Rule 6 [Intimation of receiving foreign contribution from relatives] – Any person receiving foreign contribution in excess of Rs. 10 lakhs [in place of Rs. 1 lakhs] or equivalent thereto in a financial year are required to report to the Central Government in Form FC-1 within 3 months [in place of 30 days] from the date of receipt of such contribution from relatives.

Rule 9 [Application for obtaining ‘registration’ or ‘prior permission’ to receive foreign contribution] – In clause (e) of sub-rule(1) & clause (e) of sub-rule(2), the person is required to intimate online in Form FC-6D in relation to bank accounts opened for utilising the foreign contribution received within 45 days [in place of 15 days] of the opening of any account.

Rule 13 [Declaration of receipt of foreign contribution] – Clause (b) relating to reporting of foreign contribution received by the person during the quarter in a financial year within 15 days from the end of the quarter has been omitted. Therefore, there is no requirement to furnish quarterly intimation in respect of foreign contribution received during the quarter.

Rule 17A [Change of designated bank account, name, address, aims, objectives or key members of the association] – Any person who has been granted certificate of registration or prior permission u/s 11 of the FCRA Act shall intimate the changes in designated bank account [Form FC-6C], bank for the purpose of utilisation [Form FC-6D], name [Form FC-6A], address, aims & objectives [Form FC-6B] or key members [Form FC-6E] within 45 days [in place of 15days] from such change.

Revision [Rule 20] – Any application for revision of an order passed by the competent authority u/s 32 of the Act shall be made in such form and manner, including in electronic form as may be specified by the Central Government [in place of plain paper].

At present, e-invoice is mandatory for businesses with an annual turnover of over Rs.20 crores.

government is planning to make GST e-invoicing mandatory for companies with a turnover of Rs 5 crore and above, thus bringing the threshold down from the current Rs 20 crore, according to a government official.

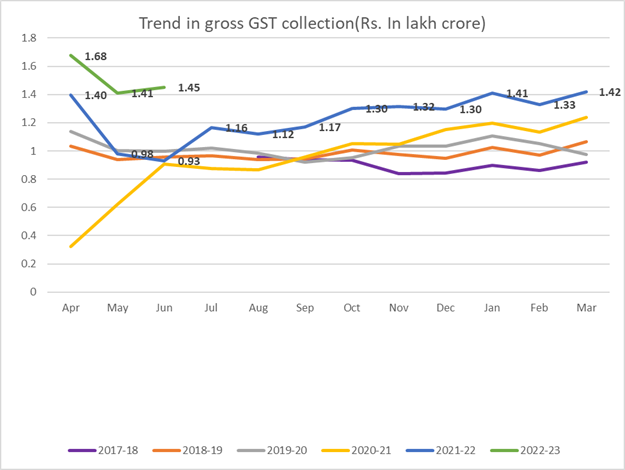

₹1,44,616 crore gross GST Revenue collection for June 2022; increase of 56% year-on-year

Gross GST collection in June 2022 is the second highest collection next to the April 2022 collection

GST collection crosses ₹1.40 lakh crore mark 5th time since inception of GST; 4th month at a stretch since March 2022

The gross GST revenue collected in the month of June 2022 is ₹144,616 crore of which CGST is ₹25,306 crore, SGST is ₹32,406 crore, IGST is ₹75887 crore (including ₹40102 crore collected on import of goods) and cess is ₹11,018 crore (including ₹ 1197 crore collected on import of goods). The gross GST collection in June 2022 is the second highest collection next to the April 2022 collection of ₹1,67,540 crore.

The government has settled ₹29,588 crore to CGST and ₹24,235 crore to SGST from IGST. In addition, Centre has also settled ₹27,000 crore of IGST on ad-hoc basis in the ratio of 50:50 between Centre and States/UTs in this month. The total revenue of Centre and the States in the month of June 2022 after regular and adhoc settlement is ₹68,394 crore for CGST and ₹70,141 crore for the SGST.

