FDI,ESOPs and off-market transactions approved by RBI, Sebi, a high court or Supreme Court and NCLAT will not face capital gains tax

In a significant decision, the Income-Tax Department has clarified about tax rules for capital gains tax made on certain equity investments in case no securities transactions tax (STT) has been paid, putting an end to the uncertainty that arose from the budget proposal relating to such transactions.

Foreign direct investment, employee stock option and off-market transactions that are recognised by RBI, Sebi, a high court or Supreme Court and NCLAT will not face capital gains tax, even if no securities transaction tax has been paid on them, the income tax department said.

The Central Board of Direct Taxes has notified a rule, introduced in the budget this year, providing for imposition of capital gains tax on acquisition of listed shares in off market transactions if STT is not paid, giving significant relief to genuine investments.

In the budget for FY18, the government had noted the misuse of exemption provided under section 10(38) to income from transfer of long term capital asset such as equities and mutual fund on which STT had been paid.

“With a view to prevent this abuse, it is proposed to amend section 10(38) to provide that exemption under this section for income arising on transfer of equity share acquired or on after 1st day of October, 2004 shall be available only if the acquisition of share is chargeable to Securities Transactions Tax under Chapter VII of the Finance (No 2) Act, 2004,” the budget had said.

However, this had unintended consequence of bringing to tax transactions such as ESOPs and FDI, which was not the intent of the provision. The clarification ensures these transactions will not be taxed

