company.

For Listed Company:

Sendcopiesofthenoticetoeachstockexchange where the securities of the company are listed within 24 hour of the occurrence of event [Refer Regulation 30(6) of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015]. A general notice of the general meeting may also be published in newspapers.

Intimate stockexchange about alterations in memorandum and articles of the company within 24 hours of the occurrence of event. [Refer Regulation 30(6) of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015]

Send to each stock exchanges, a copy of the proceedings of the general meeting in case of a listed company within 24 hour of the occurrence of event [Refer Regulation 30(6) of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015].

Draft Agenda, proposal, resolution of Board Meeting, Minutes – Gist of Discussion

Agenda Title: To amend Articles of Association of the Company

Proposal

An amendment to the AOA of the Company is required in view of __________. A detailed proposal is placed before the Board for the same.

The Board members may discuss and approve the following resolution.

Proposed Resolution

“Resolved that subject to the provisions of Section 14 and other applicable provisions, if any, of the Companies Act, 2013 and subject to the approval of the members at the General Meeting, the Articles of Association of the Company be and hereby amended by inclusion of the following clause at__________________.

Resolved further that an Extraordinary General Meeting of the members of the Company be called and held at _______ on _________ day of_________at ___________ as per the draft notice and explanatory statement placed before the meeting duly initiated by the Chairperson for the purpose of identification.

Resolved further that the draft notice of Extraordinary General Meeting be and is hereby approved and the Company Secretary and the Directors be and are hereby authorized severally to issue the said notice to the members and others who are entitled for the same, and take all necessary action in this regard.

Resolved further that Directors and the Company Secretary of the Company be and are hereby authorized severally to file necessary e-forms with the Registrar of Companies, __________, in applicable e-Forms and to do all such acts, deeds and things as may be necessary to give effect to the above resolution.”

Minutes – Gist of Discussion

The Board discussed the proposal to amend the Articles of Association of the Company in view of ____________, a copy of which was tabled at the meeting for approval. The following resolution was approved.

Draft Agenda, Explanatory Statement, proposal, resolution of General Meeting, Minutes – Gist of Discussion

Agenda Title: Amendment to Articles of Association

Proposed Resolution

To consider and, if thought fit, to pass with or without modification(s), the following resolution as a Special Resolution:

“Resolved that pursuant to Section 14 of the Companies Act, 2013, the Articles of Association of the Company be and is hereby altered as below:________________.

Resolved further that the Board of Directors and Company Secretary be and are hereby severally authorised to sign all such forms and returns and other documents and to do all such acts, deeds and things as may be necessary to give effect to the aforesaid resolution.”

Minutes – Gist of Discussion

Proposed by _________________, seconded by ___________ Resolution passed unanimously/ by majority / rejected.

Explanatory Statement

The Board of Directors of the Company at its meeting held on DD/MM/YYYY_ recommended that the existing Article of Association be altered with the text as set out in the resolution. Consent of the Members by way of Special Resolution is required for such alteration of Articles of Association in terms of the provisions of Section 14 of the Act.

None of the Directors and Key Managerial Personnel of the Company, or their relatives, is interested in this Special Resolution.

The Board recommends this Special Resolution for your approval.

Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman approves the final Sovereign Green Bonds framework of India. This approval will further strengthen India’s commitment towards its Nationally Determined Contribution (NDCs) targets, adopted under the Paris Agreement, and help in attracting global and domestic investments in eligible green projects. The proceeds generated from issuance of such bonds will be deployed in Public Sector projects which help in reducing carbon intensity of the economy.

The Framework comes close on the footsteps of India’s commitments under “Panchamrit” as elucidated by the Prime Minister, Shri Narendra Modi, at COP26 at Glasgow in November, 2021. The approval is fulfillment of the announcement in the Union Budget FY 2022-23 by the Union Finance Minister that Sovereign Green Bonds will be issued for mobilising resources for green projects.