The revenues for the month of June 2022 are 56% higher than the GST revenues in the same month last year of ₹92,800 crore. During the month, revenues from import of goods was 55% higher and the revenues from domestic transaction (including import of services) are 56% higher than the revenues from these sources during the same month last year.

This is the fifth time the monthly GST collection crossed ₹1.40 lakh crore mark since inception of GST and fourth month at a stretch since March 2022. The collection in June’2022 is not only be the second highest but also has broken the trend of being low collection month as observed in the past. Total number of e-way bills generated in the month of May 2022 was 7.3 crore, which is 2% less than 7.4 crore e-way bills generated in the month of April 2022.

The average monthly gross GST collection for the first quarter of the FY 2022-23 has been ₹1.51 lakh crore against the average monthly collection of ₹1.10 lakh crore in the first quarter of the last Financial year showing an increase of 37%. Coupled with economic recovery, anti-evasion activities, especially action against fake billers have been contributing to the enhanced GST. The gross cess collection in this month is the highest since introduction of GST.

The chart below shows trends in monthly gross GST revenues since 2017-18. The table shows the state-wise figures of GST collected in each State during the month of June 2022 as compared to June 2021.

State-wise growth of GST Revenues during June 2022[1]

FCRA registration extended to later of 30.9.2022 or till disposal of renewal application where validity extended till 30 June or expiring from Jul-Sep. 2022.

E-filing of Updated ITR u/s 139(8A) has been enabled for AY 2020-21 and AY 2021-22 using Excel utility for ITR 1 and 4. Refer details in News section. Please click Downloads | Income Tax Department to access and download the same for clicking respective AY folder. Once Updated ITR is prepared, you can upload the XML/JSON by logging into Income-tax website.

E-filing of Updated ITR u/s 139(8A) has been enabled for AY 2020-21 & AY 2021-22 I Update 27-06-2022

Company Law Adjudication & Appeal Updates -24 June 2022

Bangalore ROC Penalty order for violation of Section 170 of the Companies Act 2013 in the matter of Landomus Realty Pvt. Ltd.

👉 Default

One of the Directors has signed the documents as a capacity of Chairman & CEO during the course of inquiry u/s 206 of the Companies Act 2013. But as per records no resolution has been passed appointing him CEO by the Company or the board.

