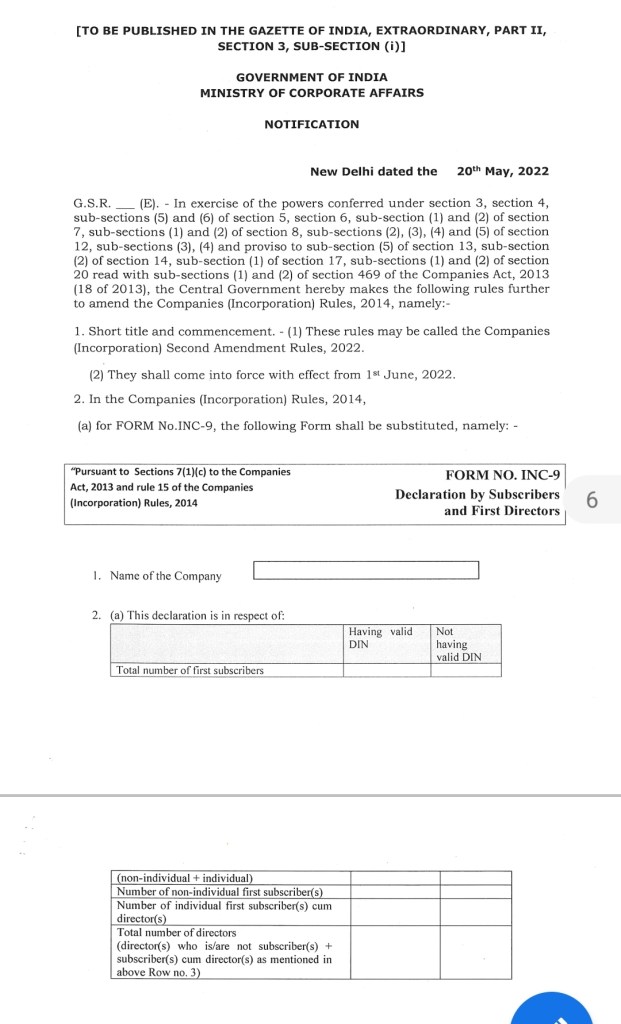

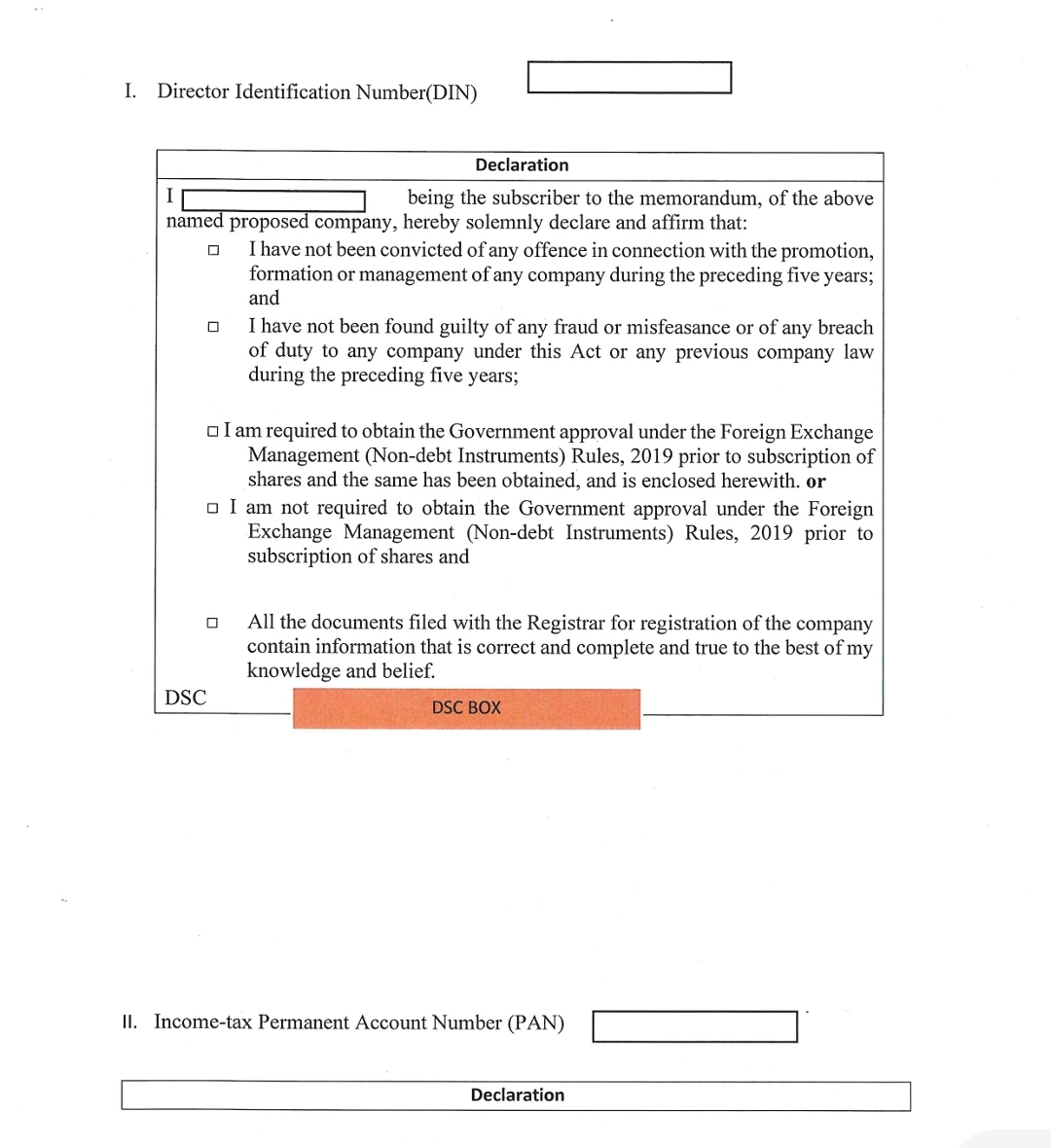

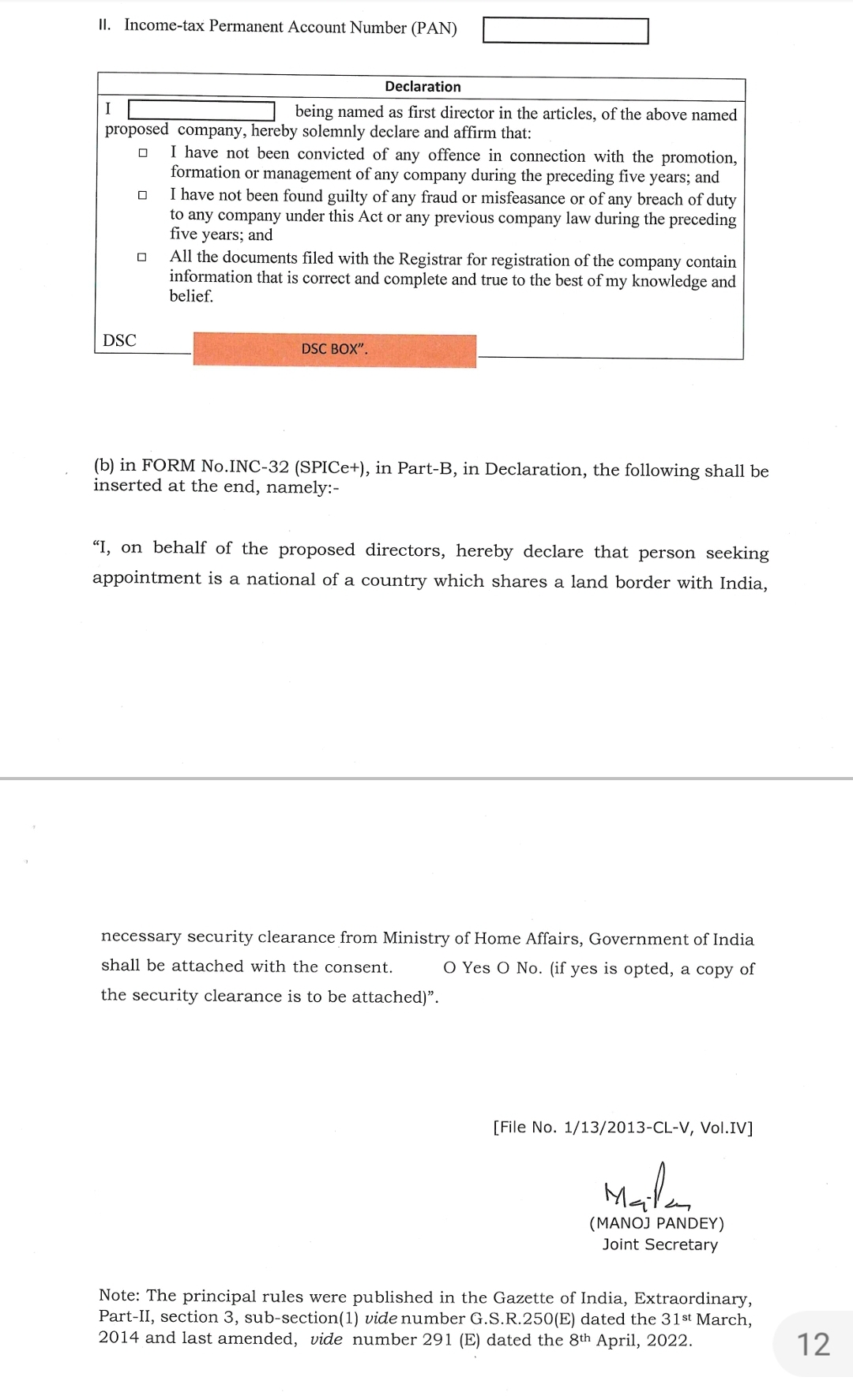

MCA has issued Companies (Incorporation) 2nd Amendment Rules, 2022.

They shall come into force w.e.f. 01/06/2022.

Refer MCA Notification dated 20 May 2022:

Simplifying your business ideas, structures, functionalities, relations & operations

MCA has issued Companies (Incorporation) 2nd Amendment Rules, 2022.

They shall come into force w.e.f. 01/06/2022.

Refer MCA Notification dated 20 May 2022:

The Directorate General of GST Intelligence (DGGI) Gurugram Zonal Unit (GZU), Haryana has detected a case wherein total ITC of more than Rs 160 crore has been utilized and passed on by network of nonexistent & fake firms in tandem with various existing entities / merchants / wholesalers.