Green bonds are financial instruments that generate proceeds for investment in environmentally sustainable and climate-suitable projects. By virtue of their indication towards environmental sustainability, green bonds command a relatively lower cost of capital vis-à-vis regular bonds and necessitates credibility and commitments associated with the process of raising bonds.

In the above context, India’s first Sovereign Green Bonds framework was formulated and as per the provisions of the framework, Green Finance Working Committee (GFWC) was constituted to validate key decisions on issuance of Sovereign Green Bonds.

Further, CICERO, an independent and globally renowned Norway-based Second Party Opinion (SPO) provider, was appointed to evaluate India’s green bonds framework and certify alignment of the framework with ICMA’s Green Bond Principles and international best practices. After due deliberation and consideration, CICERO has rated India’s Green Bonds Framework as ‘Medium Green’ with a “Good” governance score.

The report can be downloaded from the following link:

In terms of Government of India Notification No.4(6)-B(W&M)/2022 dated June 15, 2022, Sovereign Gold Bonds 2022-23 (Series II) will be opened for subscription during the period August 22-26, 2022 with Settlement date August 30, 2022. The issue price of the Bond during the subscription period shall be Rs 5,197 (Rupees five thousand one hundred ninety seven only) per gram, as also published by RBI in their Press Release dated August 19, 2022.

Government of India in consultation with the Reserve Bank of India has decided to allow discount of Rs 50 (Rupees Fifty only) per gram from the issue price to those investors who apply online and the payment is made through digital mode. For such investors the issue price of Gold Bond will be Rs 5,147 (Rupees five thousand one hundred forty seven only) per gram of gold.

At present, e-invoice is mandatory for businesses with an annual turnover of over Rs.20 crores.

government is planning to make GST e-invoicing mandatory for companies with a turnover of Rs 5 crore and above, thus bringing the threshold down from the current Rs 20 crore, according to a government official.

FCRA registration extended to later of 30.9.2022 or till disposal of renewal application where validity extended till 30 June or expiring from Jul-Sep. 2022.

Company Law Adjudication & Appeal Updates -24 June 2022

Bangalore ROC Penalty order for violation of Section 170 of the Companies Act 2013 in the matter of Landomus Realty Pvt. Ltd.

👉 Default

One of the Directors has signed the documents as a capacity of Chairman & CEO during the course of inquiry u/s 206 of the Companies Act 2013. But as per records no resolution has been passed appointing him CEO by the Company or the board.