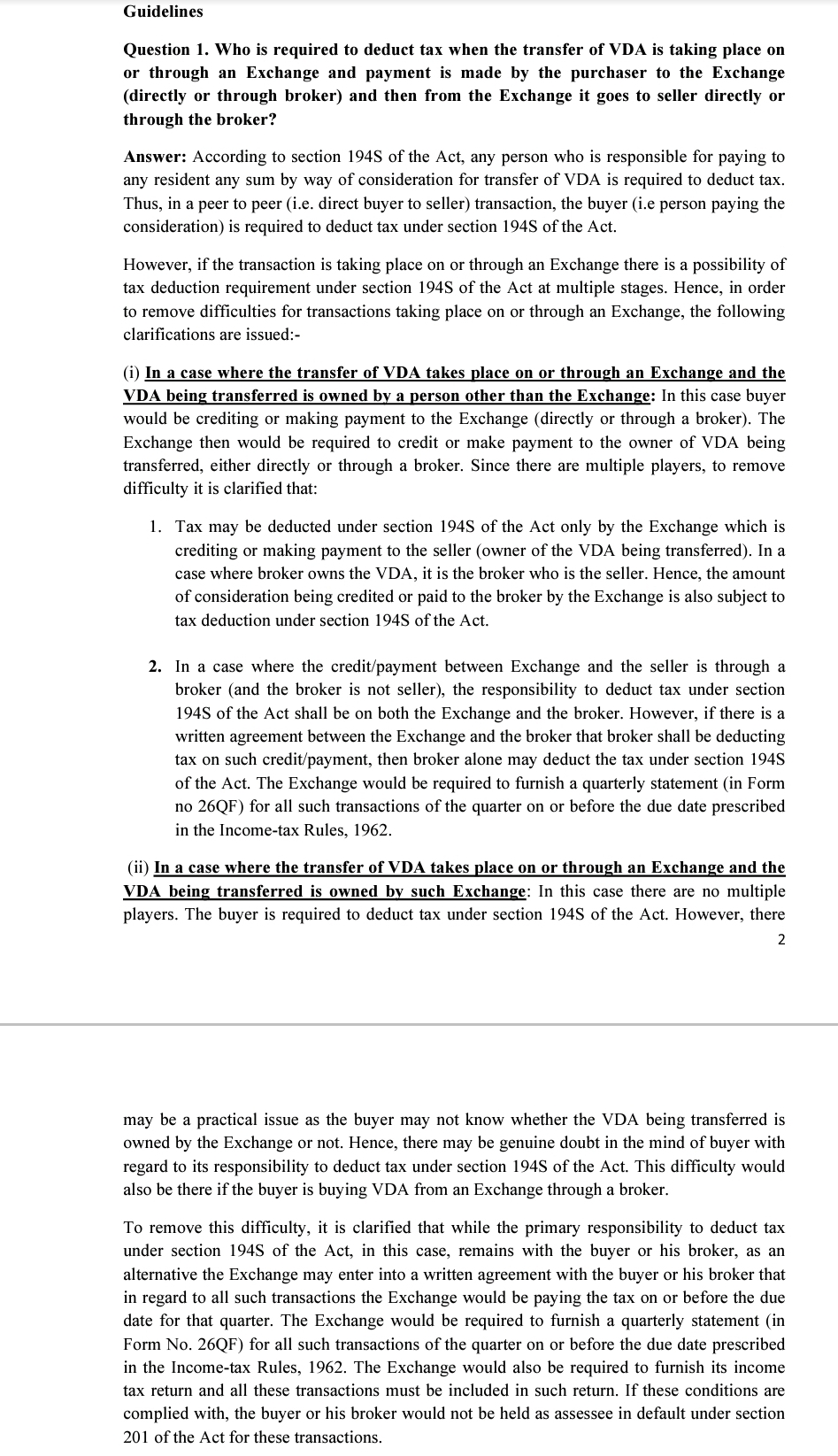

Finance Act 2022 inserted a new section 194S in the Income-tax Act, 1961 (hereinafter referred to as “the Act”) with effect from 1st July 2022.

The new section mandates a person, who is responsible for paying to any resident any sum by way of consideration for transfer of a virtual digital asset (VDA), to deduct an amount equal to 1% of such sum as income tax thereon. The tax deduction is required to be made at the time of credit of such sum to the account of the resident or at the time of payment, whichever is earlier.

This deduction is not required to be made in the following cases:-

(i) the consideration is payable by a specified person and the value or aggregate value of such consideration does not exceed fifty thousand rupees during the financial year; or

(ii) the consideration is payable by any person other than a specified person and the value or aggregate value of such consideration does not exceed ten thousand rupees during the financial year

The following are defined as specified person for the purposes of this provision:

(i) An individual or Hindu undivided family (HUF) who does not have any income under the head “profit and gains of business or profession”; and

(ii) An individual or HUF having income under the head “profits and gains of business or profession”, whose total sales/gross receipts/turnover from business carried on by him does not exceed one crore rupee or in case of profession exercised by him does not exceed fifty lakh rupee. This threshold is to be seen in the financial year immediately preceding the financial year in which the VDA is transferred.

Sub-section (6) of section 194S of the Act authorises Central Board of Direct Taxes (CBDT) to issue guidelines, for removal of difficulties, with the approval of the Central Government. These guidelines are required to be laid before each House of Parliament and are binding on the income-tax authorities and the person responsible for paying the consideration for transfer of VDA.