Based on intelligence which was analyzed & acted upon by the Gurugram Zonal Unit, it emerged that a merchant, who is an importer and wholesale trader of dry fruits has availed IGST Input Tax Credit on imports, but has further issued duty paid invoices to various non-existent firms, whereas the goods (dry fruits) were sold in the open market to various retailers. Quiet a few of the firms, to whom invoices were issued were found to be non-existent / fake (registered on GST portal under different HSN), who further issued goodless invoices to fraudulently pass on ITC without supply of any goods. The merchant has rendered itself to liable under Section 122 (i) (ii) of the CGST Act, 2017, etc., as a Consequence of which the merchant has deposited Rs. 5 crore till date, additional recovery in this matter is expected.

In all, 10 such fake firms busted so far in the investigation, have fraudulently availed & passed on Input Tax Credit (ITC) in excess of Rs. 160 crore, bases on inwards from the merchant, and from other fake/cancelled sources, which is under further investigation. Controller of one such firm to whom duty paid invoices were issued without supply of actual goods by the merchant, prima facie passed on fraudulent ITC of Rs. 26.3 crore, was identified as Sh. Pawan Kumar Sharma. It emerged through investigation that Sh. Pawan Kumar Sharma is also proprietor of another firm M/s Pawan Traders also involved in passing on fraudulent Input Tax Credit (ITC).

Accordingly, Shri Pawan Kumar Sharma was arrested on 13.05.2022 under the provisions of Section 69 of CGST Act, 2017 read with clause (b) (c) of subsection (1) of section 132 of CGST Act, 2017 and produced before CMM, Patiala House Court on 13.05.2022, who ordered judicial custody for 14 days.

Further investigations in the matter is under progress.

Dear Sir,

Please find below YouTube video link on *Super 10 Tax Saving Tips*

https://youtu.be/DpCXOuDG7Io

*Super 10 Tax Saving Tips*

✒️ *Paying rent to parents*

✒️ *Invest in wife’s name*

✒️ *Investment through HUF*

✒️ *Utilise exemption for senior citizens*

✒️ *Invest in name of adult child*

✒️ *Invest in NPS*

✒️ *Tax Harvesting*

✒️ *Car Hire*

✒️ *Accommodation lease*

✒️ *Save tax of Rs. 12,500 by small donation 80G/80GGA (For Small taxpayer, Taxable income above 5 Lakhs to 5.125 Lakhs )*

Regards,

Bipul Kumar

CBDT Circular No. 10 of 2022 dated May 17, 2022

Subject; Circular regarding use of functionality under section 206AB and 206CCA of the Income-tax Act, 1961 – reg.

1. Finance Act, 2021 inserted two new sections 206AB and 206CCA in the Income-tax Act 1961 (hereinafter referred to as “the Act”) which took effect from 1st day of July 2021. These sections (as they stood prior to its amendment by the Finance Act 2022) mandated tax deduction (section 206AB) or tax collection (section 206CCA) at higher rate in case of certain non-filers (specified persons) with respect to tax deductions (other than under sections 192, 192A, 194B, 194BB, 194LBC and 194N) and tax collections. Higher rate was twice the prescribed rate or 5%, whichever is higher. Specified person meant a person who satisfies both the following conditions: –

(i) He has not filed the returns of income for both of the two assessment years relevant to the two previous years immediately before the previous year in which tax is required to be deducted/collected. Two previous years to be counted are required to be those whose return filing date under sub-section (1) of section 139 has expired.

(ii) Aggregate of tax deducted at source and tax collected at source is rupees fifty thousand or more in each of these two previous years.

2. It can be seen that the tax deductor or the tax collector was required to do a due diligence of satisfying himself if the deductee or the collectee was a specified person? In order to ease this compliance burden the Income-tax Department came out with functionality “Compliance Check for Section 206AB & 206CCA”, which was made available through reporting portal of the Income-tax Department. It enabled the tax deductor or the collector to feed the single PAN (PAN search) or multiple PANs (bulk search) of the deductee or collectee. The functionality then gave a response if such deductee or collectee was a specified person. For PAN Search, response was visible on the screen which could be downloaded in the PDF format. For Bulk Search, response was in the form of downloadable file which could be kept for record. The’ logic of this functionality was explained through paragraph 3 of circular no 11 dated 21st June 2021.

(a) He has not furnished the return of income for the assessment year relevant to the previous year immediately preceding the financial year in which tax is required to be deducted/collected. The previous year to be counted is required to be the one whose return filing date under sub-section (I) of section 139 has expired.

(b) Aggregate of tax deducted at source and tax collected at source is rupees fifty thousand or more in that previous year.

(iii) Further, it has been provided that provisions of section 206AB will not apply in case of deduction of tax on transfer of virtual digital asset (VDA) under section 194S of the Act to a person being an individual or Hindu undivided family, whose sales, gross receipts or turnover from the business carried on by him or profession exercised by him does not exceed one crore rupees in case of business or fifty lakh rupees in case of profession, during the financial year immediately preceding the financial year in which such VDA is transferred or if such person does not have any income under the head “Profit and gains of business or profession”.

4. Thus it can be seen that now a person can become a specified person for default in one year instead of earlier provision of default in two years. Accordingly the logic of the functionality has been amended. The new logic for the current financial year is as under:

– A list of specified persons is prepared as on the start of the financial year 2022-23. taking previous year 2020-21 as the relevant previous year. List contains names of the taxpayers who did not file return of income for the assessment year 2021 -22 and have aggregate of TDS and TCS of fifty thousand rupees or more in the previous year 2020-21.