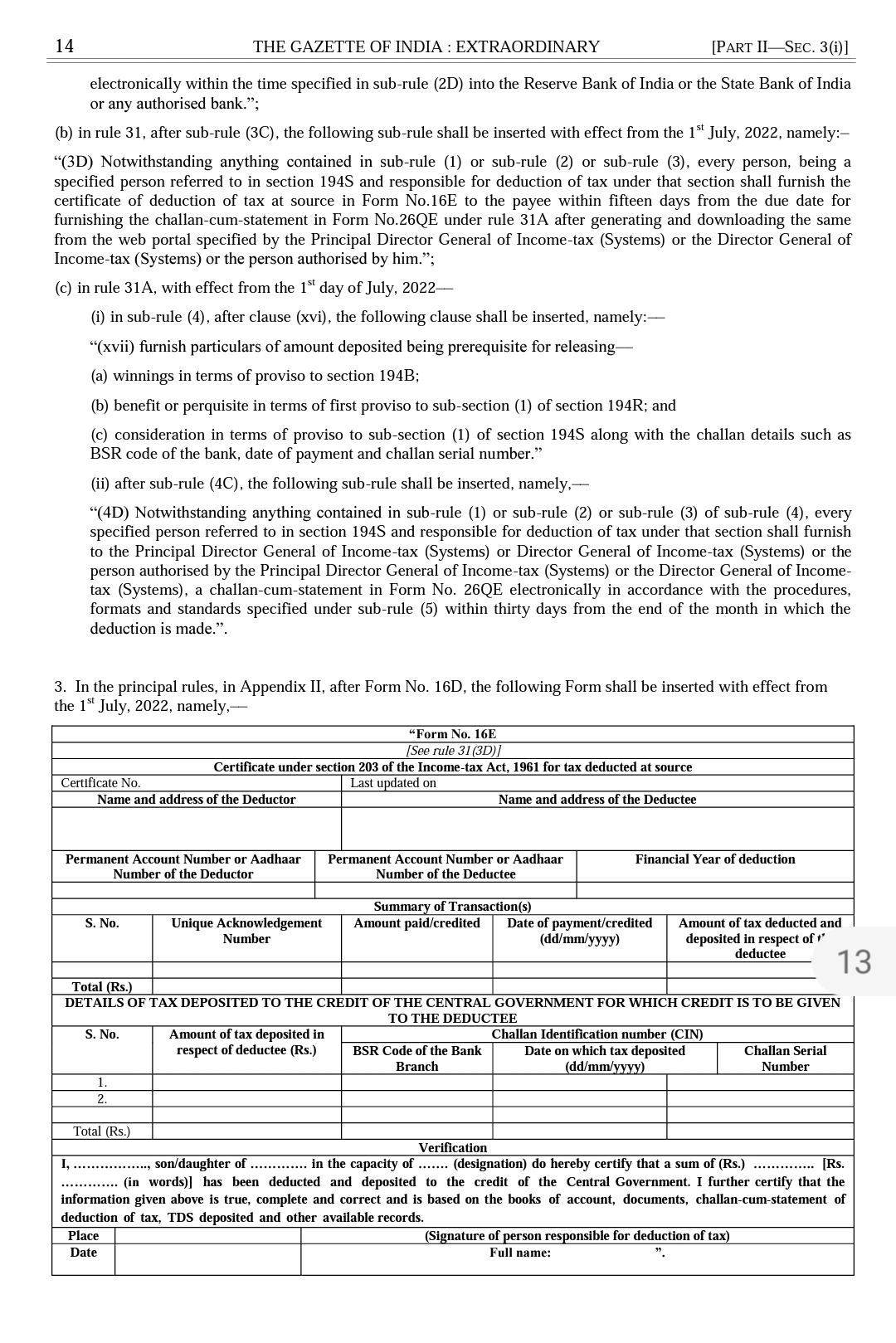

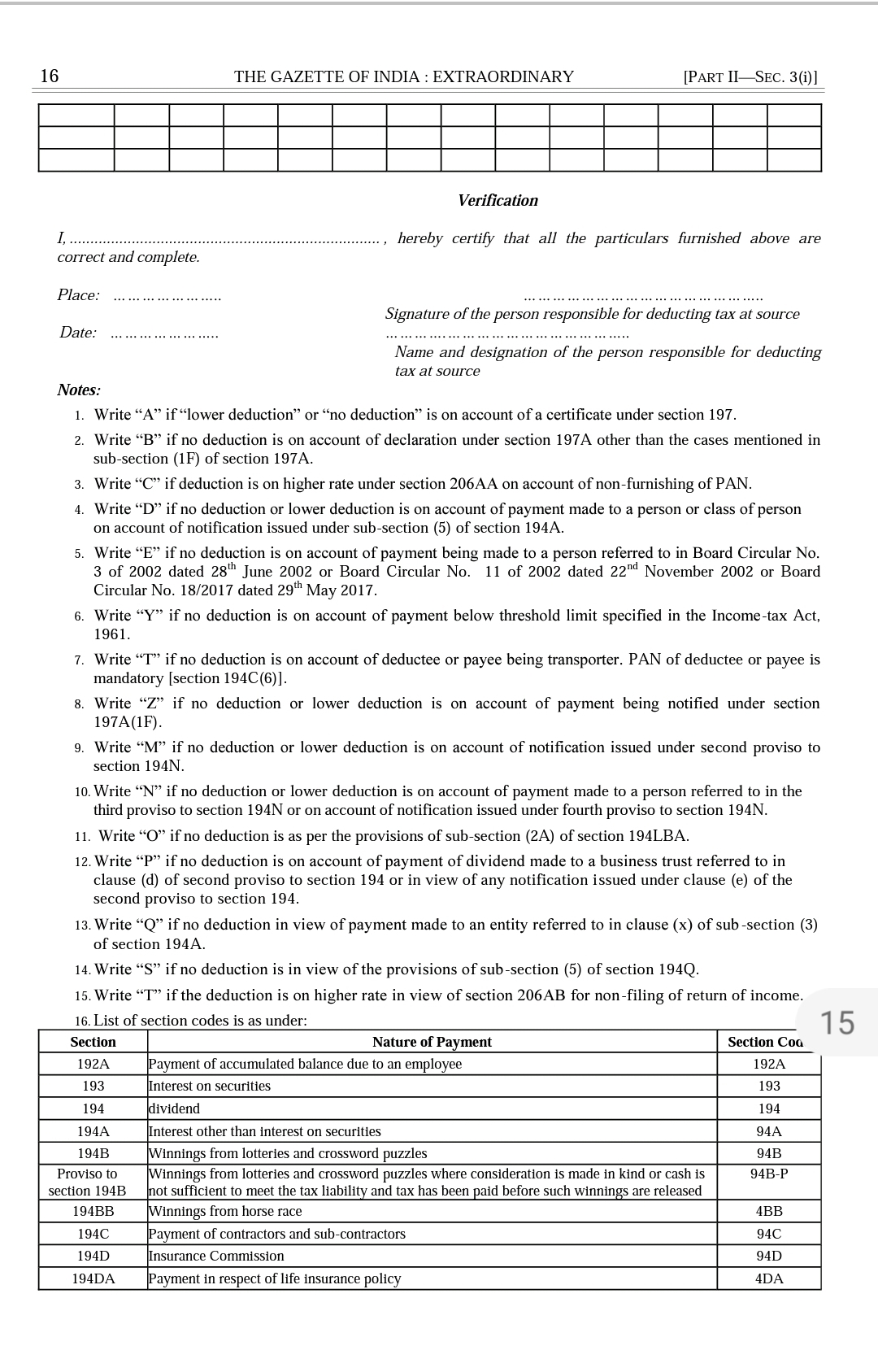

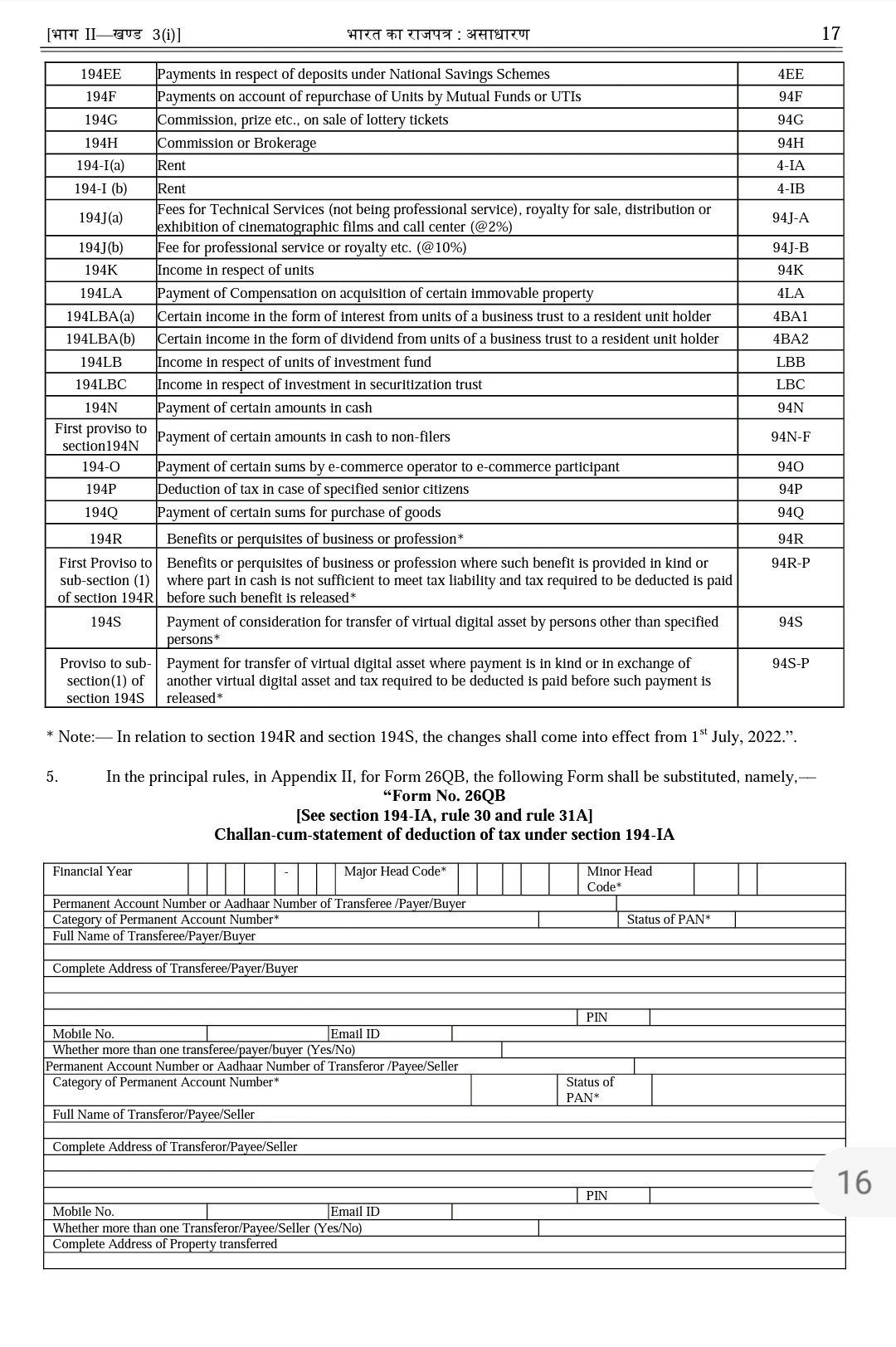

Finance Act 2022 inserted a new section 194S in the Income-tax Act, 1961 (hereinafter referred to as “the Act”) with effect from 1st July 2022.

The new section mandates a person, who is responsible for paying to any resident any sum by way of consideration for transfer of a virtual digital asset (VDA), to deduct an amount equal to 1% of such sum as income tax thereon. The tax deduction is required to be made at the time of credit of such sum to the account of the resident or at the time of payment, whichever is earlier.

This deduction is not required to be made in the following cases:-

(i) the consideration is payable by a specified person and the value or aggregate value of such consideration does not exceed fifty thousand rupees during the financial year; or

(ii) the consideration is payable by any person other than a specified person and the value or aggregate value of such consideration does not exceed ten thousand rupees during the financial year

The following are defined as specified person for the purposes of this provision:

(i) An individual or Hindu undivided family (HUF) who does not have any income under the head “profit and gains of business or profession”; and

(ii) An individual or HUF having income under the head “profits and gains of business or profession”, whose total sales/gross receipts/turnover from business carried on by him does not exceed one crore rupee or in case of profession exercised by him does not exceed fifty lakh rupee. This threshold is to be seen in the financial year immediately preceding the financial year in which the VDA is transferred.

Sub-section (6) of section 194S of the Act authorises Central Board of Direct Taxes (CBDT) to issue guidelines, for removal of difficulties, with the approval of the Central Government. These guidelines are required to be laid before each House of Parliament and are binding on the income-tax authorities and the person responsible for paying the consideration for transfer of VDA.

Accordingly, in exercise of the power conferred by sub-section (6) of section 194S of the Act, CBDT hereby issues the following guidelines. These guidelines will apply only in cases where transfer of VDA is taking place on or through an Exchange. In other cases (like peer to peer and others) provisions of section 194S of the Act shall apply and so far as these guidelines are concerned clarifications provided only in Question 6 shall apply.