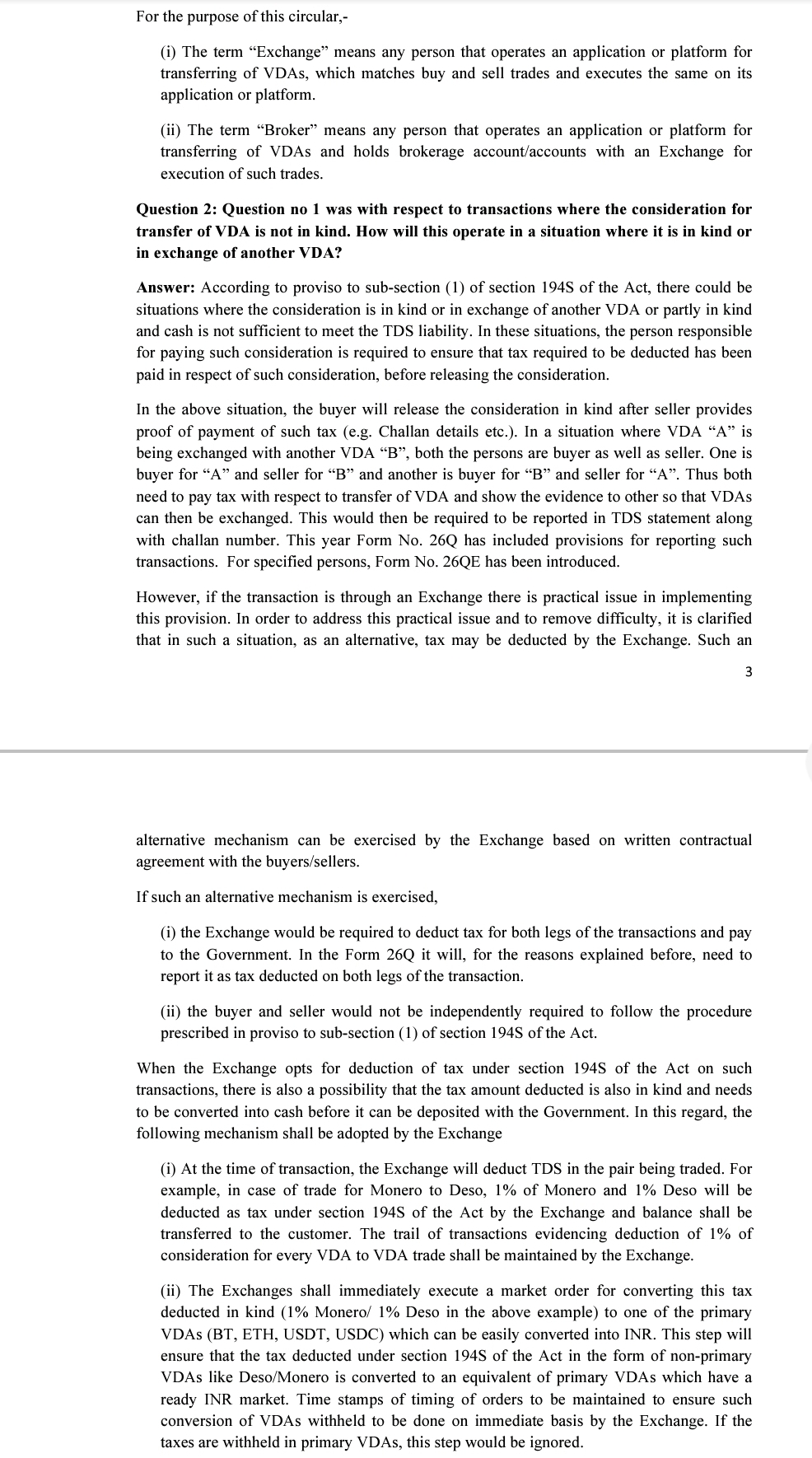

Accordingly, in exercise of the power conferred by sub-section (6) of section 194S of the Act, CBDT hereby issues the following guidelines. These guidelines will apply only in cases where transfer of VDA is taking place on or through an Exchange. In other cases (like peer to peer and others) provisions of section 194S of the Act shall apply and so far as these guidelines are concerned clarifications provided only in Question 6 shall apply.