– During the financial year 2022-23. no new names are added in the list of specified persons. This is a taxpayer friendly measure to reduce the burden on tax deductor and collector of checking PANs of non-specified person more than once during the financial year.

– If any specified person files a valid return of income (filed & verified) for the assessment year 2021-22 during the financial year 2022-23, his name would be removed from the list of specified persons. This would be done on the date of filing of the valid return of income during the financial year 2022-23.

– If any specified person files a valid return of income (filed & verified) for the assessment year 2022-23, his name would be removed from the list of specified persons. This would be done on the due date for filing of the return of income for AY 2022-23 or on the date of actual tiling of valid return (filed & verified), whichever is later.

– If the aggregate of TDS and TCS. in the case of a specified person, in the previous year 2021-22 is less than fifty thousand rupees, his name would be removed from the list of specified persons. This would be done on the first due date under sub-section (I) of section 139 of the Act falling in the financial year 2022-23. For the financial year 2022-23 this due date is 31st July 2022.

– Belated and revised TCS & TDS returns of the relevant financial year filed during the financial year 2022-23 would also be considered for removing persons from the list of specified persons on a regular basis.

5. The deductor or the collector may check the PAN in the functionality at the beginning of the financial year and then he is not required to check the PAN of non-specified person during that financial year. To illustrate, let us assume that a deductor has 10.000 vendors that he deals with. He can use the functionality in the bulk search mode and can get the result of all these 10.000 PANs at one go. Let us assume that the functionality has shown that out of these 10.000 PANs, 5 PANs are specified persons for the purposes of sections 206AB and 206CCA of the Act. Now with respect of the remaining 9,995 PANs, it is clear that they are not in the list of specified persons for that financial year. Since no new name would be added in the list of specified persons during the financial year, the deductor can be assured that these 9,995 PANs would remain outside the list of specified persons during that financial year. Thus, deductor need not check again with respect to these 9,995 PANs during that financial year. There are chances that the 5 PANs which are of specified persons may move out of the list during the financial year and for that there will be need to recheek at the time of making tax deduction or tax collection.

6. The list would be drawn afresh at the start of each financial year and the above process would have to be repeated. For example, at the beginning of the financial year 2023-24 a fresh list would be prepared with previous year 2021-22 as the relevant previous year. Then, no name would be added to the list of specified persons during the financial year and only name would be removed based on the logic given in the 3rd to 6tj bullets of paragraph 4 above.

7. It may be noted that as per the provisos of Section 206AB & 206CCA, the specified person shall not include a non-resident who does not have a permanent establishment (PE) in India. Since the functionality does not have the visibility of non-resident having PE in India, there is likelihood that non-resident having PE in India may not get retlected in this list. Tax Deductors & Collectors are expected to carry out necessary due diligence in respect of non-residents about the applicability of section 206AB and section 206CCA on them.

8. Circular no 11 of 2021 was issued on 21st June 2021. It was seen that even though this user friendly functionality has been provided to tax deductors/collectors. and explained through a circular, some of these deduclors/collectors were asking the deductee/collectee to produce evidences of their filing of return of income. It may be again highlighted that this functionality has been developed to ease compliance for tax deductors/collectors. Asking the deductee/collectee to file evidence of furnishing of their return defeat the purpose of this taxpayer friendly measure. All tax deductors/collectors are requested to make note of this circular for compliance.

(Ankit Jain)

Under Secretary (TPL)-III

Law(s) Governing the eForm DPT-3

eForm DPT-3 is required to be filed pursuant to rule 16 of the of the Companies (Acceptance of Deposits) Rules, 2014 which are reproduced for your reference.

Rule 16: Return of deposits to be filed with the Registrar:

Every company other than Government company to which these rules apply, shall on or before the 30th day of June, of every year, file with the Registrar, a return in Form DPT-3 along with the fee as provided in Companies (Registration Offices and Fees) Rules, 2014 and furnish the information contained therein as on the 31st day of March of that year duly audited by the auditor of the company.

Form DPT-3 shall be used for filing return of deposit or particulars of transaction not considered as deposit or both by every company other than Government company.

Purpose of the Form:

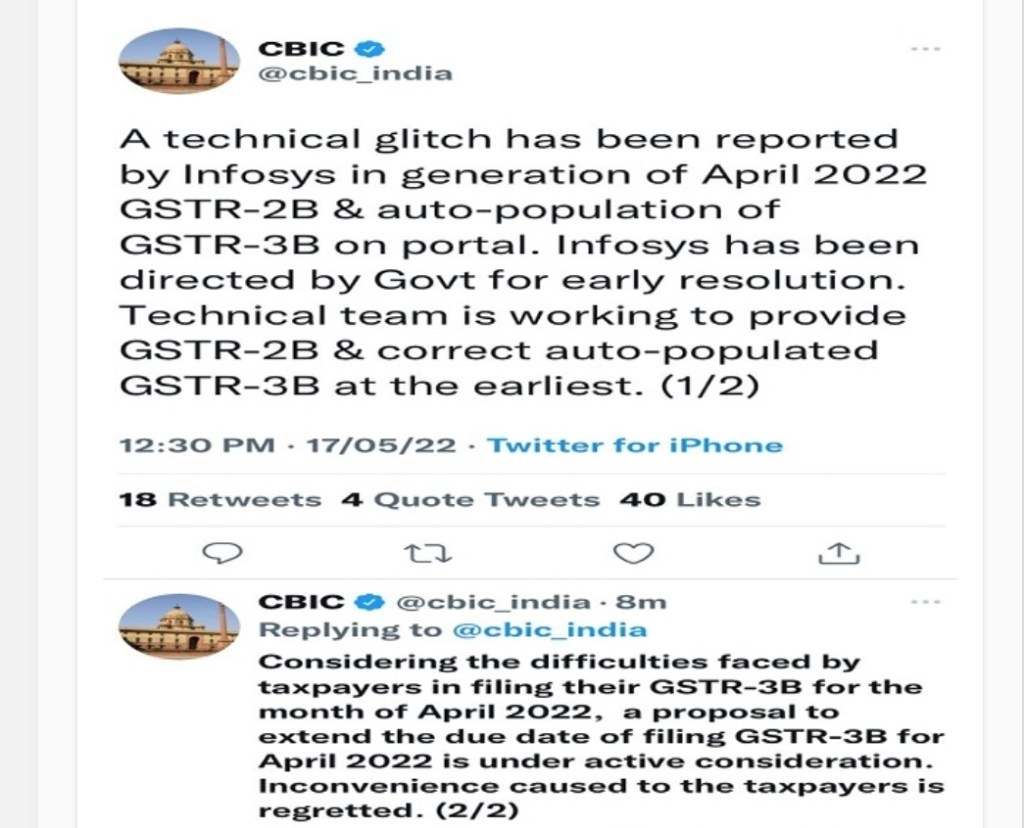

A technical glitch has been reported by Infosys in generation of April 2022 GSTR-2B & auto-population of GSTR-3B on portal. Infosys has been directed by Govt for early resolution. Technical team is working to provide GSTR-2B & correct auto-populated GSTR-3B at the earliest.

Considering the difficulties faced by taxpayers in filing their GSTR-3B for the month of April 2022, a proposal to extend the due date of filing GSTR-3B for April 2022 is under active consideration. Inconvenience caused to the taxpayers is regretted.

*Delhi ROC adjudication order for non maintenance of Registered office in the matter of Garage Cowork Private Limited (Order dated 13/05/2022)*

https://youtu.be/BD7HOuadhKA

✒️ *Action initiated on the basis of _On line complain through serious fraud form_ against Co.*

✒️ *Complainant also filed a writ petition to HC praying appropriate action for default of provisions of Companies Act*

✒️ *Penalty imposed on Company: Rs. 1 Lakh, and on two foreign director Rs. 1 Lakh each*

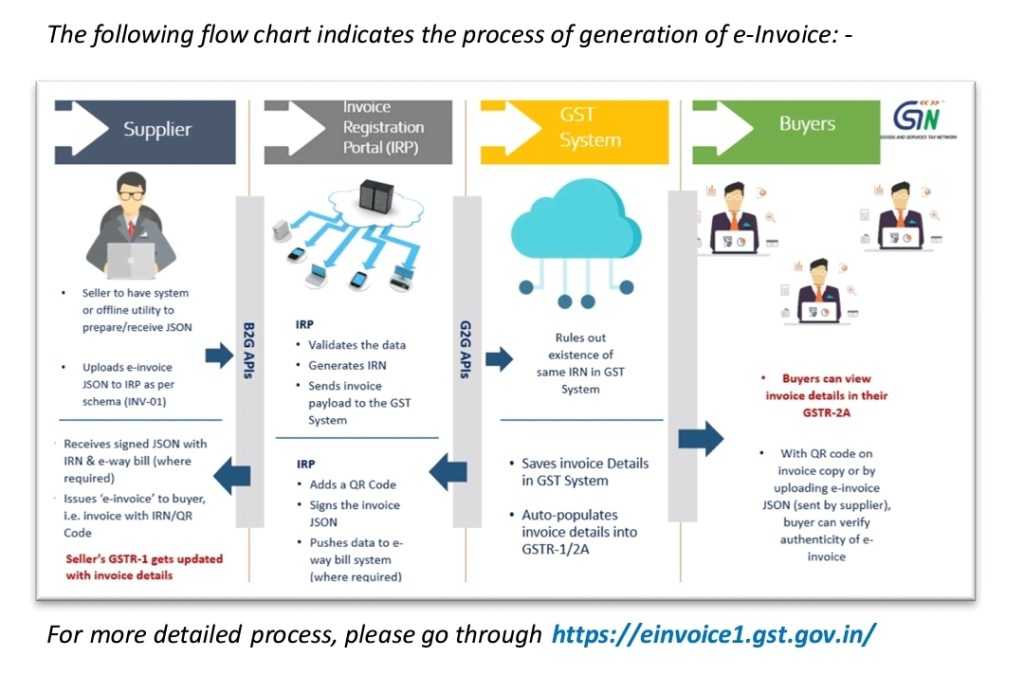

Flowchart :

What is ‘e-invoicing’?

As per Rule 48(4) of CGST Rules, notified class of registered persons shall prepare an invoice by incorporating the Invoice Reference Number (IRN) and the QR-Code generated by uploading specified particulars in FORM: GST INV-01 on Invoice Registration Portal (IRP).

Such invoice containing, inter alia, the QR Code embedded with IRN (mentioning IRN separately, is optional), issued by the notified supplier to buyer is commonly referred to as ‘e-invoice’ in GST.

Please note that ‘e-invoice’ doesn’t mean generation of invoice on a Government portal or issue of invoice in pdf form.