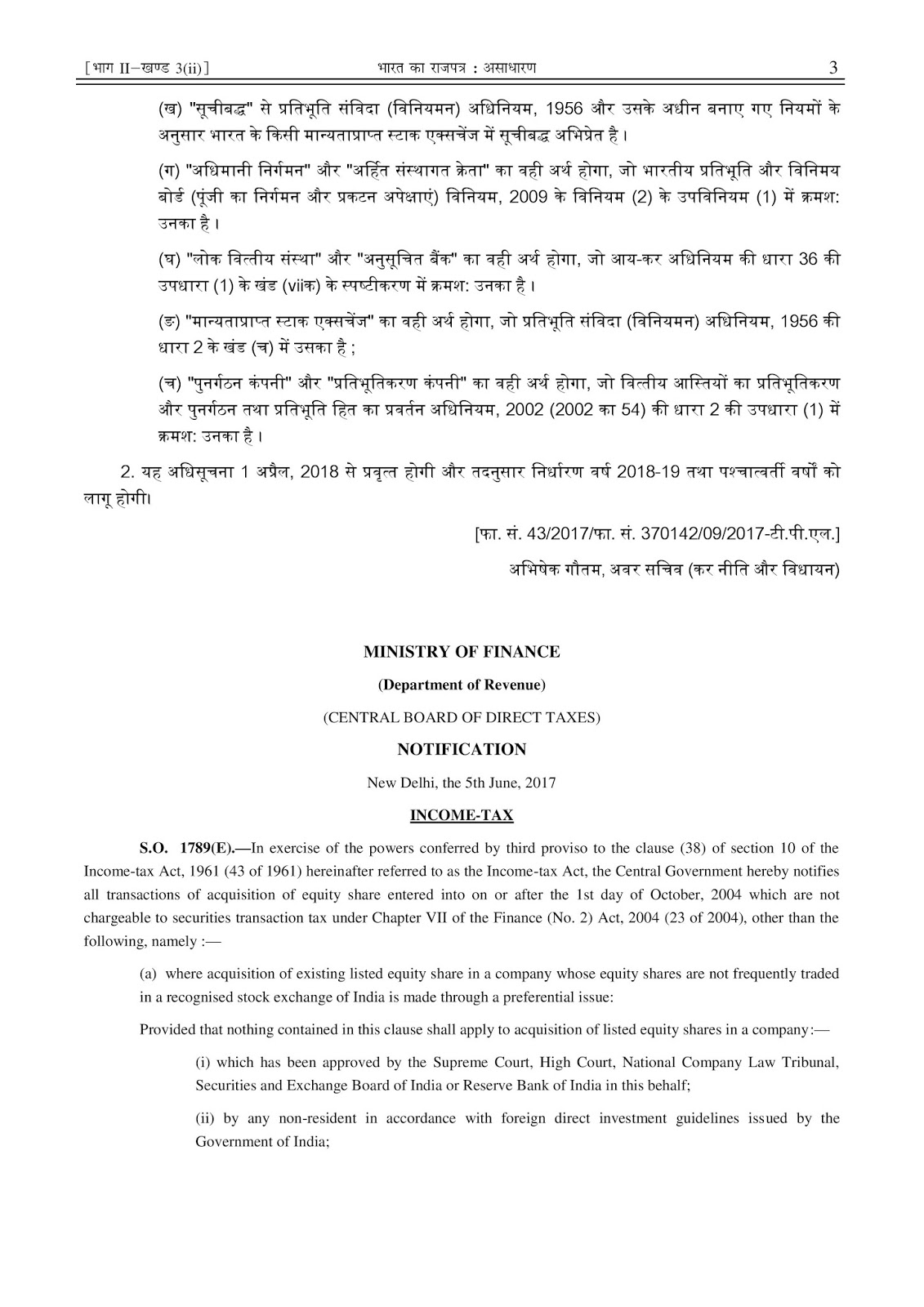

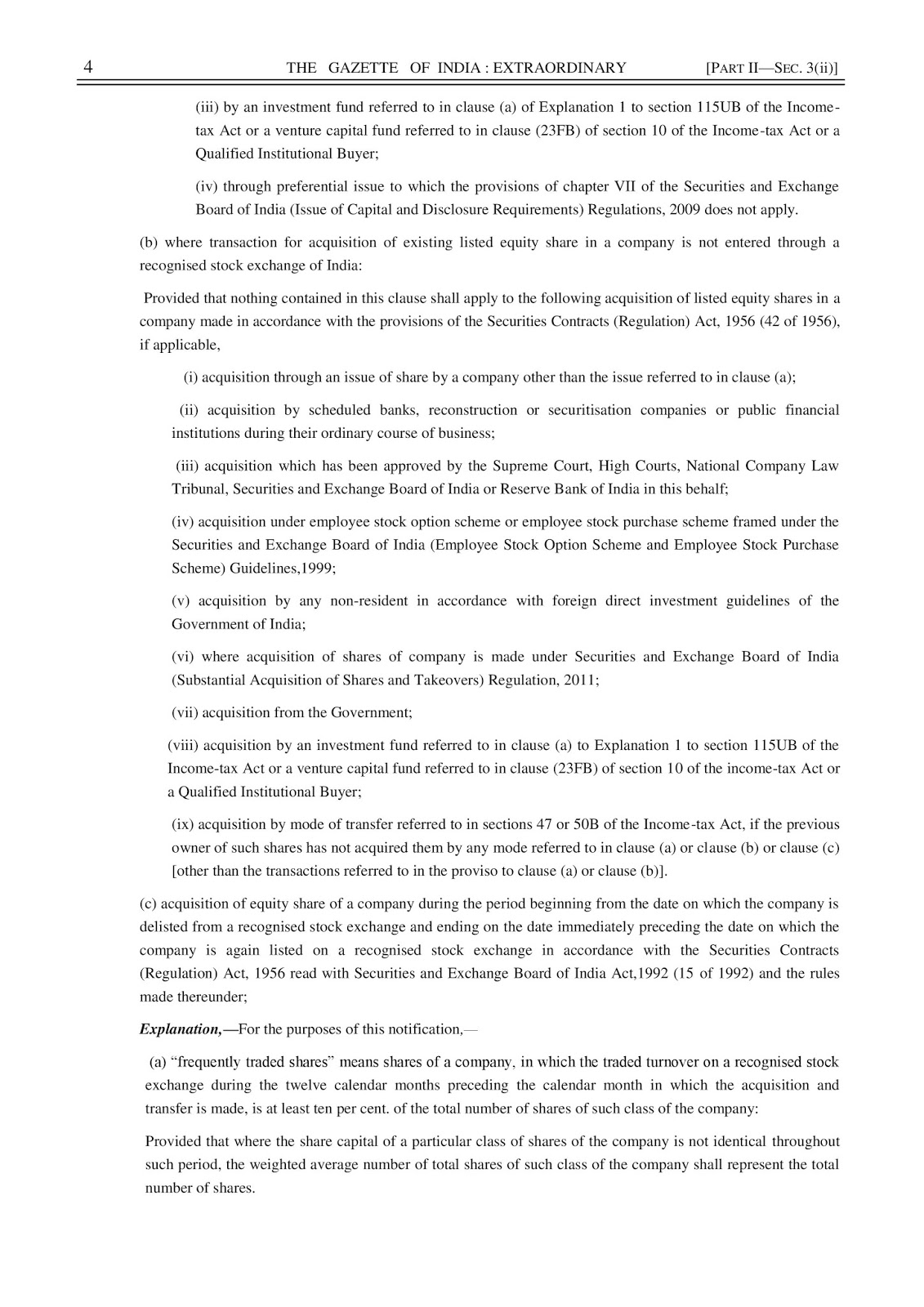

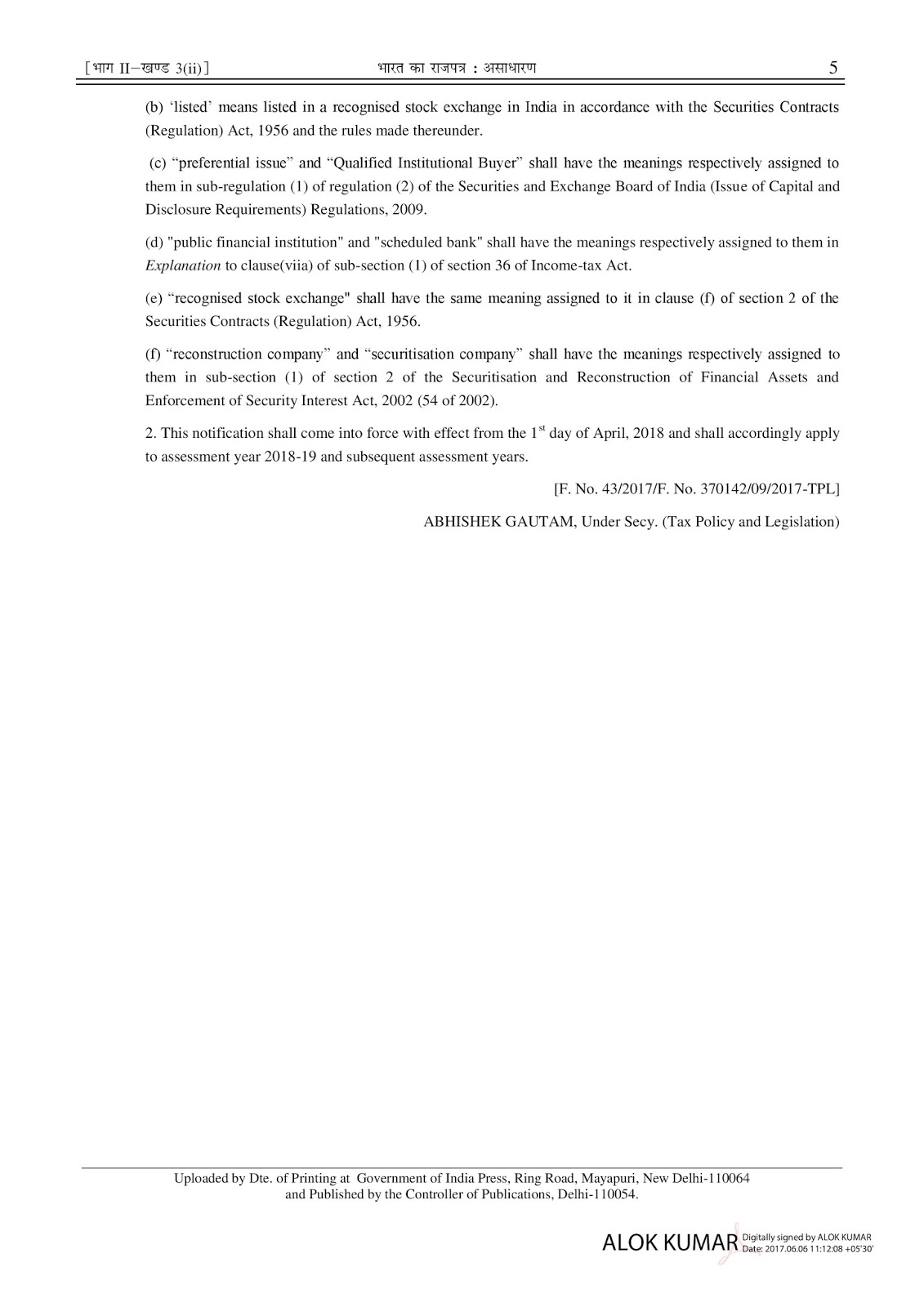

Refer Section 10(38) & CBDT notification dated 05 June 2017:

Section 10(38) of Income Tax Act,1961

Refer Section 10(38) & CBDT notification dated 05 June 2017:

Section 10(38) of Income Tax Act,1961

Incomes not included in total income.

10. In computing the total income of a previous year of any person, any income falling within any of the following clauses shall not be included—

|

(38)

|

any income arising from the transfer of a long-term capital asset, being an equity share in a company or a unit of an equity oriented fund [or a unit of a business trust] where—

|

|

(a)

|

the transaction of sale of such equity share or unit is entered into on or after the date on which Chapter VII of the Finance (No. 2) Act, 2004 comes into force; and

|

|

|

(b)

|

such transaction is chargeable to securities transaction tax under that Chapter :

|

|