Income Tax Department carried out search and seizure operations on 16.06.2022 on a business group involved in retail and export sale of handicrafts, cash financing, purchase and sale of land and buildings, alongwith some bullion traders. The search operation covered more than 25 premises spread across Rajasthan and Mumbai.

During the course of the search operation, several incriminating documents have been found and seized. The perusal of seized evidences indicates that the group has indulged in unaccounted cash transactions in real estate business as well as obtaining bogus purchase bills. The modus operandi of the group has been to suppress profits of the handicrafts business by inflating the purchases in the books of account, through bogus bills of gold and silver arranged from bullion traders. During the search, it has also been seen that cash has been received back against the cheques issued to these bullion traders.

Cash was found to be utilised for investment in real estate as well as for obtaining cheques to be introduced as credits into the books of account. The seized evidence also revealed that the group recently acquired few shell companies through entry operators.

The search action has led to seizure of unaccounted cash exceeding Rs. 1.30 crore and unaccounted gold jewellery exceeding Rs. 7.90 crore. Prima facie, estimated unaccounted income in excess of Rs. 100 crore has been unearthed, so far.

Finance Act 2022 inserted a new section 194R in the Income-tax Act, 1961 (hereinafter referred to as “the Act”) w.e.f. 01st July 2022. The new section mandates a person, who is responsible for providing any benefit or perquisite to a resident, to deduct tax at source @10% of the value or aggregate of value of such benefit or perquisite, before providing such benefit or perquisite.

The benefit or perquisite may or may not be convertible into money but should arise either from carrying out of business, or from exercising a profession, by such resident.

This deduction is not required to be made, if the value or aggregate of value of the benefit or perquisite provided or likely to be provided to the resident during the financial year does not exceed twenty thousand rupees.

The responsibility of tax deduction also does not apply to a person, being an Individual/Hindu undivided family (HUF) deductor, whose total sales / gross receipts / gross turnover from business does not exceed one crore rupees, or from profession does not exceed fifty lakh rupees, during the financial year immediately preceding the financial year in which such benefit or perquisite is provided by him.

CBDT Circular No. 12 of 2022 dated 16th June 2022

Clarification 1:

Question 1. Is it necessary that the person providing benefit or perquisite needs to check if the amount is taxable under clause (iv) of section 28 of the Act, before deducting tax under section 194R of the Act?

Section 28 The following income shall be chargeable to income-tax under the head “Profits and gains of business or profession”, (iv) the value of any benefit or perquisite, whether convertible into money or not, arising from business or the exercise of a profession ;

Answer: No. The deductor is not required to check whether the amount of benefit or perquisite that he is providing would be taxable in the hands of the recipient under clause (iv) of section 28 of the Act.

The amount could be taxable under any other section like section 41(1) etc.

Section 194R of the Act casts an obligation on the person responsible for providing any benefit or perquisite to a resident, to deduct tax at source @10%.

There is no further requirement to check whether the amount is taxable in the hands of the recipient or under which section it is taxable.

In this regard it may be highlighted that in the context of section 195 of the Act it is a requirement to know whether the payment made by the deductor is income in the hands of the non-resident recipient as section 195 of the Act requires deduction on any other sum chargeable under the provisions of this Act at the rates in force. Thus there is requirement that deductor needs to verify if the “sum is chargeable under the Income-tax Act”. The term “rate in force” is defined in clause (37A) of section 2 of the Act and it allows benefit of agreement under section 90 or section 90A of the Act, if eligible, in determining the rate of tax at which the tax is to be deducted at source.