How is ‘e -invoicing’ different from present system (normal invoice)?

There is no much difference between the e-invoice and a normal invoice. In the e-invoice system, the notified registered persons will continue to create their GST invoices on their own Accounting/Billing/ERP Systems, but it shall bear the QR Code embedded with IRN (mentioning IRN separately, is optional), pre-generated on IRP. In other words, the specified contents of the invoices will have to be first posted in FORM: GST INV-01 on IRP, to generate the said unique IRN with a QR Code. e-Invoice is nothing but an invoice issued to the receiver of goods/services by the supplier along with the QR Code .

A GST invoice issued by the notified supplier will be valid only with a valid IRN/QR-code.

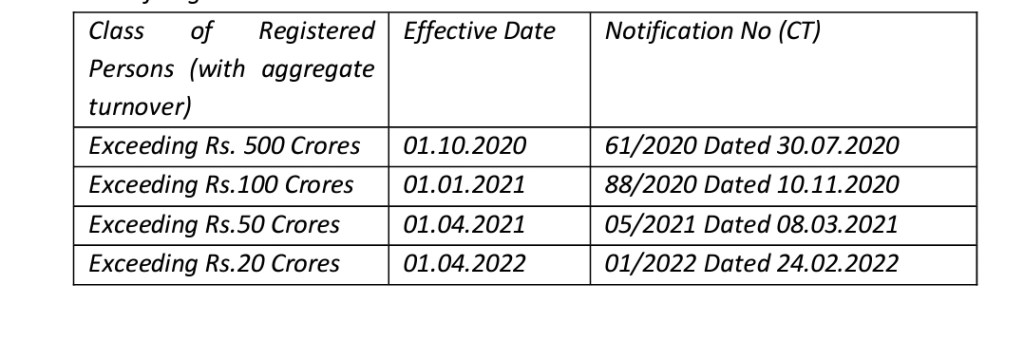

For which businesses, e-invoicing is mandatory?

e-invoicing is mandatory for the class of Registered Persons whose aggregate turnover (based on PAN) is more than the prescribed limit (as per relevant notification) in any preceding financial year from 2017-18 onwards. of The effective date from which the e-Invoice was notified as mandatory for different class of Registered Persons is indicated hereunder:

What are the advantages of e-invoice for businesses?

e-invoice has many advantages for businesses such as:

Ø Smooth ITC reconciliation by Auto-reporting of invoices into GST return;

Ø Simultaneous generation of EWB

Ø Utmost reliability (no need to doubt the genuineness- eliminates fake invoices);

Ø Reconciliation problems are eliminated;

Ø Standardisation & eliminates data entry errors;

Ø Documents become tax compliant on real time basis;

Ø Reduction of processing costs; Ø improve payment cycles;

Ø thereby greatly improving overall business efficiency and ensure Ease of doing business.

Dear Sir,

Please find below YouTube video link on *How to open Capital Gain A/c ? II Opening II Types II Interest rates II Withdrawal II Closer*