[Provided that the income by way of long-term capital gain of a company shall be taken into account in computing the book profit and income-tax payable under section 115JB :]

|

||

|

[Provided also*that nothing contained in sub-clause (b) shall apply to a transaction undertaken on a recognised stock exchange located in any International Financial Services Centre and where the consideration for such transaction is paid or payable in foreign currency.]

|

||

|

Following third proviso shall be inserted after the second proviso to clause (38) of section 10 by the Finance Act, 2017, w.e.f. 1-4-2018 :

|

||

|

Provided also that nothing contained in this clause shall apply to any income arising from the transfer of a long-term capital asset, being an equity share in a company, if the transaction of acquisition, other than the acquisition notified by the Central Government in this behalf, of such equity share is entered into on or after the 1st day of October, 2004 and such transaction is not chargeable to securities transaction tax under Chapter VII of the Finance (No. 2) Act, 2004 (23 of 2004).

|

||

|

[Explanation.—For the purposes of this clause,—

|

|

(a)

|

“equity oriented fund” means a fund—

|

|

(i)

|

where the investible funds are invested by way of equity shares in domestic companies to the extent of more than sixty-five per cent of the total proceeds of such fund; and

|

|

|

(ii)

|

which has been set up under a scheme of a Mutual Fund specified under clause (23D):

|

|

Provided that the percentage of equity share holding of the fund shall be computed with reference to the annual average of the monthly averages of the opening and closing figures;

|

||

|

(b)

|

“International Financial Services Centre” shall have the same meaning as assigned to it in clause (q) of section 2 of the Special Economic Zones Act, 2005 (28 of 2005);

|

|

|

(c)

|

“recognised stock exchange” shall have the meaning assigned to it in clause (ii) of the Explanation 1 to *sub-section (5) of section 43;]

|

CBDT notification dated 05 June 2017

eToro is the ultimate forex broker for beginner and advanced traders.

LikeLike