Hence, there is further requirement of checking if the amount is taxable under tax treaty and if yes, at what rate.

Such a requirement is not there in section 194R of the Act, in the absence of these two terms in this section.

Hence, there is no requirement for deductor to verify whether the amount is taxable in the hands of the recipient or section under which it is taxable.

It may also be highlighted that these two terms are also not there in section 194E (Section 194E TDS on Payments to Non-Resident Sportsmen or Sports Association ) of the Act and Hon’ble Supreme Court in the case of PILCOM vs. CIT West Bengal (Civil Appeal No. 5749 of 2012), held that tax is to be deducted under section 194E of the Act at a specific rate indicated there in and there is no need to see the taxability or the rate of taxability in the hands of the non-resident.

Clarification 2:

Question 2. Is it necessary that the benefit or perquisite must be in kind for section 194R of the Act to operate?

Answer: Tax under section 194R of the Act is required to be deducted whether the benefit or perquisite is in cash or in kind.

In this regard it is important to draw attention to the first proviso to sub-section (1) of section 194R of the Act, which reads as under:

“Provided that in a case where the benefit or perquisite, as the case may be, is wholly in kind or partly in cash and partly in kind but such part in cash is not sufficient to meet the liability of deduction of tax in respect of whole of such benefit or perquisite, the person responsible for providing such benefit or perquisite shall, before releasing the benefit or perquisite, ensure that tax required to be deducted has been paid in respect of the benefit or perquisite:”

This proviso clearly indicates the intent of legislature that there could also be situations where benefit or perquisite is in cash or the benefit or perquisite is in kind or partly in cash and partly in kind.

Thus, section 194R of the Act clearly brings in its scope the situation where the benefit or perquisite is in cash or in kind or partly in cash or partly in kind.

Clarification 3:

Question 3. Is there any requirement to deduct tax under section 194R of the Act, when the benefit or perquisite is in the form of capital asset?

Answer: As has been stated in response to question no 1, there is no requirement to check whether the perquisite or benefit is taxable in the hands of the recipient and the section under which it is taxable.

Further, courts have held many benefits or perquisites to be taxable even though one can argue that they are in the nature of capital asset.

The following judgments illustrate this point:

Assessee entered into an agreement with `.1′ for purchase of a plot of land and certain amount was paid as earnest money. However, possession of land was not given to assessee and seller entered into another agreement with a third party to develop the said plot. Assessee filed suit in which a consent decree was passed and in pursuance of same certain amount as paid to assessee. On appeal it was held that such sum received in pursuance of consent decree was liable to tax as business income under section 28(iv). Ramesh Babulal Shah v CIT (2015) 53 taxmann.com 277 (Born)

The amount representing principal loan waived by bank under one time settlement scheme would constitute income falling under section 28(iv) relating to value of any benefit or perquisite, arising from business or exercise of profession. CIT v Rainaniyam Homes (P) Ltd (2016) 68 taxmann.com 289 (Mad)

Value of rent free accommodation, furniture and fixtures given to director was held as taxable under section 28(iv). CIT v Subrata Roy (2016) 385ITR 547 (All)

Where a car was given to an assessee by his disciple, who had been benefited from his preaching, the value of car was held to be taxable in the hands of the assessee being a receipt from the exercise of the vocation carried on by him. CIT (Addl) v Rain Kripal Tripathi (1980) 125 ITR 408 (All)

The assessee was a director of a company. In terms of an agreement with the promoters, shares were allotted to the director. On these facts, it was held that the shares received by the director were benefit or perquisite received from a company by the director and it was a benefit assessable to tax. D. M. Neterwala v CIT (1986) 122 ITR 880 (Born)

Value of gift of land was held as a receipt by the assessee in carrying on of his vocation and was held as taxable. Amarendra Nath Chakraborty v CIT (1971) 79 ITR 342 (Cal)

Thus, it can be seen that the asset given as benefit or perquisite may be capital asset in general sense of the term like car, land etc but in the hands of the recipient it is benefit or perquisite and has accordingly been held to be taxable. In any case, as stated earlier, the deductor is not required to check if the benefit or perquisite is taxable in the hands of recipient. Thus, the deductor is required to deduct tax under section 194R of the Act in all cases where benefit or perquisite (of whatever nature) is provided.

Clarification 4:

Question 4: Whether sales discount, cash discount and rebates are benefit or perquisite?

Answer: Sales discounts, cash discount or rebates allowed to customers from the listed retail price represent lesser realization of the sale price itself. To that extent purchase price of customer is also reduced.

Logically these are also benefits though related to sales/purchase. Since TDS under section 194R of the Act is applicable on all forms of benefit/perquisite, tax is required to be deducted. However, it is seen that subjecting these to tax deduction would put seller to difficulty.

To remove such difficulty it is clarified that no tax is required to be deducted under section 194R of the Act on sales discount, cash discount and rebates allowed to customers.

Clarification 5:

Question 5. How is the valuation of benefit/perquisite required to be carried out?

Answer: The valuation would be based on fair market value of the benefit or perquisite except in following cases:-

The benefit/perquisite provider has purchased the benefit/perquisite before providing it to the recipient. In that case the purchase price shall be the value for such benefit/perquisite.

The benefit/perquisite provider manufactures such items given as benefit/perquisite, then the price that it charges to its customers for such items shall be the value for such benefit/perquisite. It is further clarified that GST will not be included for the purposes of valuation of benefit/perquisite for TDS under section 194R of the Act.

Clarification 6:

Question 6: Many a times, a social media influencer is given a product of a manufacturing company so that he can use that product and make audio/video to speak about that product in social media. Is this product given to such influencer a benefit or perquisite?

Answer: Whether this is benefit or perquisite will depend upon the facts of the case. In case of benefit or perquisite being a product like car, mobile, outfit, cosmetics etc and if the product is returned to the manufacturing company after using for the purpose of rendering service, then it will not be treated as a benefit/perquisite for the purposes of section 194R of the Act. However, if the product is retained then it will be in the nature of benefit/perquisite and tax is required to be deducted accordingly under section 194R of the Act.

Question 7: Whether reimbursement of out of pocket expense incurred by service provider in the course of rendering service is benefit/perquisite?

Answer: Any expenditure which is the liability of a person carrying out business or profession, if met by the other person is in effect benefit/perquisite provided by the second person to the first person in the course of business/profession.

Let us assume that a consultant is rendering service to a person “X” for which he is receiving consultancy fee. In the course of rendering that service, he has to travel to different city from the place where is regularly carrying on business or profession. For this purpose, he pays for boarding and lodging expense incurred exclusively for the purposes of rendering the service to “X”. Ordinarily, the expenditure incurred by the consultant is part of his business expenditure which is deductible from the fee that he receives from company “X”. In such a case, the fee received by the consultant is his income and the expenditure incurred on travel is his expenditure deductible from such income in computing his total income. Now if this travel expenditure is met by the company “X”, it is benefit or perquisite provided by “X” to the consultant.

However, sometimes the invoice is obtained in the name of “X” and accordingly, if paid by the consultant, is reimbursed by “X”. In this case, since the expense paid by the consultant (for which reimbursement is made) is incurred wholly and exclusively for the purposes of rendering services to “X” and the invoice is in the name of “X”, then the reimbursement made by “X” being the service recipient will not be considered as benefit/perquisite for the purposes of section 194R of the Act.

If the invoice is not in the name of “X” and the payment is made by “X” directly or reimbursed, it is the benefit/perquisite provided by “X” to the consultant for which deduction is required to be made under section 194R of the Act.

Question 8: If there is a dealer conference to educate the dealers about the products of the company – Is it benefit/perquisite?

Answer: The expenditure pertaining to deafer/business conference would not be considered as benefit/perquisite for the purposes of section 194R of the Act in a case where dealer/business conference is held with the prime object to educate dealers/customers about any of the following or similar aspects:

new product being launched

discussion as to how the product is better than others

obtaining orders from dealers/customers

teaching sales techniques to dealers/customers

addressing queries of the dealers/customers

reconciliation of accounts with dealers/customers

However, such conference must not be in the nature of incentives/benefits to select dealers/customers who have achieved particular targets.

Further, in the following cases the expenditure would be considered as benefit or perquisite for the purposes of section 194R of the Act:-

Expense attributable to leisure trip or leisure component, even if it is incidental to the dealer/business conference.

Expenditure incurred for family members accompanying the person attending dealer/business conference

Expenditure on participants of dealer/business conference for days which are on account of prior stay or overstay beyond the dates of such conference.

Question 9: Section 194R provides that if the benefit/perquisite is in kind or partly in kind (and cash is not sufficient to meet TDS) then the person responsible for providing such benefit or perquisite is required to ensure that tax required to be deducted has been paid in respect of the benefit or perquisite, before releasing the benefit or perquisite. How can such person be satisfied that tax has been deposited?

Answer: The requirement of law is that if a person is providing benefit in kind to a recipient and tax is required to be deducted under section 194R of the Act, the person is required to ensure that tax required to be deducted has been paid by the recipient. Such recipient would pay tax in the form of advance tax. The tax deductor may rely on a declaration along with a copy of the advance tax payment challan provided by the recipient confirming that the tax required to be deducted on the benefit/perquisite has been deposited. This would be then required to be reported in TDS return along with challan number. This year Form 26Q has included provisions for reporting such transactions.

In the alternative, as an option to remove difficulty if any, the benefit provider may deduct the tax under section 194R of the Act and pay to the Government. The tax should be deducted after taking into account the fact the tax paid by him as TDS is also a benefit under section 194R of the Act. In the Form 26Q he will need to show it as tax deducted on benefit provided.

Question 10. Section 194R would come into effect from the 1St July 2022. Second proviso to subsection (1) of section 194R of the Act provides that the provision of this section does not apply where the value or aggregate of value of the benefit or perquisite provided or likely to be provided to a resident during the financial year does not exceed twenty thousand rupees. It is not clear how this limit of twenty thousand is to be computed for the Financial Year 2022-23?

Answer: It is hereby clarified that,-

Since the threshold of twenty thousand rupees is with respect to the financial year, calculation of value or aggregate of value of the benefit or perquisite triggering deduction under section 194R of the Act shall be counted from 1st April, 2022. Hence, if the value or aggregate value of the benefit or perquisite provided or likely to be provided to a resident exceeds twenty thousand rupees during the financial year 2022-23 (including the period up to 30th June 2022), the provision of section 194R shall apply on any benefit or perquisite provided on or after July 2022.

The benefit or perquisite which has been provided on or before 30th June 2022, would not be subjected to tax deduction under section 194R of the Act.

Is all type of benefits or perquisites taxable now? I Newly inserted Section 194R of Income Tax Act, 1961 (W.e.f. 01st July 2022)

✒️ Section 194 R –An Introduction (w.e.f. 01st July 2022)

✒️ Whether deductor is required to be check taxability of Benefits/perquisites in the hands of recipient?

✒️ Is Section 194 R apply on Capital asset provided as Benefits/perquisites ?

✒️ Whether sales discount, cash discount and rebates are benefit or perquisite?

✒️ How is the valuation of benefit/perquisite required to be carried out?

✒️ Whether reimbursement of out of pocket expense incurred by service provider in the course of rendering service is benefit/perquisite?

✒️ Threshold limit for FY 2022-23-How to check for applicability

✒️ TDS deposit & compliances in case of benefits or perquisites provided in Kind