https://youtu.be/NRE61Gx0Ynk

Regards,

Bipul Kumar

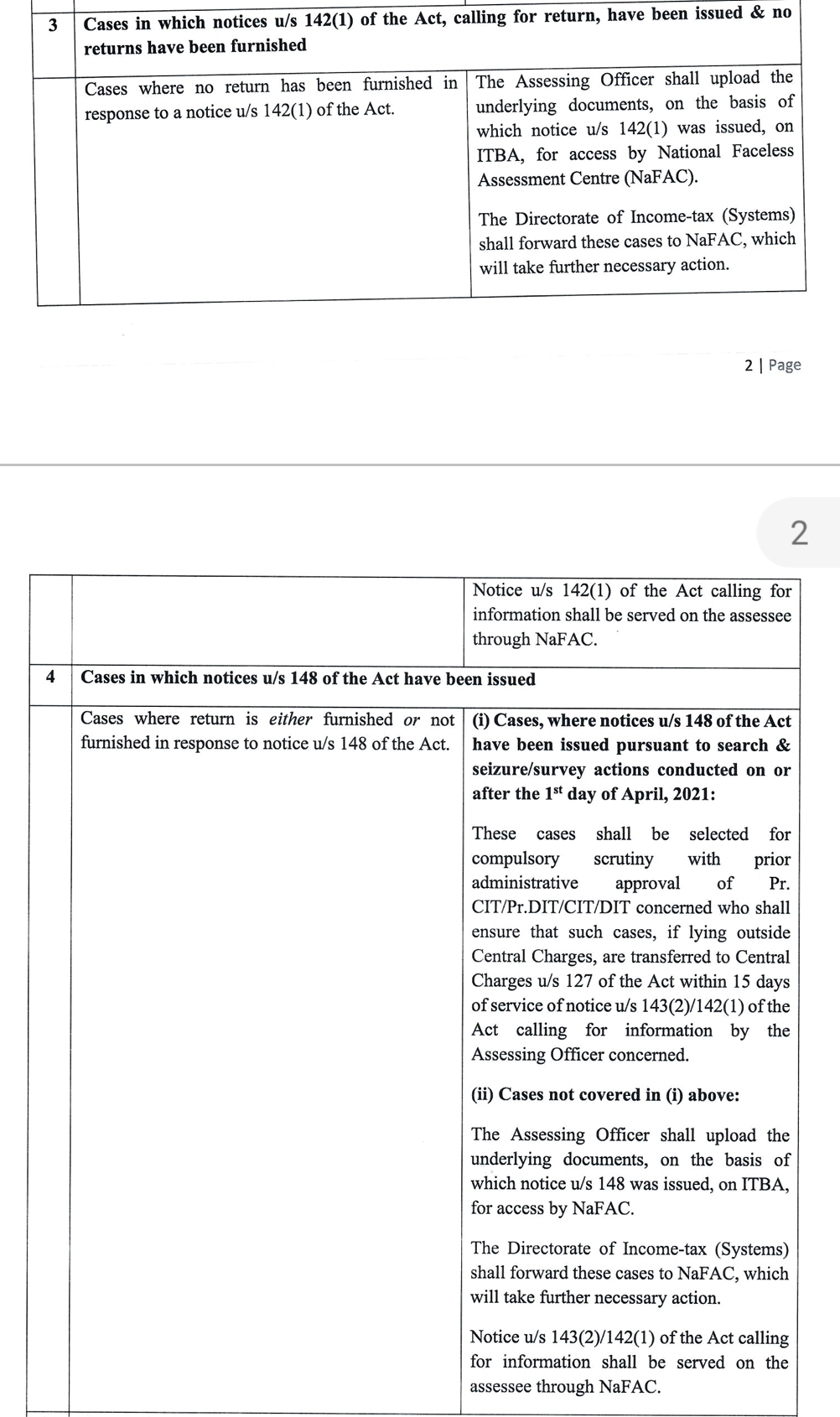

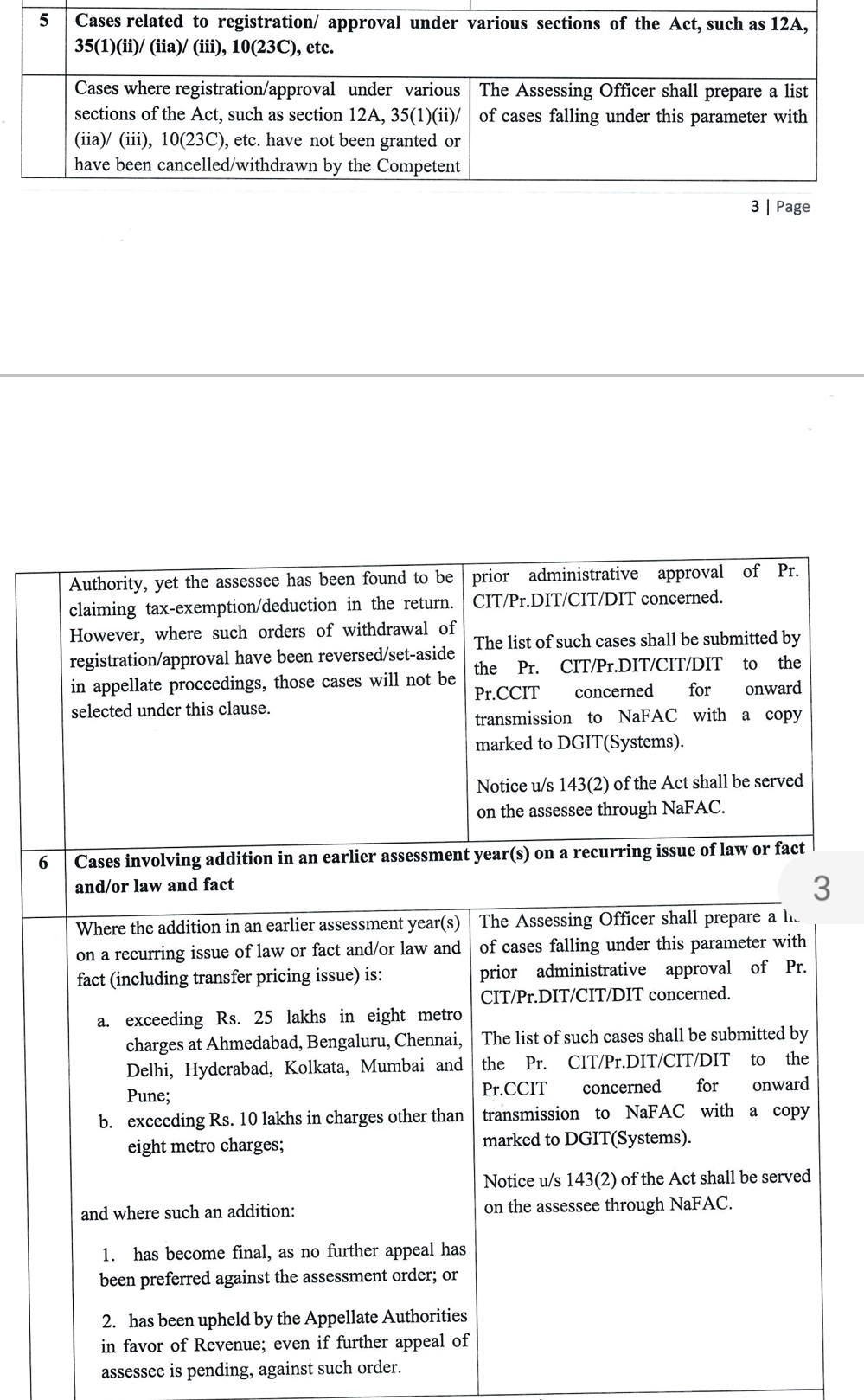

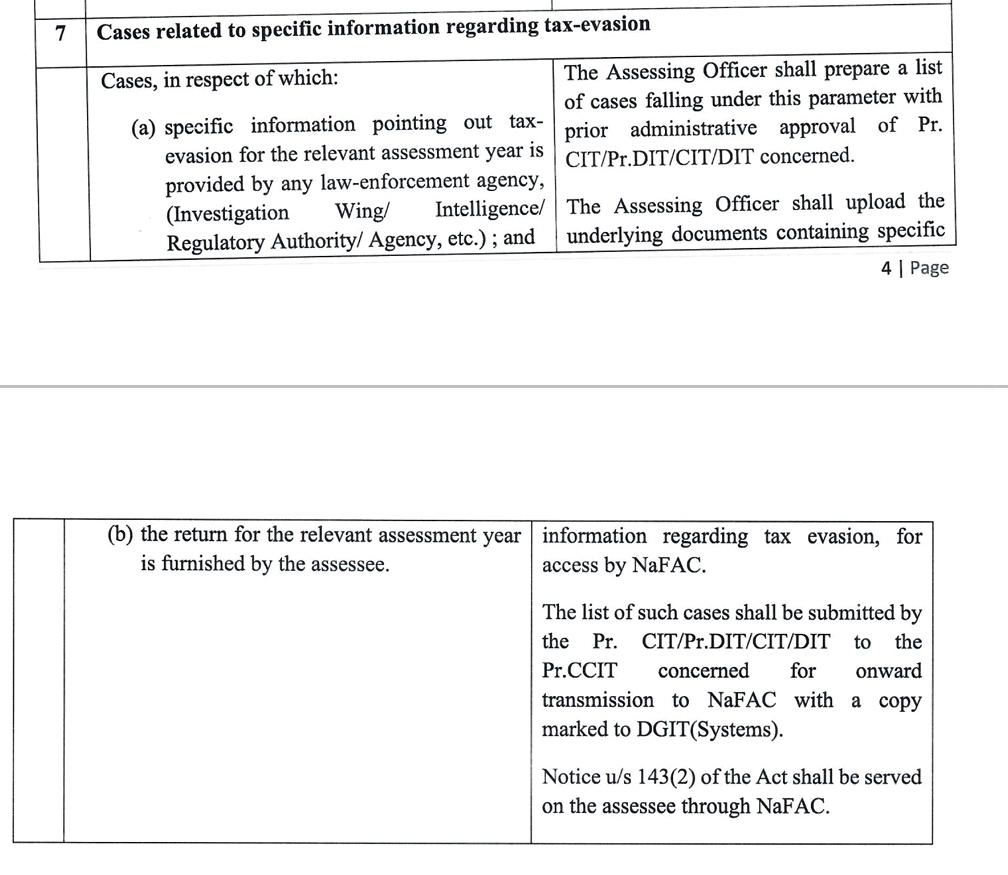

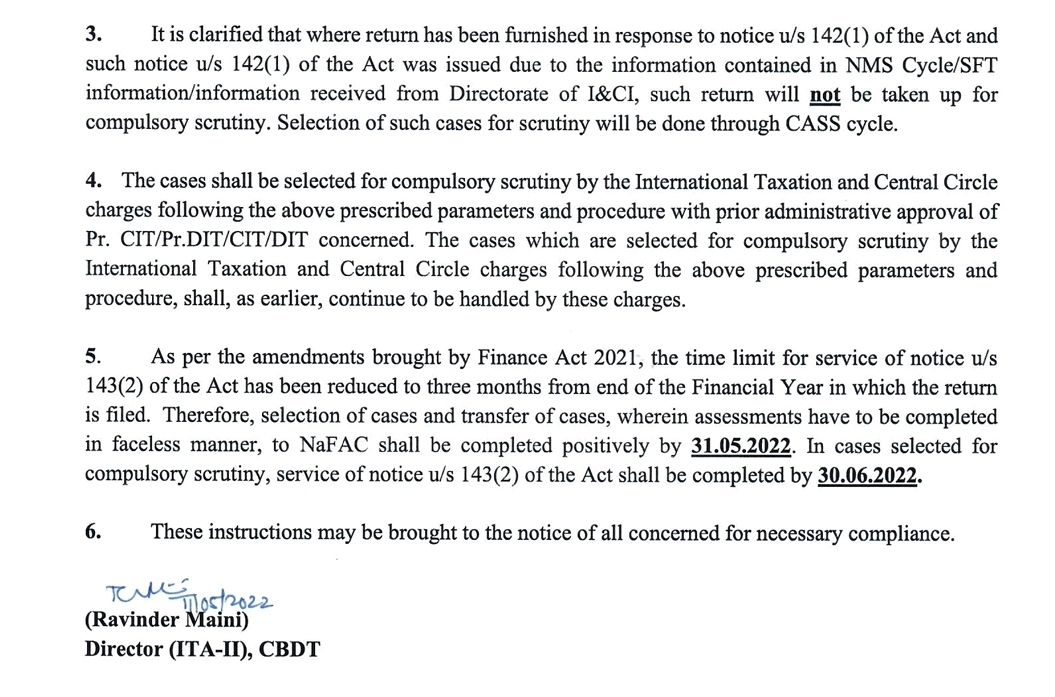

The parameters for compulsory selection of return for complete scrutiny during FY 2022-23 and procedure for compulsory selection in such cases are prescribed as under: